Alongside globalisation (see our July ‘21 newsletter), diversification has been an important feature of Little Champs’ growth strategy. Unlike what we see in the broader corporate world, Little Champs’s diversification strategies have been successful with new forays over the past decade now contributing in excess of 20% of revenues for most portfolio companies and RoCEs sustaining at healthy levels. So, why have Little Champs succeeded in an area where most of India Inc has failed? Key success factors are the ‘soft/related’ nature of diversification (strong linkages of the new businesses to the core business in terms of product, manufacturing process and/or distribution), measured capital allocation and effective organisational allocation of limited management bandwidth.

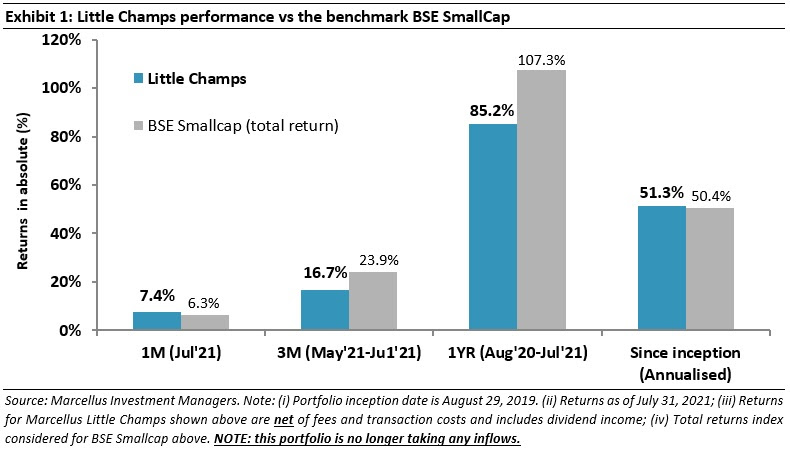

Performance update for the Little Champs Portfolio

At Marcellus, the key objective of our Little Champs Portfolio is to own a portfolio of about 15-20 sector leading franchises with a stellar track record of capital allocation, clean accounts & corporate governance and at the same time high growth potential. While we intend to fill our portfolio with winners, we want to be sure of staying away from dubious names where we are not convinced about the cleanliness of accounts or the integrity of the promoters (even though business potential may sound promising) as the fruits of company’s performance may not get shared with minority shareholders. We intend to keep the portfolio churn low (not more than 25-30% per annum) to reap the benefits of compounding as well as minimize trading costs. The Little Champs Portfolio went live on August 29, 2019. The performance so far is shown in the below table.

Diversification – Little Champs’ key strategy to mitigate growth challenges

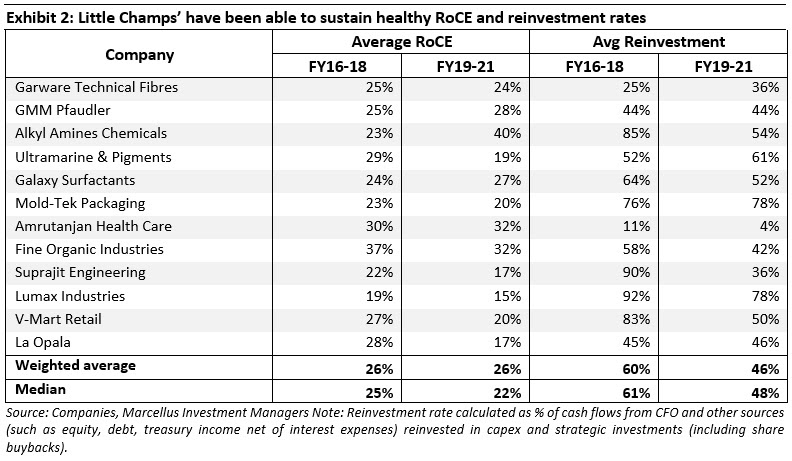

Little Champs with their deep-rooted competitive advantages deliver returns on capital employed (RoCE) substantially higher than their cost of capital. This results in strong operating cash generation for these companies. However, high RoCE and cash generation by themselves would not be of much use if the company is not able to find avenues to redeploy the surplus cash flows at the current high levels of RoCE. In this regard, Little Champs are an exceptional set of small cap companies which have been able to sustain a combination of high RoCEs and high reinvestment rates over long periods of time.

The performance shown in Exhibit 2 is despite: (i) the macroeconomic challenges of the recent years where economic growth has been weak; and (ii) the Little Champs operating in niche industries where growth becomes a challenge particularly once a company achieves a high market share. In our July 2021 newsletter, we mentioned that Little Champs have managed to sustain high growth rates (and profitably reinvestment their surplus cash) on the back of two broad strategies – globalisation and diversification. We discussed the globalisation strategy in detail in last month’s newsletter. We will focus on diversification in this month’s newsletter.

It may be noted that globalisation and more particularly diversification – as tools for driving growth – are not unique to Little Champs but have been used widely used across the corporate world. However, as is the case with globalisation, only a few Indian companies have been able to make a success out of diversification measured in terms of size, profitability, return on investment, etc. In fact, in our recently published blog (Link), we explained using Jim Collins’ ‘Five stages of decline’ framework that many companies, hitherto successful, fueled by hubris and arrogance pursue undisciplined diversification which ultimately leads to their downfall. Unfortunately, this is true for most companies as is visible in the high churn ratios of the benchmark indices like Nifty50 and BSE500.

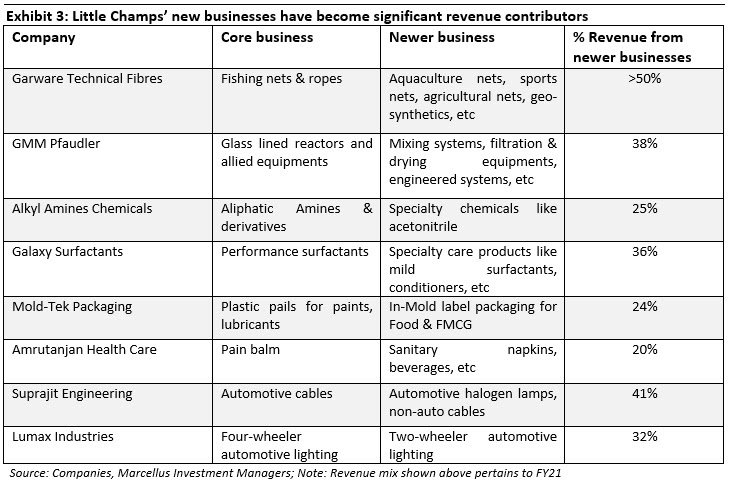

On the other hand, as can be seen in the below exhibit, most Little Champs’ diversification attempts have been broadly successful creating strong additional growth drivers for the companies over the past decade.

Some of the key success factors behind Little Champs’ diversification strategy are

A. ‘Soft’ diversification

“The hidden champions’ diversification attempts often cannot be clearly categorized according to the Ansoff matrix, and there is frequent overlap between the cells. We therefore talk about ‘soft’ diversification. ‘Soft means that the new units stay close to the traditional business, both in terms of technology and market.” – Hermann Simon in ‘Hidden Champions of the 21st Century’.

A key result for failure of most diversification attempts by Indian companies have been investing the cashflows of the core business into businesses which has nothing to do with the core business or where the competitive advantages of the core business cannot be leveraged to drive the new business. In contrast, most Little Champs have diversified into segments which have strong linkages to the core business either in terms of product, manufacturing process and/or distribution.

Some examples of ‘related’ diversification by Little Champs are:

- Garware’s success in salmon aquaculture nets comes on the back of the firm’s polymer engineering expertise and a strong understanding of fishing industry ecosystem gained through decades of experience in the traditional core fishing nets business.

- In FY2021, GMM Pfaudler derived close to 38% of revenues from non-glass lined equipment (GLE) businesses like filtration & drying, heavy engineering, mixing and engineering systems compared to 15% revenue contribution a decade back (in FY2011). While acquisitions like Mavag have helped on the technology front, leveraging the GLE customers’ relationships in pharma & chemical industries has also played an important role in GMM’s success in these non-GLE segments.

- Another example is Alkyl’s diversification in acetonitrile which is not an amine-based product but uses similar amine-type manufacturing technology and a common key ingredient, ammonia. Efficient handling of ammonia, a highly volatile raw material, is one of the biggest entry barriers in the amines industry and this has clearly helped Alkyl market dominance in the manufacturing of acetonitrile.

While soft diversification or foray into adjacencies may not result in significant revenue build-up in the short term (as opposed to say a big-bang acquisition or diversification into a large unrelated business), it provides greater chances of success and sustainability in the long term due to: (i) the company is playing to its strengths by leveraging existing competencies; and (ii) as we explain in the next section, related diversification typically creates lower stress on the balance sheet and on management bandwidth.

B. Disciplined capital allocation

‘Soft diversification’ – as opposed to diversification into unrelated businesses – lowers the capital requirement/intensity. For instance, in Garware’s case, there is a high degree of fungibility in the manufacturing processes for nets used across different applications. A similar point can be made with Lumax’s foray into the 2W lighting business (vs its traditional core 4W lighting business).

However, irrespective of related or unrelated diversification or even acquisitions, most Little Champs have been very disciplined in terms of allocating capital to their newer growth areas. Some examples are:

- Suprajit has made two relatively large acquisitions outside its core automotive cables business in recent years by first acquiring automotive halogen bulb maker Phoenix Lamps in FY16 for a total Rs2.72bn and then by acquiring US-based Wescon Controls, a non-auto cables player, for Rs2.75bn in FY17. While Phoenix Lamps and Wescon Controls were relatively large acquisitions (in total they accounted for 58% of Suprajit’s FY17-end capital employed), we believe Suprajit took measured/prudent financial risks in the acquisitions due to the following reasons: (i) Suprajit’s pursued these acquisitions after reaching a reasonable size in its core business (consolidated networth stood at Rs2.42bn at FY15-end), healthy cash generation levels in its core automotive cables business (Rs0.7 bn in FY15) and comfortable debt-equity levels (0.3x at FY15-end); and (ii) Phoenix and Wescon were not distressed companies but profitable franchises at the time of their acquisitions with sufficient cash generation to fund their future investment needs without creating a drag for the core automotive cables’ cash flows.

- GMM Pfaudler recently acquired a 54% stake in Pfaudler’s International business (the balance 26% has been bought by GMM’s promoters Patel family and 20% has been retained by the private equity firm, DBAG). This deal would seem ambitious when one looks at the relative size of the entities – Pfaudler International generated proforma revenues of Rs13,740mn in FY21 compared to GMM’s existing business of Rs7,572mn. However, we do not see any material stress on GMM’s balance sheet due to the acquisition. After factoring in net debt on Pfaudler’s international books and debt taken by GMM to fund the acquisition, GMMs’s consolidated net-debt equity (including non-controlling interests as part of equity) has increased to 0.38x at March 2021-end or Rs2bn consolidated net debt which appears quite manageable given GMM’s existing business (India + Mavag) generated adjusted EBITDA of Rs1.67bn in FY21 and for the same period Pfaudler International generated proforma EBITDA of Rs1.2bn.

- Amrutanjan’s foray into sanitary napkins (Comfy brand) has added additional revenue growth drivers to the company (Comfy contributed close to 15% of revenues in FY21). Whilst it can be debated whether sanitary napkin is a related or an unrelated diversification (the company’s core business is pain balms), Amrutanjan has relied on an outsourcing production model for Comfy resulting in negligible capital investment. In fact, Amrutanjan has seen its return on invested capital (RoIC) expand massively in the recent years on the back of its asset light business strategies.

C. Organisational structure to manage newer businesses

One of the key reasons for the failure of most diversification pursuits is the shift of management bandwidth from strengthening the core business to managing the non-core business. This ultimately results in a weakening of the core franchise and a decline in its pricing power & returns. On the other hand, suitable management bandwidth allocation with sufficient delegation of responsibilities and fair incentivisation have been success factors for Little Champs in managing the new businesses. We have discussed this aspect of Little Champs which is also relevant for their globalisation strategy in detail in our July 2021 newsletter. In summary, as Little Champs’ businesses have extended beyond one product segment and/or one market, we have seen the promoters increasingly leaving the role of execution and day to day affairs to the management team and instead focusing on the key strategic and capital allocation decisions of the firm. As William Thorndike Junior explains in his outstanding book “The Outsiders”, that is exactly what the promoter needs to do for shareholders to reap healthy returns.

More details on some of the specific companies discussed above can be read in in our earlier months’ newsletters – Garware (Link), GMM Pfaudler (Link), Alkyl Amines (Link), Suprajit Engineering (Link), Amrutanjan (Link) and Fine Organics (Link). All of these companies are part of Marcellus’ Little Champs portfolio.

|

|

Disclaimer: Copyright © 2026 Marcellus Investment Managers Pvt Ltd, All rights reserved

Note: the above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer or an employee.

This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.

Regards, Team Marcellus

If you want to read our other published material, please visit https://marcellus.in/pms-investment-blog/

Copyright © 2026 Marcellus Investment Managers Pvt Ltd, All rights reserved