OVERVIEW

POPULAR ARTICLES

Summary: Our meetings with a dozen large FIIs in North America and UK over the past few weeks suggest that scrapping equity Capital Gains Tax (CGT) for FIIs will trigger 3 different types of benefits for the Indian economy: a) lower borrowing costs for the sovereign and hence for corporates; b) a stronger INR and a healthier forex position; and c) a boost to economic growth on the back of lower cost of capital.

We spent the last fortnight meeting pension funds, endowments and family offices across the US, Canada and the UK. These conversations, especially in the US were sobering, driven by the uncomfortable reality that MSCI India has underperformed the MSCI Emerging Markets Index over the past year by the highest margin in over three decades. FIIs pulled Rs 3 trillion (~$31Bn) out of Indian equities in 2025 and Rs 3.4 trillion (~$35Bn) in the first six months of 2026 alone. The rupee has been weak, India’s capital account is struggling, and India’s window to act is narrowing as global dollar liquidity stays expensive. Competition for capital is set to intensify further as the Fed is widely anticipated to follow the ECB in hiking rates later this year.

Thankfully however now that India’s valuations have cooled from their 2024 extremes, our discussions suggest that meaningful pools of global capital remain constructive on India’s long-term prospects. The sticking point for foreign investors is India’s capital gains tax (CGT) regime which has long been viewed by them as outdated an anomalous. The said CGT regime is increasingly viewed as an avoidable impediment to fresh allocations by large global investors to India, particularly given that most competing markets do NOT impose comparable capital gains taxes on foreign institutional investors (FIIs).

With foreign ownership of Indian stocks at a 15-year low, the question is how Indian policymakers can restore India’s standing as a preferred destination for global allocators. Given prevailing the macroeconomic constraints in India, reducing equity CGT rates for FIIs appears to us to be one of the few policy levers available to the Finance Ministry that can improve India’s competitiveness for global capital without materially compromising fiscal consolidation. We explain below why this is so.

The first and most obvious reason is that India’s treatment of foreign portfolio investors is increasingly out of step with global practice. The US, the UK, Germany, Japan and every major emerging-market peer — Korea, Brazil, China, Taiwan — exempt foreign portfolio investors from CGT on listed equities. India’s 12.5 per cent long term capital gains (LTCG) tax and 20 per cent short term capital gains tax (STCG) rates have no parallel among the markets we compete with for capital . While India was the EM destination of choice during the previous decade, equity investors have real alternatives now — Korea’s Value-Up programme, Taiwan’s semiconductor ecosystem, Japan re-rating for the first time in a generation, and Brazil trading at a fraction of our multiples at a time when commodities are doing well.

The arithmetic of a targeted FIIs’ tax exemption is straightforward. CGT collections on listed equities is approximately Rs 1 trillion a year. With foreign investors owning only around 15% of India’s listed market capitalization, a simple ownership-based approximation suggests a revenue impact of around ₹15,000 crore (around $1.5 bn). The potential macroeconomic benefits to India, however, accrue across a much larger base — India’s Rs 200 trillion sovereign debt market, the exchange rate, and domestic financing conditions. By strengthening the capital account and reducing the risk premium embedded in Indian financial assets, a tax cut could lower sovereign borrowing costs, support the rupee and ease imported inflation. Even a 50-basis-point reduction in sovereign yields would save the exchequer roughly Rs 8,000 crore in the first year on new issuance alone, with the benefits compounding over time as debt is refinanced at lower rates.

A common objection in India is that exempting foreign investors while taxing domestic investors creates an uneven playing field. But foreign capital is uniquely mobile and competes across jurisdictions in a way that domestic savings do not. Tax policy toward globally mobile capital should therefore be judged by its contribution to national welfare rather than identical treatment across investor classes. A retail investor sitting in India simply does not have the range of global choices open to him that a FII sitting in London or New York does and this leads us to our next point in favour of giving CGT relief to FIIs.

Arthur Laffer’s original insight was that beyond a certain rate, raising taxes can reduce revenues because the tax base shrinks in response. For capital gains, where the act of investing is voluntary, the elasticity is unusually high for FIIs. India’s hikes over the years from zero to 12.5 per cent on LTCG saw the Laffer response migrate entirely to FIIs, who measure dollar-denominated post-tax returns against a global opportunity set and now find better risk-adjusted returns in markets charging zero taxes on capital gains. Alongside premium valuations, slowing earnings growth and the absence of a large domestic AI beneficiary, the CGT regime has become an important headwind to foreign allocations. Conversely, the same response was largely absent among domestic investors, whose savings remain relatively captive. A 12.5 per cent equity tax remains considerably more attractive than 39 per cent on a fixed deposit or debt instrument for a retail investor. Indian retail investors had no alternative; they absorbed the higher tax drag without a drop in market participation. The behavioural response to higher capital gains taxation was therefore concentrated among foreign investors.

The debt experiment has already proved the mechanism. Through the Income-tax Amendment Ordinance of early June 2026, the Government of India wiped out remaining withholding and CGT friction on Fully Accessible Route sovereign bonds for foreign investors. The response was instantaneous: over Rs 35,000 crore of fresh FII debt inflows in subsequent weeks, and a 15-basis point fall in the 10-year yield. The replication case on equity is stronger due to the inherent nature of sovereign risk. While foreign debt creates rigid, contractual repayment obligations that can severely strain a nation’s balance of payments during an economic downturn, equity capital carries no such sovereign liability. Equity is permanent risk capital that shares in the economic downside, making a tax-induced shift toward foreign equity a safer way to fund our capital account deficit.

Fiscal-discipline objections to a tax cut rooted in the budget’s 4.3 per cent deficit target underestimate how the broader macro responds. A stronger rupee also reduces imported inflation and gives the RBI room to ease monetary policy.

There is also a longer-term reason why attracting foreign capital matters. The IT services sector that has supported India’s balance of payments for two decades faces, for the first time, a credible challenge from artificial intelligence. The optimistic case that India eventually emerges as a major manufacturing exporter is real but will take time to materialize. In the interim, the capital account remains India’s most immediate lever for funding investment, supporting the rupee and financing infrastructure. The current tax framework unnecessarily discourages precisely the kind of long-term foreign capital India needs.

Cutting the equity tax now is one of the rare policy measures whose potential benefits appear disproportionate to its fiscal cost. The case stands on the static arithmetic alone and grows stronger with every second-order consequence and with every passing week.

To learn more about our investment offerings across our domestic and offshore strategies (through GIFT City), please visit our contact us at https://marcellus.in/invest/ or use the QR code shown below.

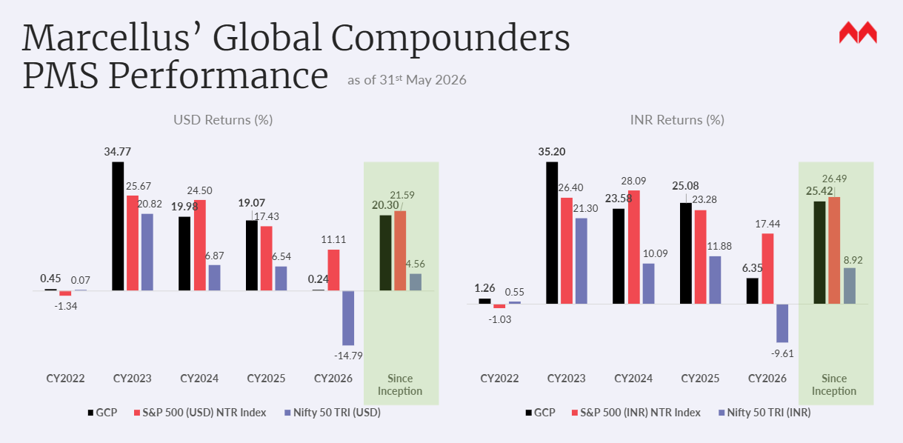

Note: Marcellus performance data is shown gross of taxes and net of fees & expenses charged till end of last month on client account. Performance fees are charged annually in December. Returns more than 1-year are annualized. Marcellus’ GCP USD returns are converted into INR using USD: INR exchange rate from RBI – Link for the reference

Note: * Since Inception performance calculated from 31st Oct 2022. The inception date is 31st Oct 2022, being the next business day after the account got funded on 28th October 2022. S&P 500 net total return is calculated by considering both capital appreciation and dividend payouts. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the IFSCA or US SEC. Performance is the combined performance of RI and NRI strategies. S&P 500 NTR is the benchmark for the strategy. Nifty 50 is provided for reference to illustrate the relative performance of the US and Indian markets. Past performance pertains to Marcellus’ GCP PMS strategy, not to this IFSC Retail Scheme and is not indicative of future results.

Marcellus GCP PMS is offered by Marcellus Investment Managers GIFT Branch in a segregated managed accounts format

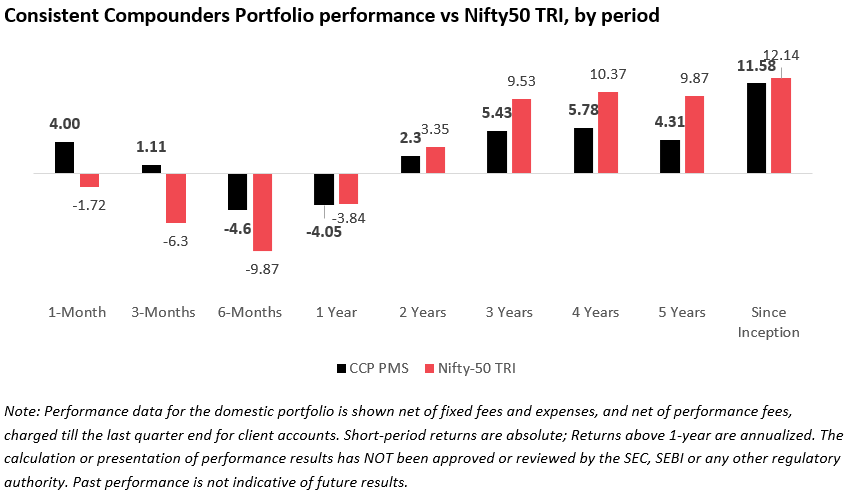

Consistent Compounders (CCP PMS) Performance as of 31st May 2026 (in %)

*For relative performance of particular Investment Approach to other Portfolio Managers within the selected strategy, please refer https://www.apmiindia.org/apmi/welcomeiaperformance.htm?action=PMSmenu , Under PMS Provider Name please select Marcellus Investment Managers Private Limited and select your Investment Approach Name for viewing the stated disclosure.

Thanks,

Saurabh Mukherjea

Data Sources:

https://www.ft.com/content/14bf78f6-e414-4bd7-973b-2b42da0bdde2?syn-25a6b1a6=1

https://www.moneycontrol.com/markets/fii-dii-data/cash/

https://economictimes.indiatimes.com/markets/stocks/news/fii-holding-of-india-equities-hits-15-year-low-at-rs-75-2-lakh-crore-nse-report/articleshow/125296715.cms?from=mdr

https://www.thehindu.com/news/national/govt-mopped-up-98681-crore-from-taxing-ltcg-in-listed-equities-in-fy23/article68463819.ece

https://www.indiabudget.gov.in/doc/rec/annex9.pdf

https://www.fortuneindia.com/economy/foreign-investors-pour-rs-35-000-cr-in-indian-bonds-after-govt-tax-exemption-move/144675

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2221455®=48&lang=2

Saurabh Mukherjea and Tej Shah work for Marcellus Investment Managers

Disclaimer:

The above material is neither investment research, nor investment advice. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the International Financial Service Centre Authority (Fund Management) Regulations, 2025 (“IFSCA”) as Fund Management Entity – Retail, rendering Investment Management Services. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by SEBI as a provider of Portfolio Management Services and acts as an Investment Manager to an Alternative Investment Fund. Marcellus is also registered with US Securities and Exchange Commission (“US SEC”) as an Investment Advisor. No content of this publication including the performance related information is verified by SEBI, IFSCA or US SEC. If any recipient or reader of this material is based outside India or US, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone. This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form. Data/information used in the preparation of this material is dated and may or may not be relevant any time after the issuance of this material. Marcellus takes no responsibility of updating any data/information in this material from time to time. The recipient of this material is solely responsible for any action taken based on this material. The recipient of this material is urged to read the Disclosure Document/Form ADV, Form CRS and any other documents or disclosures provided to them by Marcellus, as applicable, and is advised to consult their own legal and tax consultants/advisors before making any investment in the portfolio. All recipients of this material must before dealing and or transacting in any of the products referred to in this material must make their own investigation, seek appropriate professional advice and carefully read the Disclosure Document, Form ADV, Form CRS and any other documents or disclosures provided to them by Marcellus, as applicable. Actual results may differ materially from those suggested in this note due to risk or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions globally, inflation, etc. There is no assurance or guarantee that the objectives of the investment strategy/approach will be achieved. This material may include “forward looking statements”. All forward-looking statements involve risk and uncertainty. Any forward-looking statements contained in this document speak only as of the date on which they are made. Further, past performance is not indicative of future results. Marcellus clients, Marcellus clients, employees, and/or its associates, including the authors of this material (and their relatives), may have financial interests by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus and any of its directors, officers, employees and any other persons associated with this shall not be liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner whatsoever and shall not be liable for updating the document. This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.