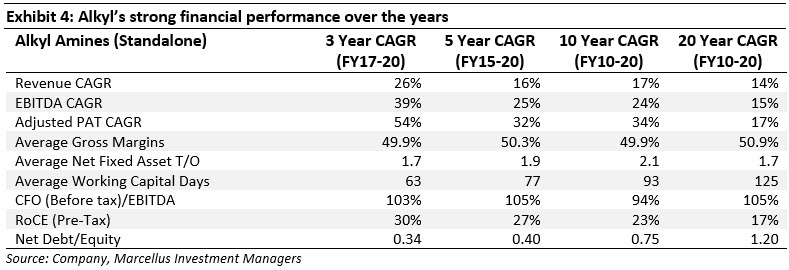

| This month we place the spotlight on Alkyl Amines, a leading manufacturer of aliphatic amines – a key ingredient in the pharma and chemical industries. Over the last ten years (FY10-20), Alkyl has delivered earnings CAGR of 34% with an average pre-tax RoCE of 23% (these numbers look even better for the last 3 and 5 years). The key factors behind Alkyl’s success have been: (a) its R&D strengths led by its technocratic top management and well-established R&D team which has enabled Alkyl to develop ~100 SKUs, nearly 4x the closest peer, as well as undertake product innovations like Acetonitrile; (b) its unwavering focus on the core business resulting in timely deployment of new capacities and identification of new product opportunities; and (c) significant entry barriers in the aliphatic amines industry, such as high capital costs, alongside long lead times in obtaining government & customer approvals.

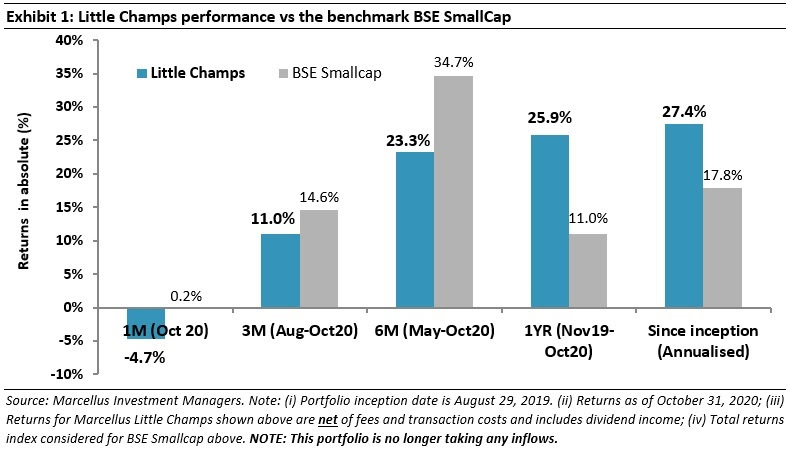

Performance update of the Little Champs Portfolio

At Marcellus, the key objective of our Little Champs Portfolio is to own a portfolio of about 15-20 sector leading franchises with a stellar track record of capital allocation, clean accounts & corporate governance and at the same time high growth potential. While we intend to fill our portfolio with winners, we want to be sure of staying away from dubious names where we are not convinced about the cleanliness of accounts or the integrity of the promoters (even though business potential may sound promising) as the fruits of company’s performance may not get shared with minority shareholders. We intend to keep the portfolio churn low (not more than 25-30% per annum) to reap the benefits of compounding as well as minimize trading costs.

The Little Champs Portfolio went live on August 29, 2019. The performance so far is shown in the below table.

Recent minority shareholder friendly corporate actions by a few Little Champs stocks

As discussed in our earlier newsletters, Corporate Governance plays a key role in generating returns especially in the small caps space. In this regard, we were positively surprised by the recent minority friendly corporate actions of a couple of Little Champs portfolio stocks.

A. Music Broadcast – issue of bonus non-convertible redeemable preference shares to minority investors

On October 22, 2020, Music Broadcast Limited’s (MBL’s) Board approved the issue of Bonus Non-Convertible Non-Cumulative Redeemable Preference Shares (NCRPS) to non-promoter shareholders ONLY. The bonus NCPRS shares shall be issued in the ratio 1:10; i.e. 1 Bonus NCRPS for every 10 equity shares held by non-promoter shareholders as on the record date to be fixed in due course. These bonus NCRPS with a coupon rate of 0.1% will be redeemed at Rs120 per NCRPS on expiry of 36 months from the date of allotment. The allotment is subject to approvals from the National Company Law Tribunal and other approvals that may be required.

We believe this is a very positive move for minority shareholders for the following reasons:

a. The issue of bonus NCPRS is only to the minority shareholders. In other words, parent Jagran Prakashan Limited which owned 74.05% of the Company as at September 30, 2020 will NOT be issued the bonus NCRPS.

b. Minority shareholders will be assured of Rs120 per NCRPS or Rs12 per equity share (given ratio of 1 NCRPS: 10 equity shares) three years from the date of the allotment of NCRPS. Rs12 per equity share is a sizeable amount given MBL’s current market price per equity share of Rs22.

c. NCRPS will be also be listed on the stock exchanges which gives minority shareholders an option to sell these NCRPS in the open market when needed.

d. MBL has total net cash of about Rs2,440 mn as at September 30, 2020. Given the non-receipt of approval from the Ministry of Information and Broadcasting for the acquisition of Reliance Broadcast Network Limited (RBNL), there had been opacity surrounding the use of this cash which drags down the overall return ratios of the Company. This opacity will be addressed to a significant extent through the issue of NCRPS which will consume around Rs1,080 mn of MBL’s cash three years down the line. At the same time, despite cash payouts towards NCRPS redemption, MBL will continue to have strong balance sheet (existing net cash plus future free cash generation from the operations).

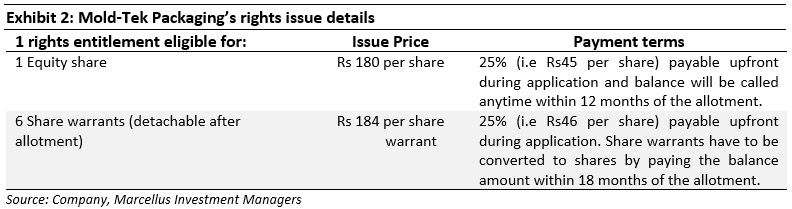

B. Mold-Tek Packaging – Rights issue – an opportunity to participate at a discounted price for all investors

Another portfolio company Mold-Tek Packaging Limited (MTP) has recently come up with its right issue to the tune of Rs713 mn. Every 50 shares owned by the eligible equity shareholders (who own the shares as on the record date October 22, 2020), will be entitled to 1 rights entitlement which comprises of the following:

|

We believe this is a positive move for minority shareholders for the following reasons:

a.The rights securities (shares and share warrants) have been priced at a significant discount to the current market price of MTP and all the shareholders get an opportunity to participate in the same.

b.The rights securities on allotment will be separately listed on the stock exchanges which creates a window of liquidity to the shareholders.

c.The payments for the rights securities have to be made in a staggered manner – only 25% upfront on application and payment of the balance upto 12 months from the date of the allotment in case of right shares and upto 18 months of allotment in case of share warrants. Again, this is a good move from the perspective of both the Company’s (seeking cash only when required) and shareholders (not blocking their funds when not required).

Stock in the Spotlight: Alkyl Amines

Company Background:

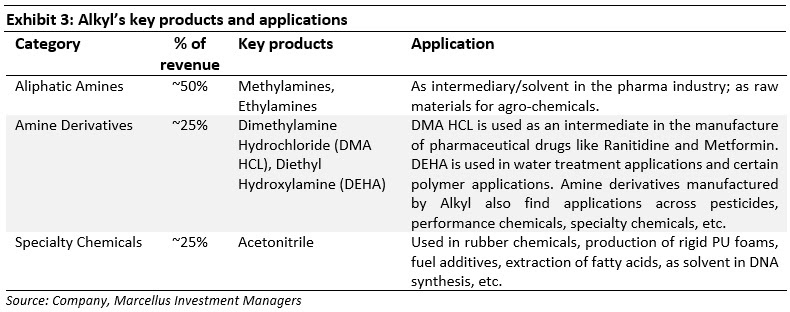

Incorporated in 1979 by Mr Yogesh Kothari, Alkyl Amines (Alkyl) is a leading manufacturer of aliphatic amines in India. Aliphatic amines are products derived from Ammonia (NH3) by displacement of H2 in the Ammonia molecule by other radicals (R) such as Methyl, Ethylene and Propanol. Apart from manufacturing basic aliphatic amines like Methylamines and Ethylamines, Alkyl has over the years also successfully diversified into value added products like amine derivatives and speciality chemicals. All these products find applications mainly as solvent and intermediates in end-user industries like Pharma (61% of total usage in FY20) and chemicals like agro (6%), water treatment (5%), foundry (4%), dyes (3%), specialty chemicals (6%) etc (Source: Alkyl Amines presentation – Click Here).Alkyl commercialised its first Ethylamines plant in 1982 with the help of a technology collaboration with Leonard Process Company, USA.During its initial years, the Company enjoyed significant success in Ethylamines emerging as its largest producer in India. In early-mid 1990s, the company also forayed into another important aliphatic amine – Methylamines – and amine derivatives such as Dimethylamine Hydrochloride (DMA HCL) and Diethyl Hydroxyl amine (DEHA). Over the years, the Company has continued to expand capacity in aliphatic amines as well as targeted new products particularly in amine derivatives and specialty chemicals. One of the big recent success for Alkyl has been its foray into Acetonitrile where it has emerged as the largest Indian player due to its unique manufacturing route. Alkyl also now generates close to 15-20% of its revenue from exports with Europe being a key export market.

|

|

|

Alkyl has maintained a healthy pace of growth in revenues and earnings over the years. The growth has picked up further in the last three years with new Methylamine capacities at Dahej coming on stream and significant increase in both the volume offtake as well as the pricing for Acetonitrile. Furthermore, the earnings growth has also been complemented by declining working capital days (helped in particular by a reduction in inventory levels) and consequent strong operational cash generation and improving return on capital ratios. |

Key success factors for Alkyl

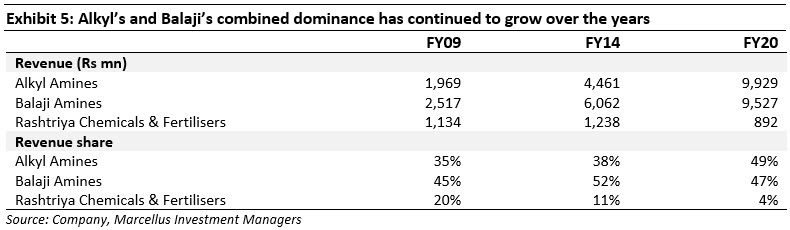

Balaji Amines and Alkyl Amines now account for >90% market share of aliphatic amines and amine-based derivatives in India with Rashtriya Chemicals & Fertilisers, the third largest player, commanding only single digit market share. Consolidation of market shares in amines industry is not only prevalent in India but in most other countries too – for instance aliphatic amines market is dominated by handful of players like BASF, Arkema, Eastman Chemical and Huntsman in USA and Europe.

As per our discussions with industry sources, the factors which have played a role in shaping the consolidated nature of the amines industry globally and more particularly in India are:

A. Inherent nature of the industry lends significant advantages to incumbents over a new entrant

Significant initial capital investments and long lead time in obtaining environmental clearances from the Government and product approvals from customers present formidable challenges for new entrants. This places potential entrants at disadvantage versus the established incumbents such as Alky and Balaji which have been able to build scale and establish strong customer relationships over the years. To be more precise, there appear to be four formidable barriers to entry into this sector:

a. Capital intensive nature of the business: Manufacturing amines that involves hazardous raw materials like ammonia is a complex process requiring significant technical know-how and initial investments. Fixed assets turnover in the industry ranges between 1.5-2x at optimum capacity utilisation but is significantly low at the initial stages of the ramp-up.

b. Requirement of environmental clearances: Given the hazardous nature of the industry, Governmental approvals are needed for putting up a new plant or even brownfield expansion beyond the licensed capacity of the existing plant. On an average it takes 1.5-2 years to obtain environmental clearances and any delays in obtaining the same (which can be quite frequent) increases the project costs further.

c. Lead time in getting approvals from the customers: Given the products go (as raw materials/intermediates) into end-user industries like pharma, the customers take time to derive comfort on the product as well as the manufacturing process. Furthermore, there has to be meaningful differentiation in either costs or product features for a customer to switch from an established vendor which again raises the ask for a new entrant.

d. Significant efficiencies from scale: The high capital investments involved make operating at meaningful capacity utilisation critical to generate respectable levels of profitability. Furthermore, there are a lot of efficiencies in operating as a continuous process rather than a batch process which again is dependent on having an adequate volume base.

B. The incumbents have been proactive in setting up capacities and identifying new product opportunities thus shrinking the space for new entrants in an already niche industry

Aliphatic amine is a niche industry accounting for less than 1% of the broader chemicals industry globally as well in India. After nearly 30-40 years of existence, Alkyl and Balaji put together generated revenues of Rs19.5 bn in FY20 indicating the niche size of the industry. Furthermore, both Alkyl as well as Balaji have been proactive in setting up amine capacities (sometimes ahead of the demand and thus getting adversely impacted in the interim) and capturing the benefits of the expanding end-user industry and opportunities in the value added products. For instance, Alkyl’s gross block has risen by nearly 1.8x over FY15-20. This has left little room for a new player to develop a credible scale in an already niche industry.

C. Alkyl’s clear strengths in R&D

Industry sources point towards strong R&D capability of Alkyl led by its technocrat top management as a key reason for Alkyl’s success.Mr Yogesh Kothari, the founder, Chairman and Managing Director of Alkyl Amines, is a chemical engineer from Institute of Chemical Technology (Mumbai) with nearly four decades of experience in the chemical industry. Mr Suneet Kothari, son of Mr Yogesh Kothari, joined the company in 2001 and is now designated as an Executive Director (commercial). He is a chemical engineer and chemistry/bio-chemistry graduate from Cornell University. The executive director (operations) Mr Kirat Patel is a mechanical engineer from IIT (Mumbai) and has been with the company since its inception. The top management also maintains connect with academicians of various universities such as Institute of Chemical Technology (Mumbai) and IIT (Mumbai) which has been a source of important product ideas over the years.In addition, the company has an established R&D team of ~50 employees with many senior members of the R&D team being associated with the company for more than 10 years now.Alkyl Amines has an institutionalised product development process. Every year, the company creates a list of around 20 new products. Within this list, a much smaller set of products are shortlisted for commercialisation. The various factors that are given consideration are: (i) The current and/or potential market size for the product; (ii) Whether Alkyl has or can have a technical edge in the product or its manufacturing process; (iii) Whether the products can have a diversified customer base rather than over-dependence on 1-2 customers; (iv) Whether there is fungibility surrounding the products – if the product demand drops, can another product be manufactured in the same facility; and (v) Whether the product can be scaled up globally. The top management, R&D and the commercial teams all play a part in the process. Once the products are identified, the R&D team plays a key role in developing the products to the commercial production stage. This process has enabled Alkyl to now scale up to nearly 100 SKUs, nearly 4x the nearest peer.The Company R&D’s team not only focusses on the products but also on the process improvements and developing in-house process technologies. While the Company initially relied on outside technology for commissioning the plants, over the years it has developed strong in-house engineering capabilities which has helped it bring down the capital costs significantly.Alkyl’s success in Acetonitrile through unique manufacturing process

Acetonitrile has been an important success for Alkyl in the recent years. The key applications for Acetonitrile are in rubber chemicals, production of rigid PU foams, fuel additives, extraction of fatty acids, as solvent in DNA synthesis, etc. The common route for manufacturing Acetonitrile is its generation as a by-product during the Acrylonitrile (ACN) manufacturing process. ACN is used for making acrylic fibres (which is used for home textiles, apparels) and Acrylonitrile Butadiene Styrene (ABS) polymer (which is used for manufacturing plastic for automobiles and consumer durables).However, Alkyl came up with a unique synthetic route of manufacturing Acetonitrile using acetic acid and ammonia as key raw materials. The product was commissioned by Alkyl in FY2012. While the product did not take off immediately, there has been marked change in the fortune of the product in the last 2 years. This has been mainly on account of decline in automobile production (due to tepid demand) and consequent decline in production of Acetonitrile under the common ACN route. This created significant demand-supply mismatch for the product resulting in not only significant off-take for Alkyl’s Acetonitrile (which was manufactured under a different route as explained above) but also increase in prices. The price of Acetonitrile has more than doubled in the last two years. Alkyl has also been scaling up its Acetonitrile capacities contributing handsomely to Alkyl’s profits in the recent years. With automobile production gradually recovering, the supply of Acetonitrile could improve leading to some reversals in the current high prices. However, Alkyl’s route has gained recognition in recent years as a greener route which can help Alkyl sustain market share. Furthermore, with increased capacities (Alkyl is adding another 15,000 tons p.a. to its already existing 12,000 tons p.a.), Alkyl now has a shot at the global market.

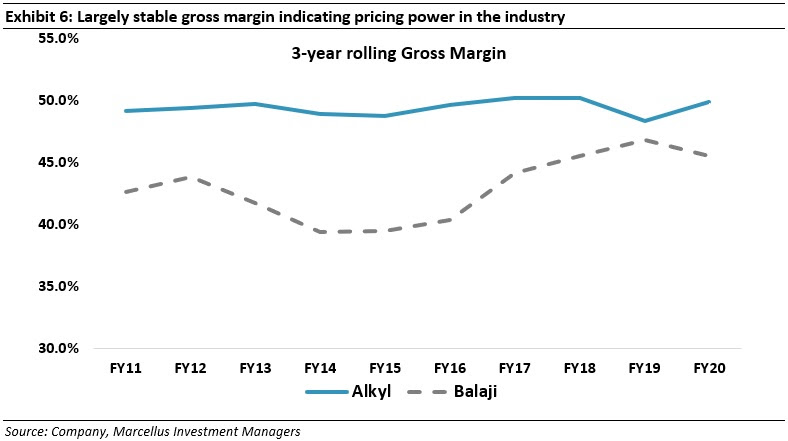

D. Relatively stable gross margin indicative of the pricing power

The key raw materials for the company are: (i) Methanol – mainly imported from the Middle East; (ii) Ethanol – sourced from domestic sugar industries and increasingly imported from USA; and (iii) Ammonia – largely sourced domestically being a very volatile product. As per our discussion with the industry sources, there is a good degree of pricing power in the industry even though there is a lag impact involved. Hence, despite significant volatility in the prices of methanol (crude based) and ammonia, Alkyl’s 3-year rolling Gross Margin has been fairly stable over a long period of time indicating the existence of strong pricing power in the industry.

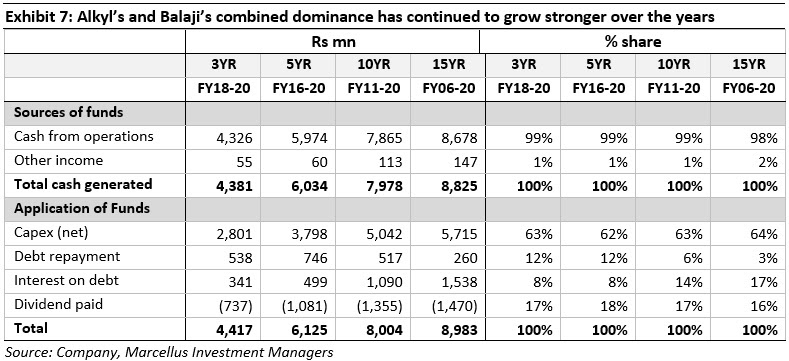

E. Prudent capital allocation

Alkyl’s capital allocation has been impeccable. The company has maintained an unwavering focus on aliphatic amines and its adjacencies (Acetonitrile is technically not an amine-based product but uses a key similar raw material ammonia and has somewhat similar manufacturing set-up). Furthermore, as mentioned in the preceding point, Alkyl has been proactive in setting up capacities as well as identifying and entering new products. The result is that the company has consistently high reinvestment rates (>60%) of its free cashflows. The cash not deployed in expanding capacities have been used to bring down the debt levels and payment of dividends to the shareholders.

|

|

Regards

Team Marcellus |

|