OVERVIEW

POPULAR ARTICLES

Two in-depth, independently researched publications – our bestselling book “Breakpoint” and Azim Premji University’s “State of Working India 2026” – make three points which have significant implications for everyone reading this note: a) Jobs for graduates have dried up in India; b) Salaries for graduates have been FALLING for the best part of the past decade in real terms; and c) A university degree dramatically REDUCES the chances of getting employment in India.

Result: For the first time in four decades, Indian men are opting out of the education system – the share of young men withdrawing from education citing household income needs has jumped from 58% to 72% in six years.

Investment implications: As India deals with a major structural challenge in the labour market, there are two ways in which you can protect your wealth. You can invest with us in our cost-efficient & tax-efficient global funds with ticket sizes starting from Rs. 4.5 lakhs. OR you can invest with us in our domestic portfolios of clean, well-managed high quality Indian companies with ticket sizes starting from Rs. 50 lakhs.

For four decades, India sold its young people a simple promise: study hard, earn a degree, land a salaried job, climb. Repeat that often enough across a billion-plus people, and the country’s demographic dividend would quietly become an economic one. That was and remains the pitch that Indian investors make to retail investors across India and to institutional investors across the world.

In Breakpoint: The Crisis of the Middle Class and the Future of Work (2026), we argued that this promise has broken — and that it has broken along three fault lines that feed on one another: a scarcity of good jobs, stagnating wages, and an outdated education system at the root of it all, so outdated that going to university in India now significantly lowers your odds of gainful employment.

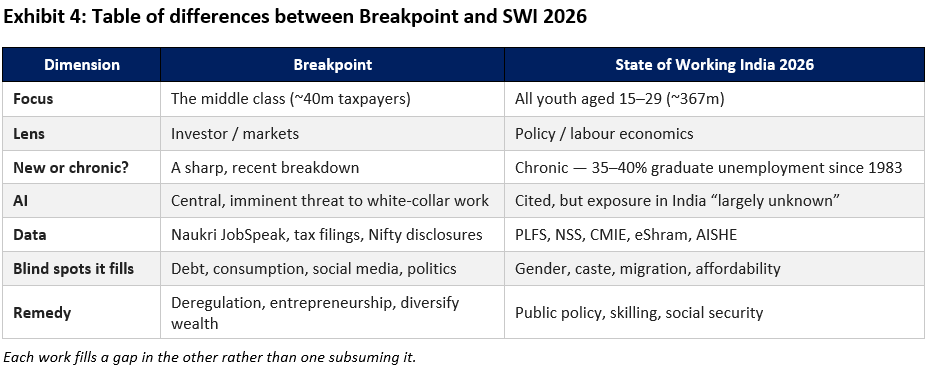

Within weeks of Breakpoint’s release in March 2026, Azim Premji University published its State of Working India 2026 (SWI) report. Working from an entirely different vantage point — four decades of official survey data, a policy lens, and the whole of Indian youth (~300–400 million) rather than the ~40 million middle-class taxpayers Breakpoint focuses on — the report flagged the very same problems.

There are differences of emphasis. SWI argues that graduate unemployment is not new at all: it has hovered at 35–40% since 1983, making this a chronic condition. We, in Breakpoint, place more weight on the last decade, where the deterioration in white collar job availability has been sharp and sudden in the past three years. But on the essentials, two very different teams at Marcellus and Azim Premji University, using very different data, arrived at the same place.

Which brings us to the questions both teams set out to answer: Is this slowdown in the Indian job market for graduates a structural breakdown or a passing phase? And if it is structural, why is it happening, who does it hit hardest, and what would actually fix it? Breakpoint answers these for the middle class and for Indian investors; SWI answers them for policymakers. The diagnoses in both publications rhyme for most part.

The shared diagnosis, across three fault lines

Both the book and the report, using different data and different logic, reach the same headline conclusion: this is structural, not a passing phase. Here is how each frames the three dimensions — and where they agree.

1. Job scarcity: too many graduates, too few jobs

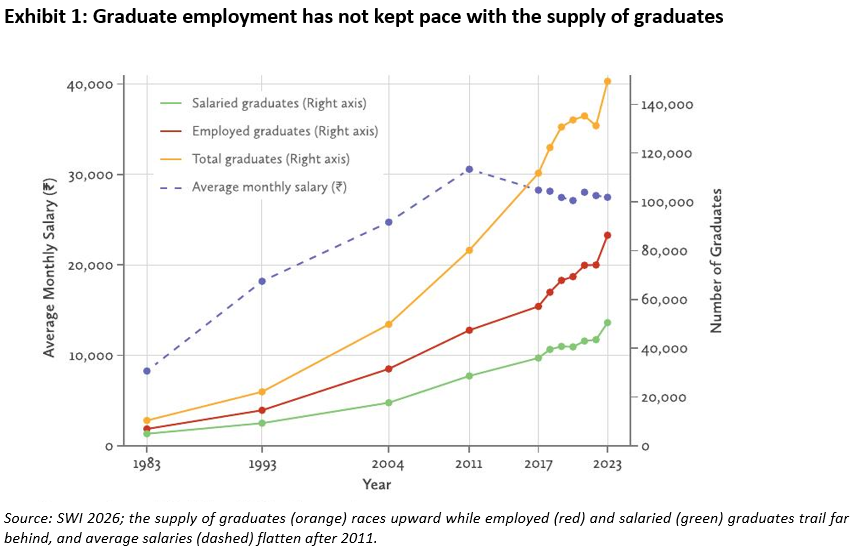

The arithmetic is brutal, and both publications hammer home the grim maths. SWI shows that between 2004 and 2023, India added roughly 5 million graduates a year, but the number of employed graduates rose by only about 2.8 million a year — and only about 1.7 million of those landed salaried jobs (implying that the remaining 1.1 million a year ended up in gig work of some sort). The result, in the SWI’s own words, is a situation of “too many graduates and too few jobs.” The chart above captures it at a glance.

In Breakpoint, we reach the same conclusion from the demand side. Using Naukri’s JobSpeak index of white-collar listings, we show that white-collar hiring grew about 11% a year in the decade to FY2020 and then collapsed to roughly 3% implying per-capita stagnation once you account for the swelling graduate pool. In simple English, India is producing educated jobseekers far faster than the economy is producing the salaried jobs they trained for.

2. Wage stagnation: real pay has gone nowhere

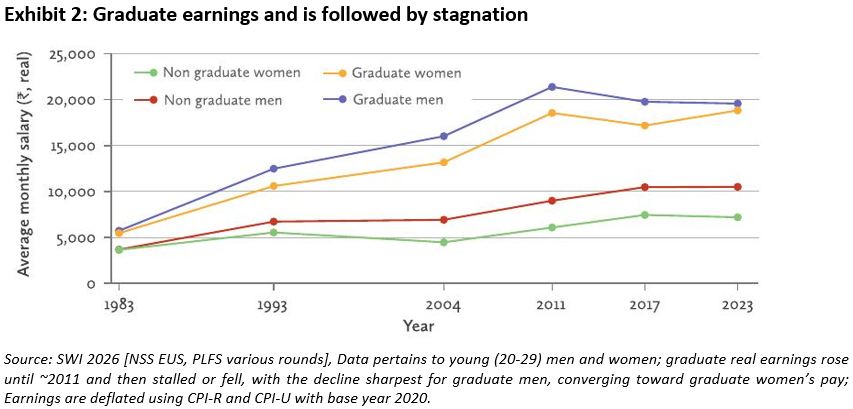

If demand for educated labour is weak, wages should stall in real terms (i.e. after adjusting for cost of living inflation). This is exactly what the data shows. SWI’s earnings series shows graduates’ salaries rising sharply until about 2011 and then declining, with the fall sharpest for graduate men (so sharp that male and female graduate salaries have converged in 2023).

In Breakpoint, we document the same stall from the other end. Salary growth at the Nifty-50 firms failed to beat inflation for eight years; average middle-class income barely budged over a decade (about ₹10.23 lakh to ₹10.69 lakh); and managers’ real wage growth halved, from 5.1% to 2.2% a year. Deloitte’s reading of data from the International Labour Organisation places India in the bottom quartile of 130 countries on real wage growth. For the educated — and especially educated men — real pay has declined for the better part of a decade.

3. Education and employment: the cruel paradox

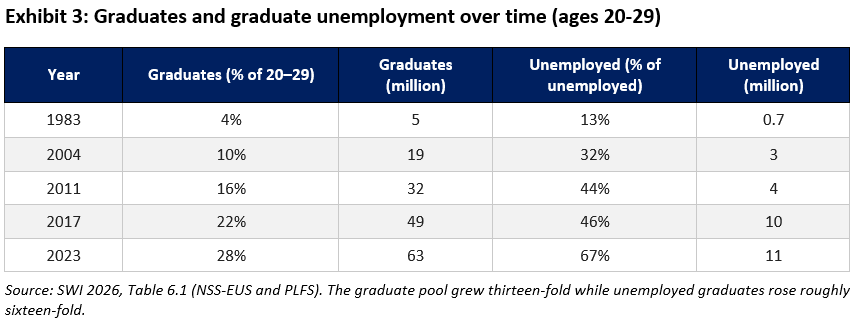

The cruellest twist in both publications is the adverse relationship between education and employment. In India today, unemployment rises with education. SWI puts graduate unemployment near 40% for the youngest cohort; Breakpoint cites 29% overall, about nine times the rate for those who cannot read or write. As the graduate pool has ballooned, the absolute number of unemployed graduates has exploded — from 0.7 million in 1983 to 11 million in 2023.

Both works trace this to an education system that has expanded enrolment rapidly while neglecting to upgrade the quality of education in line with the changes in the broader economy. Breakpoint dwells on collapsing graduate quality and a hard skills mismatch — only about 42–45% of graduates are judged employable. SWI documents the same erosion in vocational training — Industrial Training Institutes (it is) grew by nearly 300% between 2005 and 2025, but newer, mostly private institutes score far WORSE on quality. An education system focused quantity over quality is no longer producing what a modern economy needs — so more schooling now buys worse, not better, employment odds.

Where the book and the report part ways

Agreement on the diagnosis does not make the two works identical. They differ in revealing ways.

First, AI. Breakpoint treats artificial intelligence as a central, imminent force hollowing out white-collar work — a key reason we believe the job freeze is structural and will deepen. SWI is far more cautious: it cites the same emerging evidence (young workers in AI-exposed roles seeing a ~13% relative decline in employment) but stresses that India’s actual exposure is, as yet, largely unknown. Where we see a clear and present danger, the report sees an open question.

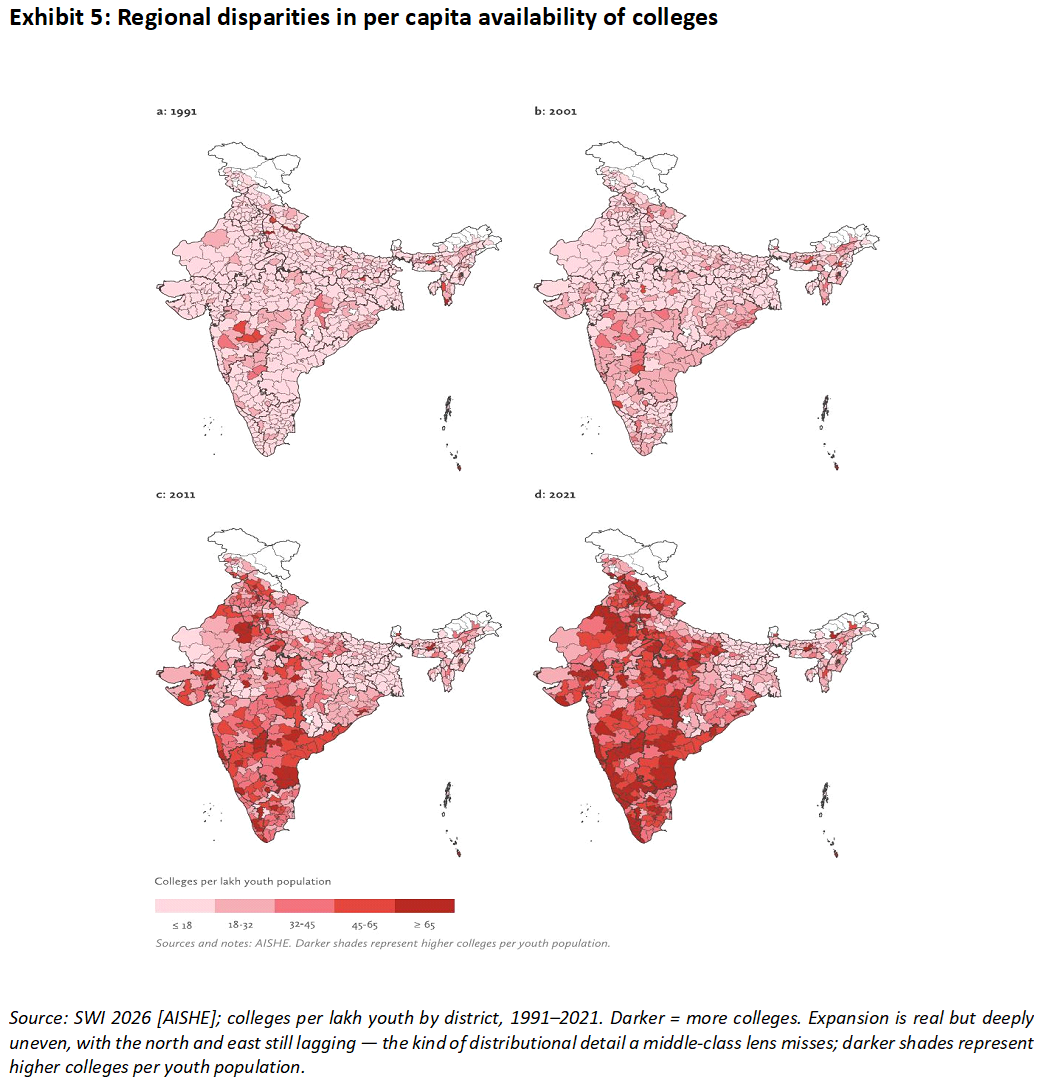

Second, the retreat from education itself.SWI flags something striking: young men are now pulling out of education. The share of young men in education fell from 38% in 2017 to 34% by late 2024, and the share citing the need to support household income as their reason for leaving rose from 58% to 72% (over the past 6 years). Set against SWI’s own mapping of how unevenly opportunity is spread across India’s districts (below), this looks like distress — and it fits the Breakpoint thesis uncomfortably well. When a degree no longer reliably pays off, rational families stop paying for one. Where SWI reads this withdrawal as a household coping strategy, we read it as confirmation that the education-to-employment compact has broken: free market agents are voting with their feet.

What this means for your career — and your money

Whilst diagnosis is relatively easy, navigation is hard. For India’s youth and for investors, two practical conclusions follow.

Be creative with your work, and disciplined with your money — not the other way around

As jobs and careers become less stable by the day, the old script — a steady salary that quietly compounds into wealth — is failing at both ends. You can no longer count on the job for stability, so the work itself has to become more inventive, more entrepreneurial, more adaptable. And because the income is shakier, the savings have to be handled with more discipline, not less.

Diversify beyond India — and into the factors that are exacerbating the job loss problem for India

As AI becomes better at run of the mill, clerical and back office jobs, jobs which were historically done by Indians at a cheaper cost for MNCs, the issues highlighted by SWI 2026 are only likely to become worse before newer opportunities emerge. As we argue in Breakpoint, this difficult adjustment period also called substitution effect, has coincided in India at a time when household savings are near multi-decade lows and household debt is high. Given that we are in Sankat Kaal, and protecting your wealth now also demands looking to geographies and assets which are beneficiaries of this change.

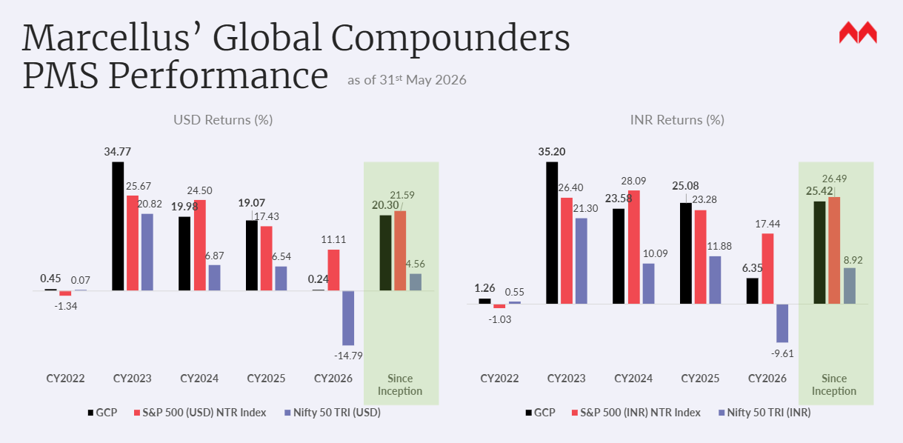

The practical response is to keep some of your wealth in dollar-denominated, globally diversified assets, specifically in those companies which are facilitating AI pickup, and we don’t just mean the well-discovered GPU and AI plays in the US, but everything in the value chain – the cooling systems, the power generation plays and so on required for data centres to thrive. Marcellus’s Global Compounders Portfolio (GCP), accessible from GIFT City with ticket sizes from US$5,000 (about ₹4.5 lakh), is one way in which investment in such high quality, global companies becomes possible. Its track record against the S&P 500 and the Nifty is shown below.

Marcellus’ Global Compounders Portfolio (GCP) PMS performance, as of 31 May 2026 (USD and INR returns). Past performance is not indicative of future results.

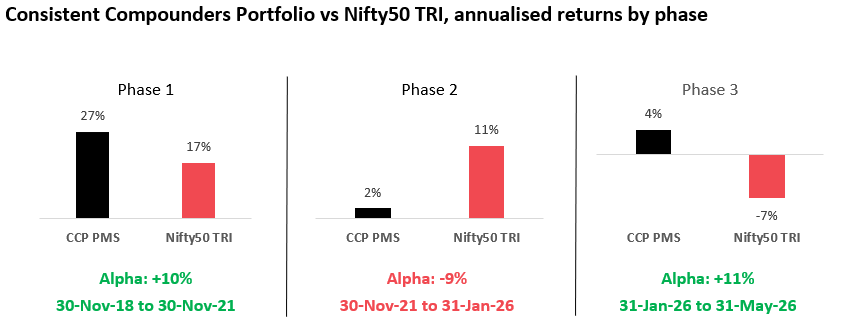

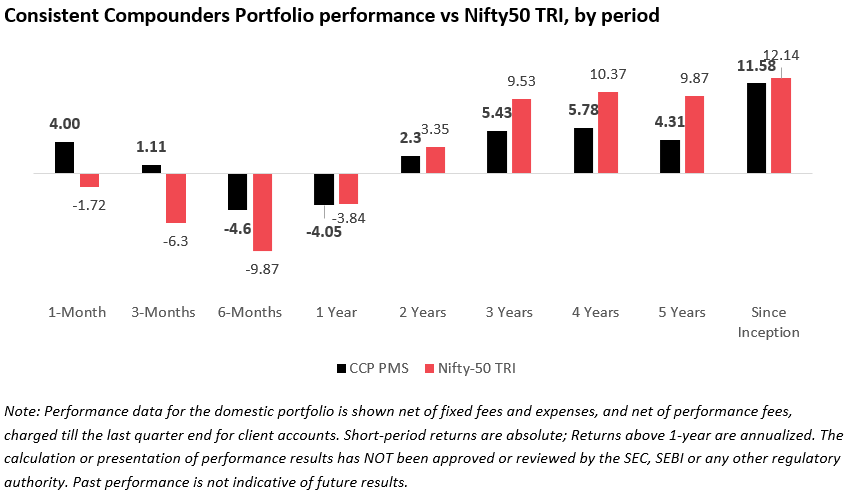

For those who prefer to stay invested at home, the answer is to own quality — companies with clean accounts and durable, compounding profit growth, such as Marcellus’s Consistent Compounders Portfolio — rather than the speculative froth that drove the post-Covid rally.

The Consistent Compounders PMS portfolio (CCP) is Marcellus’ flagship domestic offering with over Rs 1800 crores invested in this strategy. As you might know, we avoid naughty companies in sectors with high exposure to regulated or government-related activities. After four difficult years, CCP is beating the benchmark again (see chart below) largely because the investee companies are able to sustain profit growth through, both, good years an Sankat Kaal.

To learn more about these options, scan the code below.

Thanks,

Saurabh Mukherjea and Nandita Rajhansa

The authors of this note work for Marcellus Investment Managers (www.marcellus.in) and are the authors of “Breakpoint: The Crisis of the Middle Class & The Future of Work”.

The views and opinions expressed in this material are those of the writers/authors and do not necessarily reflect the official policy. This material is for informational and educational purposes only and should not be considered as financial, investment, or other professional advice. The inclusion of any book does not imply endorsement or recommendation by the writers or the publisher of this material.

Click here for details about our regulatory registration and licensing information.

Disclaimer:

The above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the International Financial Services Centres Authority (IFSCA) as a Fund Management Entity No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. All recipients of this material must before dealing and or transacting in any of the products/services referred to in this material must make their own investigation, seek appropriate professional advice. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer or an employee. This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.