| Marcellus’ Little Champs portfolio witnessed revenue growth of 31% YoY and PBT growth of 51% YoY in 4QFY21 (vs 13% and 36% respectively in 3QFY21). More impressively, the Little Champs companies more than DOUBLED their average free cash flow in FY21 (despite continuing to invest heavily in expansion) thanks to cost controls, working capital management and a muted FCF base of FY20. The net outcome, is that as we gradually emerge from the Covid-19 lockdown, the Little Champs are much better positioned to gain market share (courtesy their superior balance sheet strength) and much better placed to weather the near-term disruptions emanating from future Covid waves and commodity price inflation.

Performance update of the Little Champs Portfolio

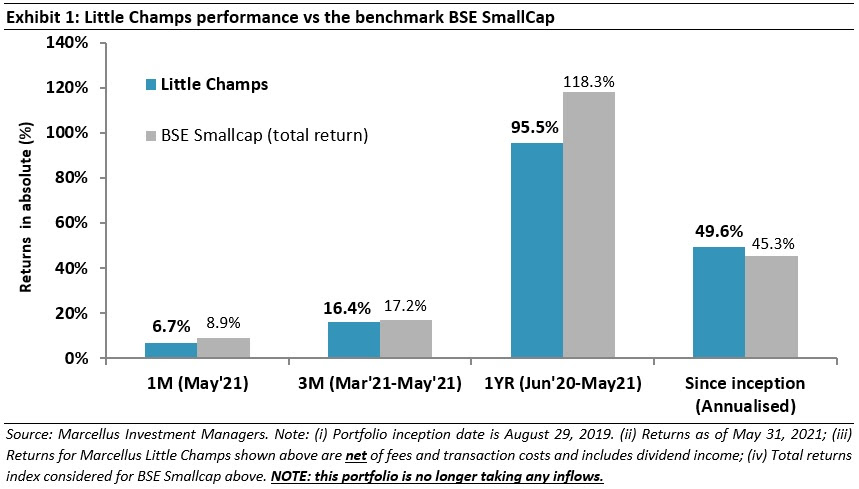

At Marcellus, the key objective of our Little Champs Portfolio is to own a portfolio of about 15-20 sector leading franchises with a stellar track record of capital allocation, clean accounts & corporate governance and at the same time high growth potential. While we intend to fill our portfolio with winners, we want to be sure of staying away from dubious names where we are not convinced about the cleanliness of accounts or the integrity of the promoters (even though business potential may sound promising) as the fruits of company’s performance may not get shared with minority shareholders. We intend to keep the portfolio churn low (not more than 25-30% per annum) to reap the benefits of compounding as well as minimize trading costs. The Little Champs Portfolio went live on August 29, 2019. The performance so far is shown in the below table. |

|

Portfolio updates

We have exited from a couple of stocks in the recent months viz. PPAP Automotive and Music Broadcast. The sale proceeds from these exits have been re-invested in the other portfolio stocks basis our position sizing frameworks.

PPAP Automotive

We decided to exit from PPAP Automotive due to the following reasons:

- PPAP’s second largest customer viz. Honda Cars India Limited has been going through a rough patch in India over the last two years with its market share in the domestic passenger vehicle market plummeting from 5.4% in FY19 to 3.0% in FY21. The absolute sales volumes have declined from ~183k units in FY19 to about ~82k in FY21 prompting Honda to stop car manufacturing at one of its plants (Greater Noida) in India. Obviously, this has had an impact on PPAP with its revenues from Honda declining sharply over these last two years.

- PPAP to its credit has somewhat made up for Honda’s revenue loss through rising revenues from Maruti (courtesy supplying injection parts from its new Gujarat plant), increasing penetration in the two-wheeler segment and certain other customers. However, it seems that the Company is not able to make the same level of margin in these new businesses/customers. For instance, the Company’s standalone gross margin stood at ~43% in 2HFY21 vs 48.4% in 2HFY19 while generating 15% higher revenues in 2HFY21 vs 2HFY19. Given these margin challenges, we see the climb-back to 20% pre-tax RoCE (the Company generated 19% in FY19) to be a tough ask for PPAP.

Music Broadcast

Our exit from Music Broadcast (MBL) centered around the following reasons:

- Even pre-Covid-19, the radio industry has been going through a challenging phase due to a sharp drop in radio advertising by the Government, traditionally a major advertiser on the medium. As per MBL’s investor presentations, Government’s radio advertising volumes witnessed a YoY drop of 70% in FY20. This further declined by 34% YoY in FY21. Given the post-Covid fiscal situation, we could not see when and how the Government would re-emerge as a big advertiser.

- Owing to the Covid-19 uncertainties during the first wave in 2020, radio players took aggressive price cuts to push volumes to both the existing clients as well as to attract new clients to the industry. However, a fall-out of this seems to be structural decline in radio ad-yields as evidenced by 3QFY21 and 4QFY21 when volumes recovered (YoY positive volume growth) but realization were still down sharply YoY.

- MBL also faced a setback in its pursuit of RBNL with approval from the Ministry of Information & Broadcasting not forthcoming and subsequent cancellation of the deal. RBNL’s acquisition would have made MBL an undisputed leader in the radio industry helping it command greater pricing power, bringing in a complimentary set of radio channels while not putting undue stress on MBL’s balance sheet given its strong net cash reserves & healthy free cash generating business model.

- Finally, while we were conscious of impact of digital and online music streaming mediums on the radio industry when we bought MBL in the portfolio, Covid-19 seems to have accelerated this shift significantly. Ever growing free access to music on various internet mediums seems to be weaning away listeners from radio much quicker than we thought.

Little Champs end FY21 on a high note

Healthy recovery in revenues and earnings…

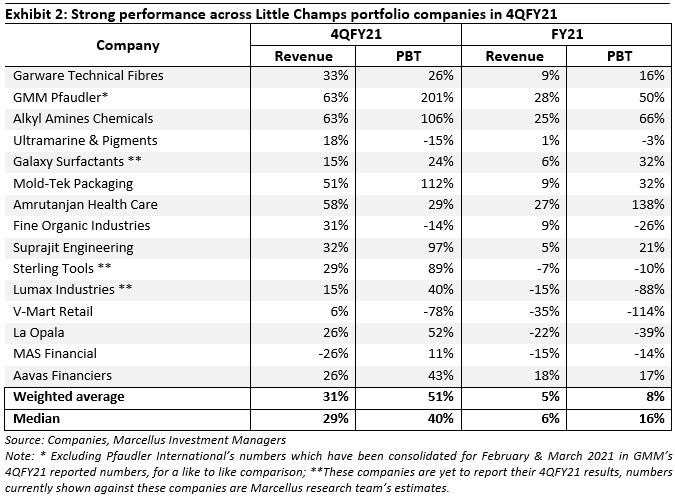

The recovery in the revenues and earnings for the Little Champs that began since 2QFY21 accelerated significantly in 4QFY21. At the weighted average level, the YoY revenue growth for 4QFY21 was 31% (vs 13% in 3QFY21) while the YoY growth in PBT was 51% (again much better than 36% seen in 3QFY21). The recovery in revenues and earnings have been helped by the fact that majority of the portfolio companies cater to resilient end-user industries like pharma, food, FMCG, etc. Secondly, most of our portfolio companies have witnessed market share gains against their weaker competitors (while FY21 numbers for some of the peers, particularly in the unlisted space is not yet available, management commentaries of the portfolio companies consistently point towards market share gains from peers). Thirdly, the YoY trend in revenues and PBT is also helped to some extent by a weak base of 4QFY20 (due to the imposition of the total lockdown in the country in the last few days of March 2020).

Helped by a robust 4QFY21, despite a washout in 1QFY21 (due to the first lockdown), the Little Champs portfolio has delivered weighted average revenue growth of 5% and PBT growth of 8% for FY21. In fact, the median PBT growth for the portfolio for FY21 is 16% indicating a broad-based earnings recovery across the portfolio stocks.

|

…complimented by a strong free cash generation

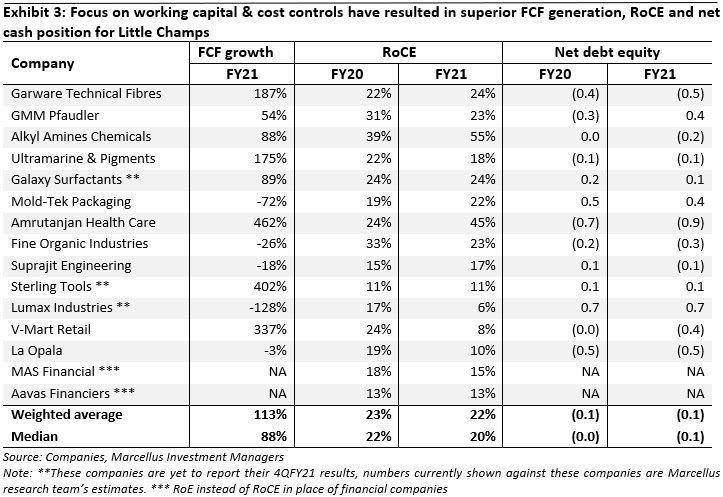

In addition to the recovery in the earnings highlighted above, the icing on the cake has been strong free-cash flow (FCF) growth recorded by the portfolio stocks in FY21. On a weighted average basis, the portfolio has delivered FCF growth of 113% for FY21 (median of 88% indicating again a broad-based FCF improvement across the portfolio stocks). This doubling in FCF comes despite our portfolio companies maintaining reinvestment rates at high levels. Besides focus on cost controls, working capital management has been a key focus of our investee companies to mitigate the Covid-19 impacts. This improved in working capital – contrasted with the stretched working capital at FY20-end as companies got stuck with high inventories and receivables due to the lockdown imposed during the first wave – has helped drive the doubling of FCF in FY21.

Investment implications – Little Champs on a much stronger footing now than pre-Covid-19

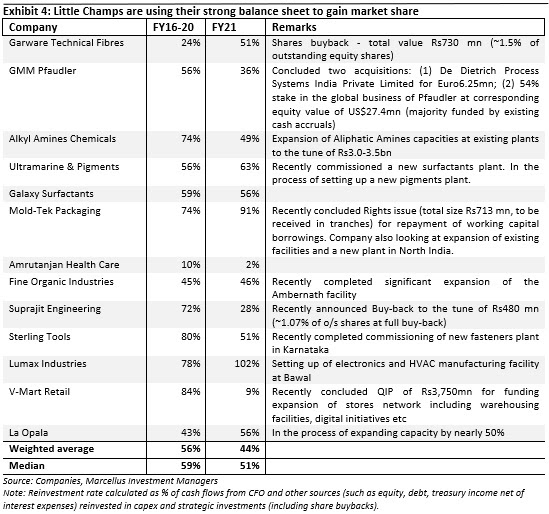

The result of the recovery in earnings alongside the strong cash generation witnessed through FY21 is that the Little Champs are well positioned to gain market share over the coming years courtesy their significantly superior balance sheet vs peers. In fact, the Little Champs are already putting their balance sheet into action as evident in weighted average reinvestment rate of about 44% in FY21. While this is lower than average 56% for FY16-20, it has to be viewed in the context of: (i) the lockdown in operations during a significant part of the year (particularly in 1QFY20), (ii) the strong operating cash generation of FY21 (described in the preceding section) which optically suppress the reinvestment rate % – please refer to the table above to see how we calculate the reinvestment rate; and (iii) in the case of one portfolio company viz. V-Mart Retail the reinvestment rate is also impacted by the Rs37bn equity raised through a QIP towards the end of the year. Clearly, the portfolio companies have stepped on the accelerator to gain market share by investing capital in strengthening their core business, expanding capacities or in some cases even buying out weaker peers as can be seen in the above exhibit.

We expect the Little Champs’ strong financial position to help them, both, weather the near-term issues surrounding the lockdown in 1QFY22 (induced by the second Covid-19 wave) and cushion the impact of the input price inflation which we are currently seeing. In fact, these adversities are likely to once again widen the gap between the Little Champs and their peers. As they cliché goes, “When the going gets tough….”

|

|

|

Disclaimer: Copyright © 2026 Marcellus Investment Managers Pvt Ltd, All rights reserved

Note: the above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer or an employee.

This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.

Regards, Team Marcellus

If you want to read our other published material, please visit https://marcellus.in/pms-investment-blog/

Copyright © 2026 Marcellus Investment Managers Pvt Ltd, All rights reserved