Consistent Compounders Portfolio (CCP)

Despite volatility in the external economic and geo-political environment, Marcellus’ CCP companies have historically delivered consistency of revenue growth and profit growth. We expect this consistency to sustain in the foreseeable future as well. Additionally, over the last few months, we have seen a rise in competitive intensity through new entrants for many of the CCP firms – Asian Paints (Grasim’s expected entry), Bajaj Finance (Jio Financial Services’ expected entry), Titan (Aditya Birla has announced Rs 5,000 crores investment in jewellery retail), Dr. Lal Pathlabs (entry of e-pharmacies, pharma companies and hospital chains) and Page Industries (Van Heusen and several private equity backed players).

In our recent CCP newsletter (click here), we highlighted that in any vibrant, free market economy, firms that enjoy high RoCE will attract continuous waves of competition. Amidst high competitive intensity, while most firms will fall by the wayside, the Consistent Compounders are able to maintain their dominance due to their strong moats – built through prudent capital allocation and strategic decision making. Marcellus’ research process continuously assesses competition threats via a two layered framework focusing on: (a) the structure and strength of the current moat; and (b) the strategic decision making of the incumbent in response to competition. Firms that display any signs of ‘lethargy’ – whether in terms of strengthening their moats or in terms of responding to competition lose their place in our portfolio e.g. Abbott India in early 2022. However, for CCP stocks that are proactively strengthening their moats and defending their territory, we consider any temporary dislocation in market price vs. intrinsic value as an opportunity to increase our exposure in such businesses.

Going forward, as normalised revenues and profit growth (i.e. normalised for Covid base effects, commodity price base effects etc) are reported by our portfolio companies from 2QFY24 onwards, we expect to see the outcomes of initiatives taken by the management teams to strengthen their businesses during the last three years. During the first six months of FY24, we have witnessed a strong performance of Marcellus’ CCP portfolio as share prices catchup with underlying fundamental progression of the portfolio companies. Despite this, the gap between fundamentals of our portfolio companies and their share prices is over 25% currently. We expect this gap to narrow down significantly in the coming quarters.

Kings of Capital Portfolio (KCP)

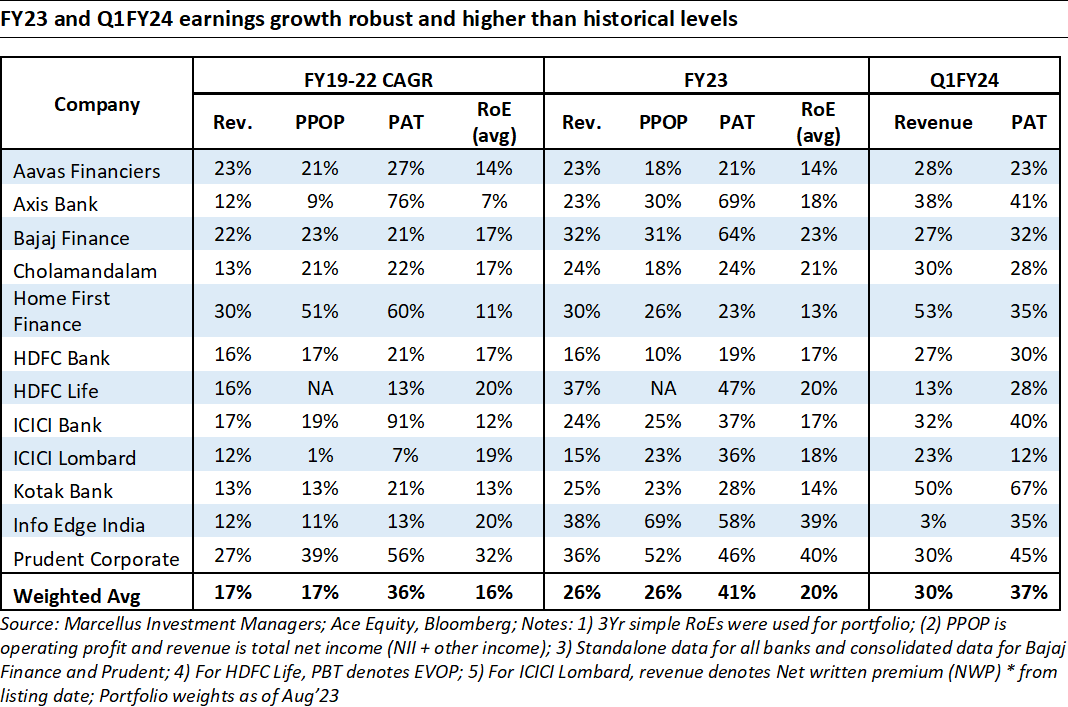

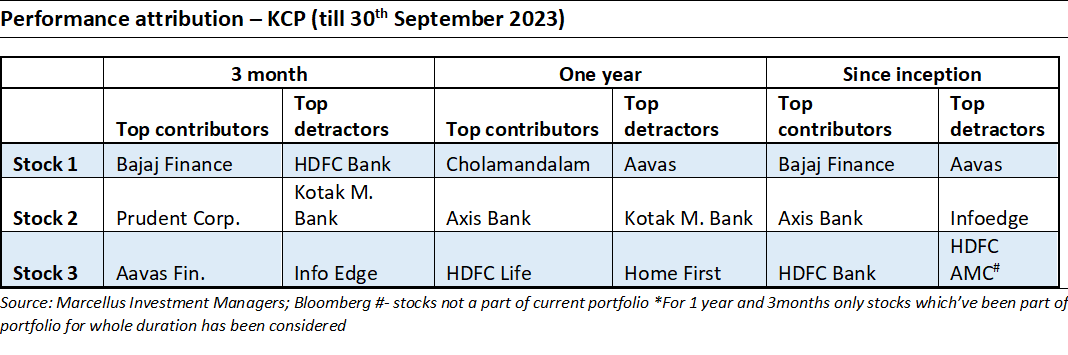

KCP portfolio companies have continued to deliver strong fundamentals with robust growth and asset quality which we expect to continue going forward as well. During Q1FY24, Kings of Capital portfolio companies continued their robust loan and profit growth performance with portfolio’s weighted average Q1FY24 revenue growth of 30% and weighted average PAT growth of 37%.

Post the Q1FY24 results, the industry data and pre-quarter result updates suggests strong traction on credit demand as well as steady growth of the insurance industry. Relevant insights and data points from September for KCP investors are as below:

- RBI’s disclosure on banking sector credit growth suggests 15% YoY credit growth for the banking industry and 13% deposit growth. While deposit growth continues to be a constrain for the banking industry, the gap between loan and deposit growth has been narrowing through this financial year.

- Bajaj Finance reported a ~33% YoY loan growth in its pre-quarter result update for the quarter ending Sep, 2023. This was accompanied with solid traction on deposits as it reported 40% YoY deposit growth in what has been a tough environment for the rest of the sector on garnering deposits.

- After a disappointing Q1FY24 on deposit garnering, HDFC Bank reported solid incremental deposit addition of Rs. 1.1 trillion in its pre-quarter update for Q2FY24. If HDFC Bank is able to continue this over the next couple of quarters, it will be able to put to rest the biggest uncertainty of the merger and focus on extracting synergies out of the merger.

- The general insurance industry has grown at a healthy 15% for the first half of the financial year while ICICI Lombard has grown at 18% during the period. We believe ICICI Lombard can further accelerate market share gains if irrational pricing and competition in the motor insurance segment reduces.

- The private life insurance industry reported ~12% annualised premium equivalent growth for the first half of the financial year while LIC reported a 11% de-growth leading to the overall sector growing at ~1%. HDFC Life grew ~10% during vs. earlier expectations of no/ negative growth due to the adverse taxation of guaranteed return policies.

- During the past month, our interactions with bankers, large loan sourcing agents and other financial intermediaries suggests that there is unabated credit demand across all segments (housing, personal loans, vehicle loans, SMEs etc). As long as companies in our portfolio are watchful of risks and prudent in their underwriting decisions, we continue to be well positioned for 20%+ earnings growth at the portfolio level.

There have been no additions/ deletions to the portfolio during YTDFY24.

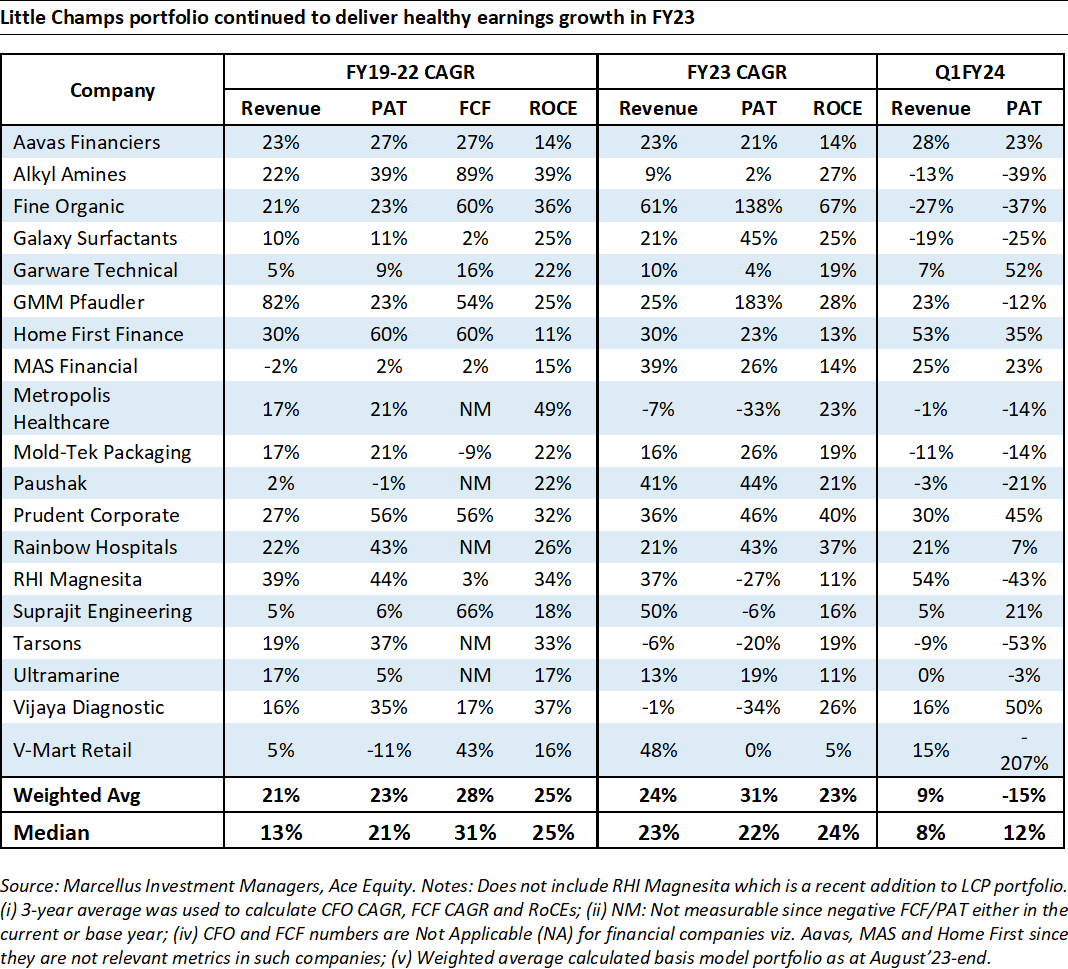

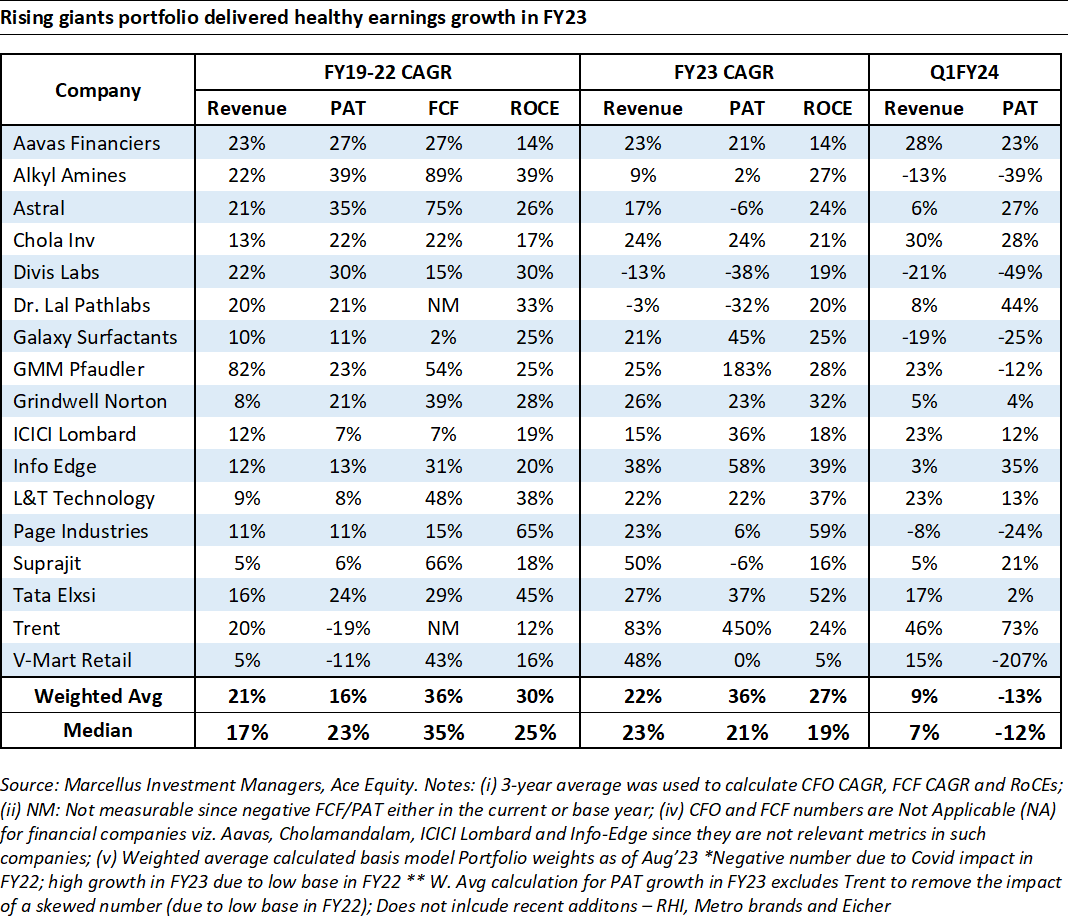

Little Champs portfolio (LCP) & Rising Giants Portfolio (RGP)

We expect the earnings trends seen in 1QFY24 for the Little Champs (LCP) and Rising Giants portfolios (RGP) to continue in 2QFY24 as well i.e. continued healthy earnings trends for the financial companies viz. Aavas, MAS Financial, Home First and Prudent Corporate in LCP and Aavas, Cholamandalam in RGP. On the other hand, helped by normalisation of the YoY base (devoid of Covid-19 related revenues), we expect Dr Lal Pathlabs, Divis Laboratories (both RGP companies) and Vijaya Diagnostics and Metropolis (in LCP) to see better YoY earnings trends vs the most recent quarters. On the flip side, the stocks in the chemicals space (Alkyl, Galaxy – in both LCP and RGP and Ultramarine and Fine Organics – in LCP) are likely to continue witnessing muted earnings due to adverse global demand-supply dynamics.

For both the portfolios, beyond the near- term headwinds we don’t see any structural concerns in the industry or the portfolio companies. The high level of reinvestments in FY23 and recent years (click on Aug’23 update) has provided enhanced visibility on the earnings performance for the portfolio over the next 3-5 years.

Changes to the Rising Giants portfolio:

We have made the following additions to the Rising Giants in the month of September 2023:

1. Metro Brands Limited:

Metro Brands Limited (MBL) is the one of the largest and fastest growing Indian footwear retailers with a revenue and earnings CAGR of 15% & 20% respectively over FY18-23. MBL is the most efficient footwear retailer in India as evidenced by store level ROI of ~60-80% which is almost twice as good as other footwear retailers despite the challenges in managing close to 6,000 to 8,000 SKUs per store across ~750 stores.

MBL’s competitive advantage is promoters’ art in buying & merchandising which comes from decades of hands-on experience along with a Theory of Constraints based automated replenishment at the store level to bring in efficiencies, decades old strong vendor relations who MBL favorable terms in new designs and payment cycles, and a unique incentive structure at the store level (80% pay is variable) which ensures store staff has high skin in the game to offer best customer service and give right inputs to buying & merchandising team at the HO. MBL’s proven track record of running the most efficient footwear business in India makes it the platform of choice for global brands entering India. While MBL started as a standalone store in 1955 under the name ‘Metro Shoes’, as launched multiple formats like: – Mochi (started in the year 2000 to cater to fashion footwear); – Walkway (started in the year 2009 to cater to value segment); – Crocs EBOs started in the year 2016 with MBL having Right Of First Refusal for offline Crocs stores and today running 80-85% of Crocs stores in India. – In 2022, MBL was awarded as licensee of the UK based FitFlop brand in India. – Recently the firm has acquired licensing rights for the brand ‘Fila’ in India to cater to the sneakers & sports shoe segment. Across its 5 brands, MBL mainly caters to the formal & casual segment of the market with aspirational product offering as evidenced by ASP of ~Rs1600-1700.

2. Addition of RHI Magnesita India Limited:

RHI Magnesita India (RHIM India) is the Indian subsidiary of RHI Magnesita (RHIM Global), a global leader in manufacturing & servicing of refractories with ~30% market share (ex-China). Refractories are non-metallic material having very high melting points enabling its usage as an internal lining in furnaces, kilns or any other vessels in the Metal, Cement and Glass industries.

Our key investment thesis in RHI Magnesita India revolves around the following points:

- Highly critical nature of refractories: Even though refractory accounts for only 2-3% of the overall cost, without refractories the customer’s plants cannot commence production. Additionally, refractories go through general wear and tear and hence need to be replaced at regular intervals, which is a very tedious process and entails plant shutdowns which may take as long as a day. Given the low-cost but critical impact of refractories, a customer demands products with the highest quality and longest life, thereby reducing the downtime risks.

- RHI’s Quality and R&D focus: RHIM India’ leadership in the Indian refractory market is underpinned by its superior product quality. This superior product quality is a result of RHIM Global’s high focus on R&D (1700+ active patents) and ability to continuously come out with better quality products that have longer lives. Our channel checks suggest that RHIM India is a dominant player in the refractory industry with 40%+ market share in the Basic Oxygen furnace + Laddle segments.

- Significant reinvestments by RHIM India in the recent years: In the last 5 years, RHIM India has been on an acquisition spree wherein it has added various flywheels and gained new capabilities. For instance, by merging all the subsidiaries of RHIM Global into RHIM India (listed entity), RHIM Global has aligned its interest with that of the minority shareholders. Similarly, the Dalmia acquisition has further fortified RHIM India’s moat through access to an extensive manufacturing base as well as facilitating entry into the Cement/Industrial and Blast Furnace refractory segments.

- Eicher Motors Limited:

Eicher Motors (EML) is an Indian automobile company housing two brands under its fold: Royal Enfield (catering to the Premium motorcycle segment) and VECV (catering to Trucks and Buses segment). Our key investment thesis in Eicher Motors revolves around the following points:

- Premiumisation of Indian 2Ws: Rising income levels & financing penetration alongwith customer aspirations are likely to drive premiumisation of the Indian 2Ws and Eicher Motors is expected to be a key beneficiary of the same. In late 2000s, Eicher Motors, with its Royal Enfield brand, revolutionised the premium motorcycle market in India by launching its famous ‘Classic 350’ motorcycle in 2009. Thereafter, Eicher Motors, cemented its initial success by swiftly expanding its distribution network from 250 dealer points in FY12 to 2000+ dealer points in FY23 and at the same time launched various new models in the premium segment over the last 10 years, viz. Bullet 350, Himalayan, Meteor 350, etc. Consequently, from FY13 to FY23, Royal Enfield sales have grown 6x from 122,000 units in FY13 to 734,000 units in FY23 in the domestic market.

- Strong Competitive advantages built around the Royal Enfield Brand: Over the years, various players have tried to enter the Premium Motorcycle segment. However, Royal Enfield has remained relatively unscathed due to the following competitive advantages:

- Aspirational appeal of the brand: Royal Enfield motorcycles have been well ingrained in Indian society with the brand gaining a cult-status in the riding community. The company is monetising this loyal base to the fullest by not just selling motorcycle but also by selling various non-motorcycle components such as apparel and equipment.

- Dealer Viability as a barrier for new entrants. Premium motorcycles/vehicles require a different distribution set-up to provide a premium customer experience to the end customer – a motorcycle enthusiast catering to the customer, premium quality store lighting and layout, etc. Thus even if a conventional peer enters this segment, they still need to set up a distribution network from scratch. Further, existing dealerships of established OEMs (incl. Royal Enfield’s) generate majority of their income by servicing the vehicle whereas margins earned on motorcycle sales are only able to cover the day to day running costs of the dealership. Since servicing income is not available to a new distribution channel, setting up a new dealer network is extremely difficult even for existing OEMs.

- Replicating India’s growth story in International markets: Since the last 5 years, Eicher Motors has been focusing on the exports market where its strategy is clear to follow the Indian template of creating aspiration and building a loyal customer base in the exports market. Company has done extremely well on the exports front where it has increased volumes from less than 5k units in FY16 to over 1lakh units in FY23. With many markets still available for Royal Enfield to tap, there is immense scope for further growth in the Exports market.

- Healthy market share gains for VECV segment: Eicher Motors has a JV with Sweden’s AB Volvo – Volvo Eicher Commercial Vehicles Limited (VECV), wherein Eicher holds 54.4% in the JV. Similar to the motorcycle portfolio, Eicher has done well in the Trucks and Buses segment as well by launching new products (viz. the Pro Series) as well as expanding its distribution network. Resultantly, company has in the last 5 years, increased its market share in light and medium duty trucks from 29% in FY19 to 32% in FY23 and from 4% in heavy duty trucks in FY19 to 8% in FY23.