OVERVIEW

POPULAR ARTICLES

The 150-year-old concept of the nation state is steadily being altered by: a) the growing complexity for such states to tax economic activity; b) the fact that barring USA & China, every state has reduced control of the critical technologies which underpin modern economies; and c) the migration of gainful employment away from salaried jobs (which are easy to tax) and towards global gig work (which is harder to tax).

National investing was, in large part, a one-time bet on a closed market re-rating as it opened — a trade that has now largely played out. As the nation state weakens, the case for diversifying into US and global equities over a home-biased, “buy-the-national-index” strategy is stronger than at any point in the liberalisation era.

The Nation State Was Born in 19th Century Europe…

The idea of a nation-state was and is associated with the rise of the modern system of states, often called the “Westphalian system”, following the Treaty of Westphalia (1648). The balance of power, which characterized that system, depended for its effectiveness upon clearly defined, centrally controlled, independent entities, whether empires or nation states, which recognize each other’s sovereignty and territory. (i)

The first high profile implementation of the construct of the nation state was in Germany in the second half of the 19th century under Otto Von Bismarck (ii) . The unification of Germany was a process of building the first nation-state for Germans with federal features, with a common army, a customs union and a tax union . It commenced on 18 August 1866 with the adoption of the North German Confederation Treaty establishing the North German Confederation, initially a military alliance de facto dominated by the Kingdom of Prussia, which was subsequently deepened through adoption of the North German Constitution.

Subsequently, other European countries followed the German model and the modern idea of the nation state as we know it today was on its way to becoming the default model of economic and political union the world over.

…But is Fading Away Across the World in the 21st Century

In the 21st century however the nation state is under severe pressure. Across the world, three sets of powerful economic forces are steadily eroding the construct of the nation state

The State’s Ability to Tax is Shrinking

Joseph Schumpeter called the modern polity a ‘tax state’: its capacity to do anything rests on its capacity to raise revenue. With capital – both investments in financial markets and investments in plant & productive capacity – now mobile across borders, it is increasingly challenging for the nation state to tax the returns arising from capital. Since 40% of India’s GDP is accounted for returns to capital (iii) , as the years go by, the Indian state will find it increasingly complex to tax this part of national income. Any attempt to tax this will result in capital seeking optimization and leaving the country – click here for our June 2026 blog on this subject .

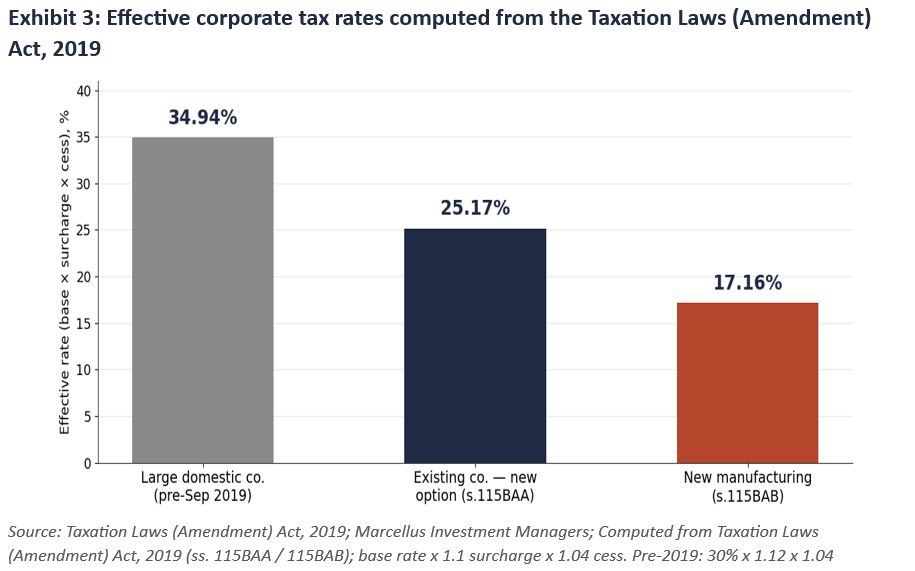

It is not just FIIs who are reluctant to pay tax; corporates the world over are just as reluctant. India’s Taxation Laws (Amendment) Act, 2019 cut the base rate for existing domestic companies to 22% and introduced a 15% rate for new manufacturing companies. The effective tax rates shown in the chart below highlight the remarkable extent of the 2019 corporate tax cut.

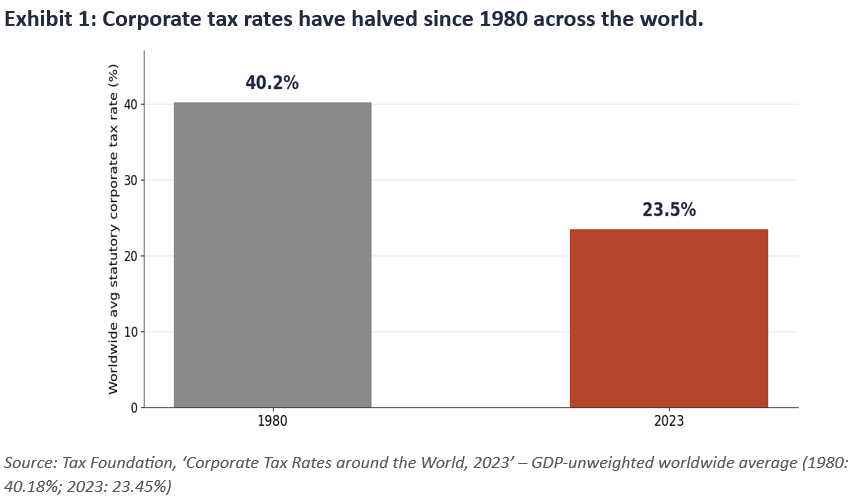

To be clear, the growing shifts in how the state to taxes capital are NOT confined to India – this is a global phenomenon – see the opening exhibit of this blog. Capital is mobile; a booked profit can move across borders far more easily than a worker. If one government raises corporate tax, capital can relocate. Anticipating this, governments compete competitively on rates — a pattern the tax-competition literature has tracked for three decades, and which is visible in the worldwide average rate. (iv)

2. Technology Sits Outside National Control for Every Nation Barring USA & China

Sovereignty increasingly means control over compute, data, energy and the hardware beneath them. Farrell & Newman show how states that sit at the hub of critical networks — financial messaging, cloud, chokepoint supply chains — can leverage those networks structurally, restricting access (the ‘chokepoint effect’) or tracking information (the ‘panopticon effect’) (v) . On each key network, the hub is the US or China, and India is a technology taker.

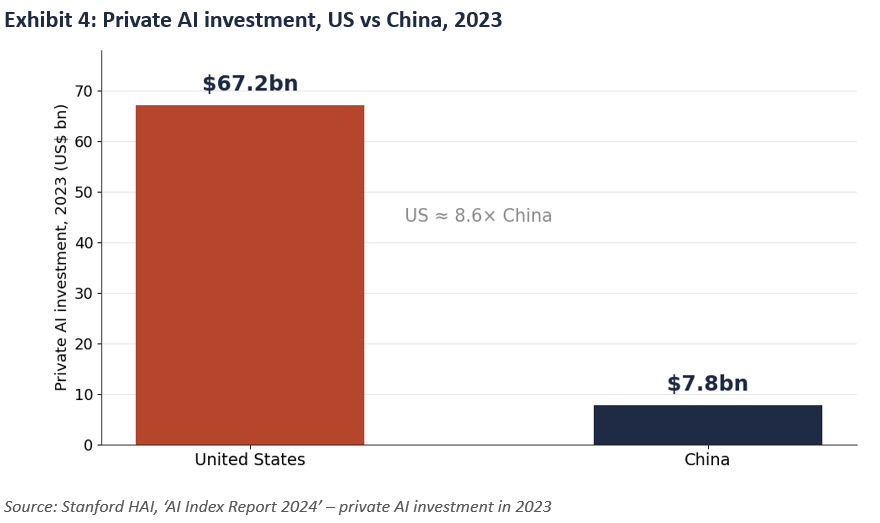

The frontier of AI — the largest models, leading-edge accelerators, and hyperscale cloud — is overwhelmingly American (with chip fabrication concentrated in Taiwan). Private capital tells the story – see chart below.

India’s responses — RBI’s 2018 payments-data-localisation mandate, the Digital Personal Data Protection Act (2023), and the India AI Mission approved by the Union Cabinet in 2024 with an outlay of roughly ₹10K crore (vi) — are real attempts to claw back control, but modest relative to the gap. A jurisdiction problem compounds it: data on US-headquartered clouds can be reachable under the US CLOUD Act regardless of physical location — the panopticon effect in practice. (vii)

If AI is American, the energy transition is Chinese. The IEA reports that China’s share exceeds 80% at every major manufacturing stage of solar PV, rising above 95% for polysilicon and wafers, (viii) and it dominates battery-cell manufacturing and the processing of rare earths and other critical minerals. (ix)

The dependency is weaponizable — as is widely known, China has restricted exports of rare earths and, more recently, gallium and germanium — a textbook chokepoint. India’s answer (PLI for solar, advanced-chemistry-cell batteries and electronics, plus a Critical Minerals Mission) addresses this, but upstream capacity takes a decade to build.

3. Global Gig Work and Cryptocurrencies

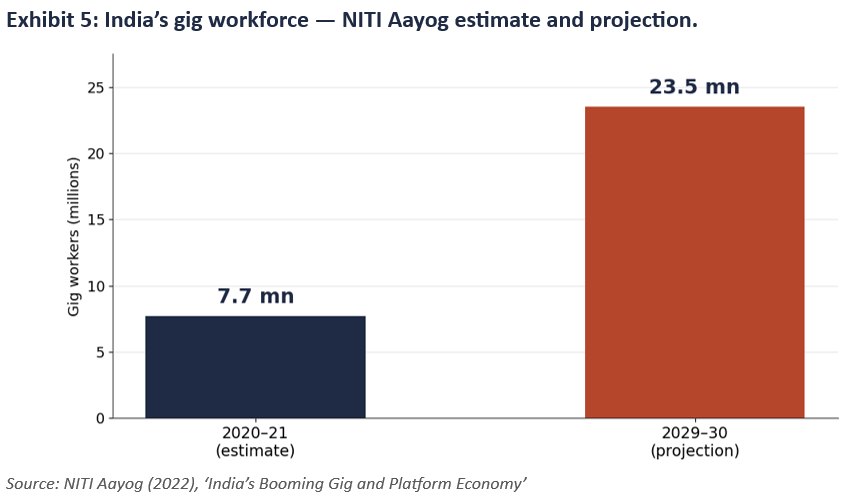

The second squeeze is on labour income. The salaried employee is the tax authority’s ideal subject: income is third party-reported and withheld at source. The self-employed and gig worker are harder to observe. NITI Aayog projects India’s gig workforce to roughly triple this decade – see chart below.

The more fundamental point is that India’s income-tax net was never wide: the workforce is overwhelmingly informal and the share of the population paying material income tax is small. In fact, as highlighted in our bestselling book, “Breakpoint: The Crisis of the Middle Class & The Future of Work,” less than 40 million of India’s 1.5 billion strong population pays substantial Income Tax. India therefore leans on indirect (GST) and corporate taxes to generate tax revenues. However, as explained above, it is increasingly untenable for the nation state to tax corporates heavily. That in turn underscores the growing challenge the modern nation state faces in collecting taxes.

The state’s ability to collect taxes is undergoing a shift due to the changing environment of its most captive source of Income Tax – white collar office workers. As we have explained in Breakpoint and in several podcasts, the rise of automation and AI in the workplace means that white collar office workers the world over are being replaced by technology. As detailed in “Breakpoint” in India, this has meant the job creation for graduates has come to a halt over the past three years. (See our blog dated 18 June 2026 for more information.)

For white collar workers, as options for salaried employment dwindle, the most attractive source of income now is global gig work sourced from platforms such as Upwork. Increasingly however the mode of payment for such work is likely to be in the form of cryptocurrency. Effectively, labour income itself seems likely to migrate out of the observable financial system — paid in crypto or, more plausibly, dollar stablecoins.

Modern income taxation does not rely on taxpayer honesty; it relies on third-party information and withholding. The employer reports and withholds (TDS/PAYE); the bank reports interest and large flows; the exchange or broker reports gains. Compliance is high wherever a regulated intermediary sits between the taxpayer and their money, and collapses where one does not — which is why self-employment and cash income are chronically under-reported everywhere. Crypto is, in effect, a technology for removing those intermediaries. The IMF’s analysis of taxing crypto-assets makes the point directly: pseudonymity and disintermediation mean the binding constraint is enforcement, not the statute — a government can declare crypto income taxable (most now do) and still be unable to see it. (x)

The Fading State Points to the Twilight of National Investing

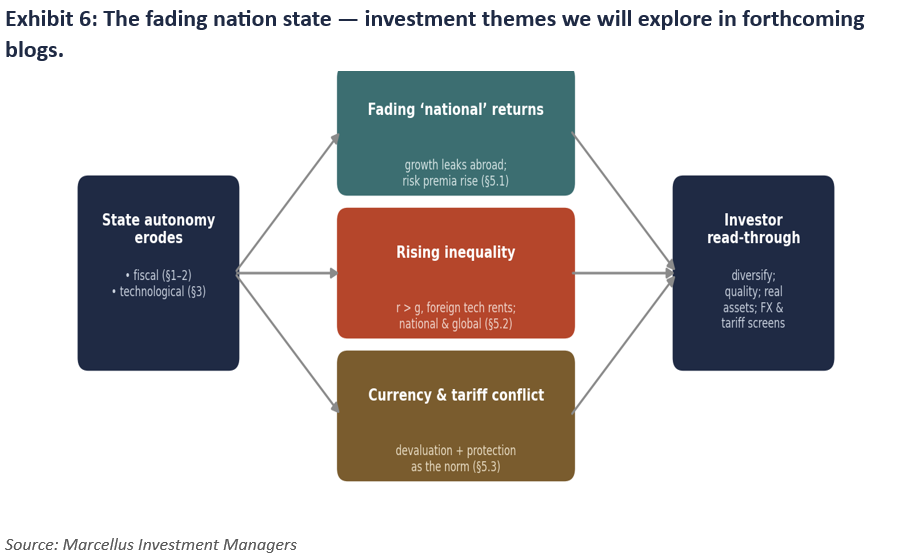

The erosion of the nation state has several implications. For example, if the nation state was the default provider of public goods such as law & order, education, and public sanitation, as the nation state fades, it is not obvious who will provide these services. In our subsequent blogs, we will delve deeper into these subjects. We believe that the erosion of the nation state opens up several attractive investment opportunities alongside key investment risks. The chart below highlights some of the themes which we will explore in our forthcoming blogs.

In this blog we delve deeper into one such implication of the fading of the nation state – the decreasing relevance of investing based on national boundaries.

National investing was, in large part, a one-time bet on a closed market re-rating as it opened — a trade that has now largely played out. As the nation state weakens, the case for diversifying into US and global equities over a home-biased, buy-the-national-index strategy is stronger than at any point in the liberalisation era: owning the hub — and the foreign-owned commanding heights themselves — is how an investor captures the value that is, by this very thesis, leaking away from the periphery.

Domestic equity returns have historically rested on three pillars: a predictable national policy regime, a captive pool of domestic savings, and growth that accrued to listed national champions. Each weakens as the forces which we have described in this blog accelerate in the coming years — and stock market returns in India already show the effect.

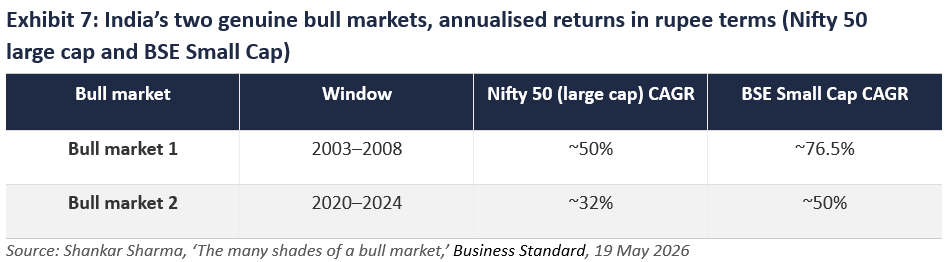

On a strict definition of a broad-based advance, India has had only two genuine bull markets in the liberalisation era: 2003–2008 and 2020–2024 – see table below. The 1991–92 boom was a narrow, bank-financed episode, and the late-1990s technology surge too brief and too concentrated, for to qualify. Between the two real advances, annualised returns have stepped down hard.

Large-cap compounding fell by more than a third — from about 50% a year to about 32% — and small-cap compounding from about 76% to about 50%. The returns plane, on the same index that carried the liberalisation trade, has shifted down.

This is not a cyclical accident; it is the same erosion described in the preceding section of this blog, seen from the bottom up. Three forces then compress forward returns, largely independent of the cycle count.

First, valuation math: each run now begins from a far larger base and a higher starting multiple, and high starting valuations mechanically imply lower subsequent long horizon returns. (xi)

Second, lower trend growth: a slower growing, ageing corporate base translates into lower asset returns. (xii)

Third, a fragmentation premium: as the world splinters, cross-border returns fall and the risk premium demanded of a periphery market rises. (xiii)

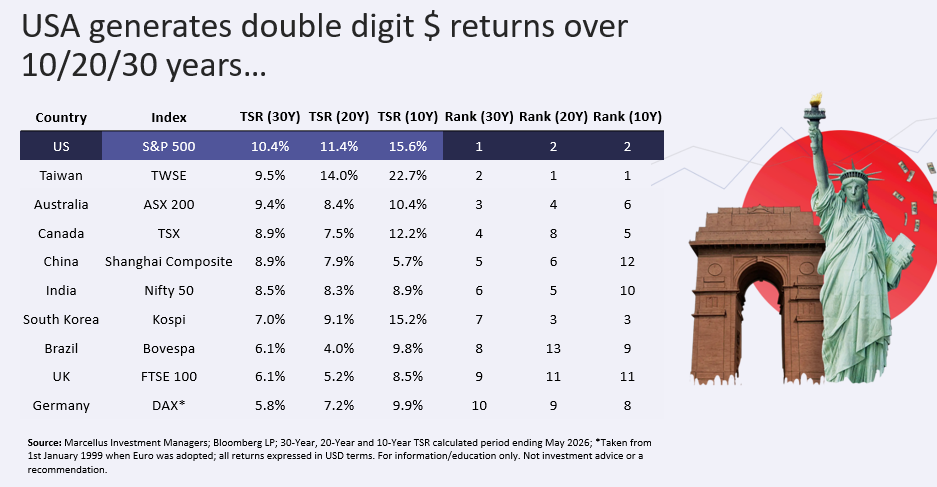

Overlaid on all three is the value-leakage: as the commanding heights of the new economy (AI, cloud, advanced-manufacturing inputs) come to be owned abroad, a rising share of the value created in India accrues to owners outside it, and the risk premium demanded of the ageing domestic champion rises as capital turns mobile and the policy-and-currency regime less autonomous. The table below might help you contextualise how powerful this value migration from the periphery to the hub is.

Why the United States is the exception and why this matters for you

The decay is not universal, and the exception is instructive. US equity cycles have not shown the same step-down in returns which has been seen in India — and the reason is the mirror image of India’s. The United States issues the reserve currency and sits at the hub of the very networks whose foreign ownership drains value from the periphery: the dollar, the deepest and most liquid capital markets, Treasuries as the global risk-free asset, and the frontier-technology franchises (AI, cloud, chip design) that capture the economy’s scarce rents. When state autonomy erodes elsewhere, capital does not disappear; it flows toward that hub, and faster in stress — so the US risk premium stays compressed while its listed champions harvest the growth that opening economies cede. This is the underlying logic of the preceding sections of this blog expressed in asset prices.

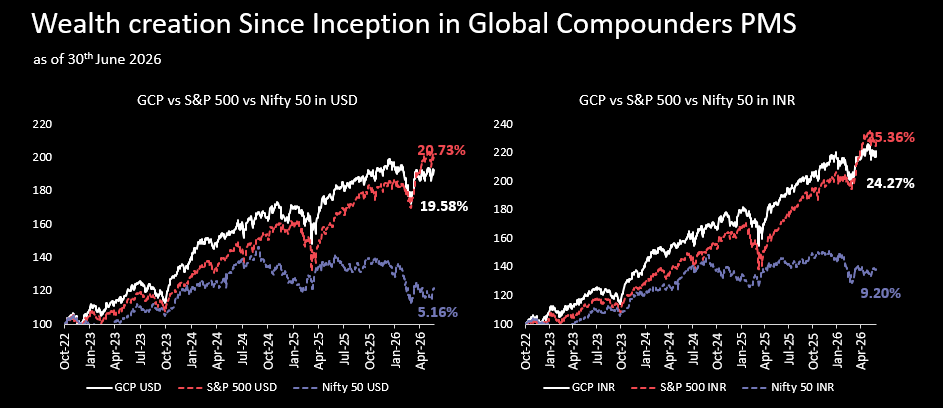

Through its offices in GIFT City, Gujarat, Marcellus offers multiple funds through which investors can access the world’s largest stock markets. Ticket sizes for these investments start at US$5K (~Rs 4.5 lakhs)*. The track record of our flagship global product – the Global Compounders Portfolio – is shown below.

For more information on available products and suitability, please scan the QR code underneath this chart.

*subject to the specific product, regulatory classification, and investor eligibility criteria

Note: Marcellus performance data is shown gross of taxes and net of fees & expenses charged till end of last month on client account. Performance fees are charged annually in December. Returns more than 1-year are annualized. Marcellus’ GCP USD returns are converted into INR using USD: INR exchange rate from RBI – Link for the reference

Since Inception performance calculated from 31st Oct 2022. The inception date is 31st Oct 2022, being the next business day after the account got funded on 28th October 2022. S&P 500 net total return is calculated by considering both capital appreciation and dividend payouts. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the IFSCA or US SEC. Performance is the combined performance of RI and NRI strategies. S&P 500 NTR is the benchmark for the strategy. Nifty 50 is provided for reference to illustrate the relative performance of the US and Indian markets. Past performance pertains to Marcellus’ GCP PMS strategy, not to this IFSC Retail Scheme and is not indicative of future results.

Thanks,

Saurabh Mukherjea

The views and opinions expressed in this material are those of the writers/authors and do not necessarily reflect the official policy. This material is for informational and educational purposes only and should not be considered as financial, investment, or other professional advice.

Click here for details about our regulatory registration and licensing information.

Disclaimer:

This material is for informational purposes only and does not constitute investment advice or research. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the International Financial Services Centres Authority (IFSCA) as a Fund Management Entity (Retail) offers Retail and Non-Retail products and is registered with the U.S. Securities and Exchange Commission (SEC) as an Investment Advisor. The PMS strategy, Category III AIF products (non-retail schemes), and IFSCA retail schemes are distinct offerings with different regulatory frameworks, risk profiles, fee structures, and investment thresholds. Minimum investment amounts referenced (e.g., ~US$5K) are applicable to specific IFSCA retail schemes and may not apply to PMS or Category III AIF products. Investors should refer to product-specific documents for details before investing. This communication is not a solicitation in jurisdictions where Marcellus is not regulated. It is confidential and intended solely for the addressed recipient; unauthorized use or distribution is prohibited. carefully read the Disclosure Document, Form ADV, Form CRS and any other documents or disclosures provided to them by Marcellus, as applicable. Actual results may differ materially from those suggested in this note due to risk or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions globally, inflation, etc. Information provided is based on data available at the time of preparation and may change without notice. Marcellus makes no representation regarding accuracy or completeness and assumes no obligation to update. Recipients should rely on their own judgment and consult independent legal, tax, and financial advisors before making any investment decisions. Investments are subject to market risks and uncertainties. This material may include “forward looking statements”. All forward-looking statements involve risk and uncertainty. Any forward-looking statements contained in this document speak only as of the date on which they are made. Past performance is not indicative of future results, and there is no assurance that investment objectives will be achieved. Marcellus, its affiliates, employees, and authors may have financial interests in securities discussed. To the fullest extent permitted by law, Marcellus disclaims all liability arising from the use of this material. This is not meant for US investors.

Sources:

(i) https://en.wikipedia.org/wiki/Nation_state

(ii) https://en.wikipedia.org/wiki/Unification_of_Germany

(iii) Centre for Development Economics, Delhi School of Economics: http://www.cdedse.org/pdf/work273

(iv) Devereux, M.P., Lockwood, B. & Redoano, M. (2008), ‘Do countries compete over corporate tax rates?’, Journal of Public Economics, 92(5–6), pp. 1210–1235; Keen, M. & Konrad, K.A. (2013), ‘The Theory of International Tax Competition and Coordination’, in Handbook of Public Economics, Vol. 5, Elsevier; worldwide average statutory rate data from Tax Foundation, ‘Corporate Tax Rates around the World’ (annual).

(v) Farrell, H. & Newman, A. (2019), ‘Weaponized Interdependence: How Global Economic Networks Shape State Coercion’, International Security, 44(1).

(vi) Cabinet Approves Over Rs 10,300 Crore for IndiaAI Mission, will Empower AI Startups and Expand Compute Infrastructure Access

(vii) Clarifying Lawful Overseas Use of Data (CLOUD) Act, 2018 (United States).

(viii) IEA (2022), ‘Solar PV Global Supply Chains’. China’s share exceeds 80% across polysilicon, ingots, wafers, cells and modules, and is projected above 95% for polysilicon and wafers.

(ix) IEA, ‘Energy Technology Perspectives’ and critical-minerals reporting; USGS Mineral Commodity Summaries for rare-earth mining/processing shares.

(x) Baer, K., De Mooij, R., Hebous, S. & Keen, M. (2023), ‘Taxing cryptocurrencies’, Oxford Review of Economic Policy, 39(3); IMF Working Paper WP/23/144. Argues the core difficulty is enforcement/visibility rather than the legal characterisation of crypto income.

(xi) Methodological caution on cross-cycle return comparisons: the authoritative long-run, cross-country equity-return dataset is Dimson, E., Marsh, P. & Staunton, M., ‘Global Investment Returns Yearbook’ (annual; UBS/Credit Suisse) — used to date and measure cycles and long-run real returns rather than eyeballing index levels.

(xii) Campbell, J. & Shiller, R. (1988), ‘Stock Prices, Earnings, and Expected Dividends’, Journal of Finance, 43(3); Campbell & Shiller (1998), ‘Valuation Ratios and the Long-Run Stock Market Outlook’, Journal of Portfolio Management.

(xiii) Summers, L. (2014), ‘U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the Zero Lower Bound’, Business Economics, 49(2); Rachel, Ł. & Summers, L. (2019), ‘On Falling Neutral Real Rates, Fiscal Policy, and the Risk of Secular Stagnation’, Brookings Papers on Economic Activity.