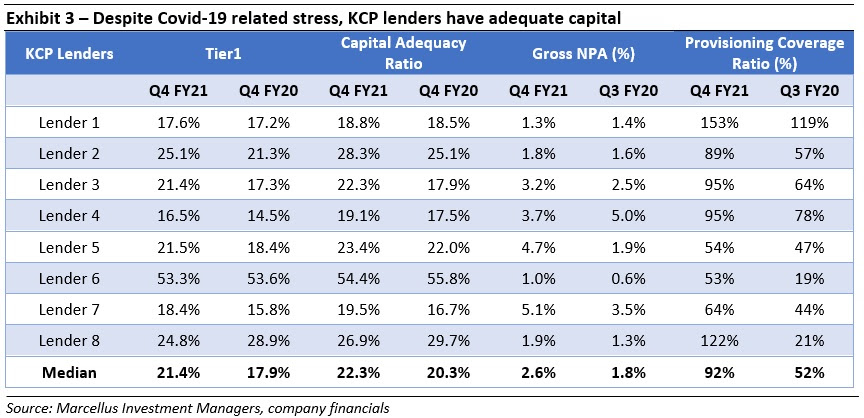

Over the past 15 months, the Kings of Capital (KCP) lenders have focused on broadly three aspects to counter the impact of Covid induced lockdowns and restricted economic activity: (i) augmenting collection capacity to sustain NPAs at manageable levels; (ii) preserving liquidity by raising debt/deposits at competitive interest rates; and (iii) maintaining healthy capital adequacy after making accelerated provisions for expected loan losses. These proactive measures have resulted in the Net NPAs of the KCP lenders staying at manageable levels of 1.1% vs. pre-Covid NNPA of 1.0% and the Tier-1 capital increasing to 21% in Q4FY21 vs. the pre Covid levels of 18%. This balance sheet strength of the KCP lenders will enable them to gain market share and capitalize on the revival of credit demand as the Indian economy recovers from the second Covid wave. This was visible during Q4FY21 when the KCP lenders saw an annualized loan book growth of 27% vs. banking sector credit growth of 13%.

Performance update of the live fund

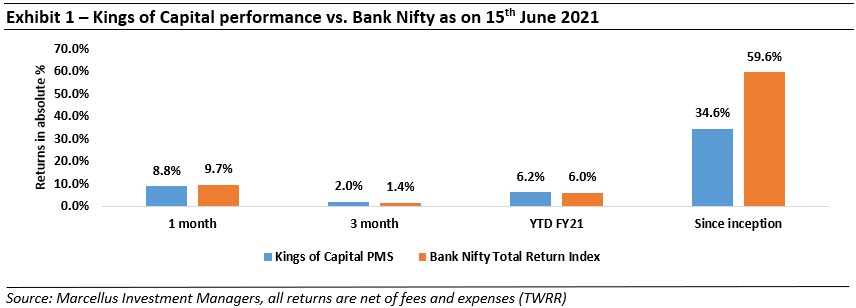

The key objective of our “Kings of Capital” strategy is to own a portfolio of 10 to 14 high quality financial companies (banks, NBFCs, life insurers, general insurers, asset managers, brokers) that have good corporate governance, prudent capital allocation skills and high barriers to entry. By owning these high-quality financial companies, we intend to benefit from the consolidation in the lending sector and the financialization of household savings over the next decade. The latest performance of our PMS is shown in the chart below.

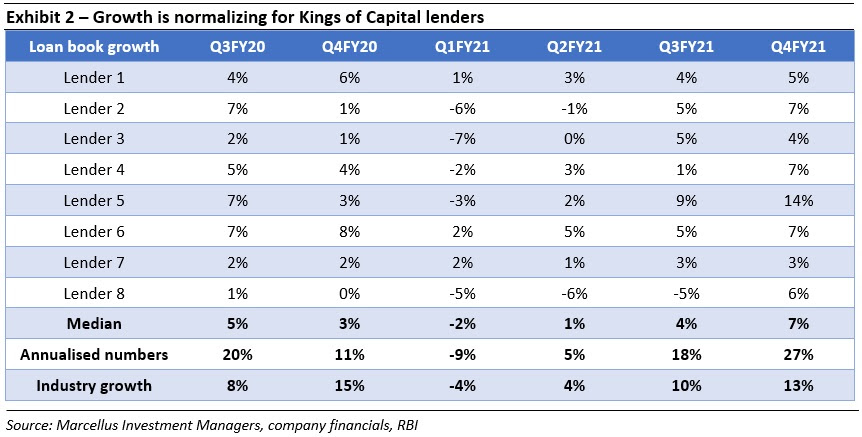

KCP lenders exceeded pre-Covid growth rates in Q4FY21

- Lenders maintained a conservative stance in Q1FY21 and Q2FY21: During the Covid 1.0 lockdown (Q1FY21), the KCP lenders remained conservative with a focus on balance sheet protection and liquidity conservation. The Covid 1.0 lockdown was further accompanied by the moratorium and dispensations around NPA classification which further reduced visibility of borrower cashflows, leverage and credit worthiness.

- Growth picked up Q3FY21 onwards: Q3FY21 onwards as visibility around borrower cashflows started improving, the data from credit bureaus became clearer and the economy started opening up we saw the growth of KCP lenders reach pre-Covid levels. In Q4FY21, the KCP lenders further accelerated their growth rate and continued to grow at twice the rate of the banking industry with annualized growth rates exceeding pre-Covid levels. The growth in Q4FY21 was higher not only at an aggregate portfolio level but was broad based across the portfolio as the growth of all KCP lenders were equal to or higher than pre-Covid levels.

|

|

KCP lenders have demonstrated resilience during the crisis

- Tier-1 capital of KCP lenders increased to 21% from 18%: Contrary to expectations, the Tier-1 Capital of the KCP lenders has increased relative to pre-Covid levels. The KCP lenders were able to increase Tier-1 capital because of: (i) a resilient P&L thanks to strong pre-provisioning profitability (which was able to absorb Covid provisions); (ii) the ability of the KCP lenders to raise equity during the crisis; and (iii) lower consumption of capital due to lower growth in FY21. The KCP lenders will be able to use this additional firepower to cater to credit demand over the next few quarters.

- Manageable increase in net NPAs to 1.1%: Despite a nationwide lockdown for three months and an unprecedented health crisis in the country, the KCP lenders saw their gross NPAs increase by only 80bps to 2.6% and their net NPAs increase by only 10 bps to 1.1%. The 1.1% net NPAs are excluding overlay Covid provisions held by the KCP lenders. If these Covid provisions were to be included, the net NPAs of KCP lenders in Q4FY21 would be lower than pre-Covid levels. The KCP lenders were able to manage asset quality better than their peers because of: (i) conservative underwriting practices followed by KCP lenders even before Covid; and (ii) proactive measures taken to augment collection capacity. For eg. Bajaj Finance added 2,800 collections officers and 16,000 outsourced collection agents to increase its collection infrastructure by 25%-30% relative to pre-Covid levels.

- Conservative provisioning standards: We prefer to invest in lenders which do not kick the can down the road on NPA recognition and provisioning to show higher profitability in the short term. In general, lenders which are well provided for may have lower profitability temporarily but have stronger balance sheets and a higher future earnings potential on a structural basis. As discussed in the December 2020 Kings of Capital newsletter (click here to read) during the moratorium period even though NPAs were not required to be recognized, the KCP lenders continued to provide for expected NPAs. As a result, the provision coverage ratio of KCP lenders in Q4FY21 stands at 92% versus a 52% provision coverage ratio before Covid. We expect these excess provision buffers to reduce the requirement for Kings of Capital lenders to create incremental provisions for the second Covid wave. We do NOT believe that the same can be said for other lenders in India.

|

|

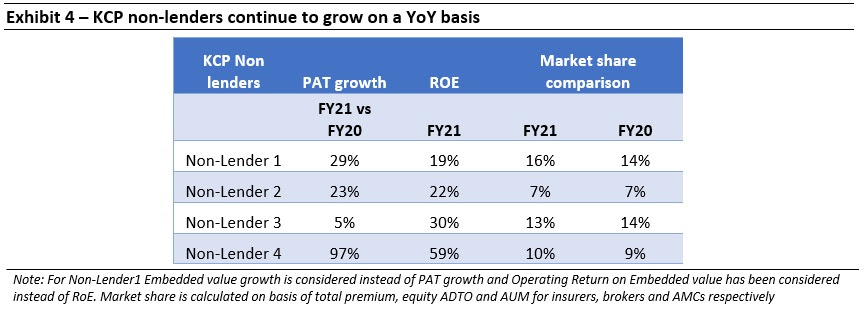

KCP non-lenders continued their growth trajectory even during Covid

Non-lenders in the KCP portfolio include insurance companies, asset managers and brokerages. We have given below is an update on each of these businesses:

- Life insurance: HDFC Life’s Embedded Value grew 29% YoY during FY21. This was on the back of continued market share gains during the year. During the year, HDFC Life improved its solvency ratio (201% in FY21 vs. 184% in FY20), persistency metrics (13th month persistency of 90% in FY21 vs. 88% in FY20), new business margins (26.1% in FY21 vs. 25.9% in FY20) and return on embedded value (18.5% in FY21 vs. 18.1% in FY20).

- General Insurance: While the market share for ICICI Lombard based on total premiums was flat year on year, ICICI Lombard’s PAT grew 23% YoY during FY21. This is in-line with ICICI Lombard’s strategy of focusing on profitable growth as highlighted in our March 2021 KCP newsletter (click here to read). ICICI Lombard was able to grow profitability on the back of lower motor insurance claims during the year which were able to offset the higher health insurance claims due to Covid.

- Asset Management: The asset management business grew its AUM by 12% YoY and continues to be one of the largest asset managers in the country. The company has seen a leadership transition and is taking steps towards reversing the market share loss during the year. Some of the steps taken by the company are: (i) recruiting new fund managers to increase style diversity, (ii) launching new products including NFOs; and (iii) investing in digital initiatives to accelerate client acquisition and improve customer experience.

- Broking and wealth management: The retail brokerage business continues to do well with strong industry tailwinds. During FY21, its PAT grew by 97% YoY on the back of market share gains and increasing retail participation in equity markets. The company has added various new revenue drivers over the past year along and acceleration of client acquisition to ~1 lakh clients per month.

|

|

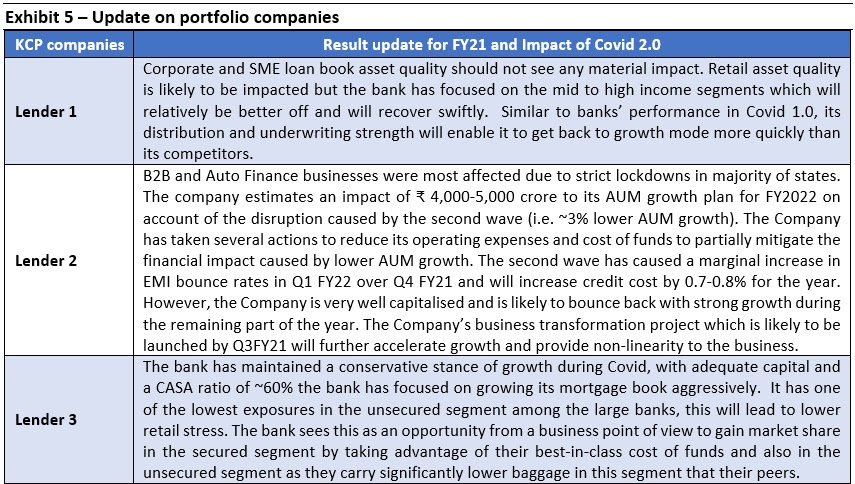

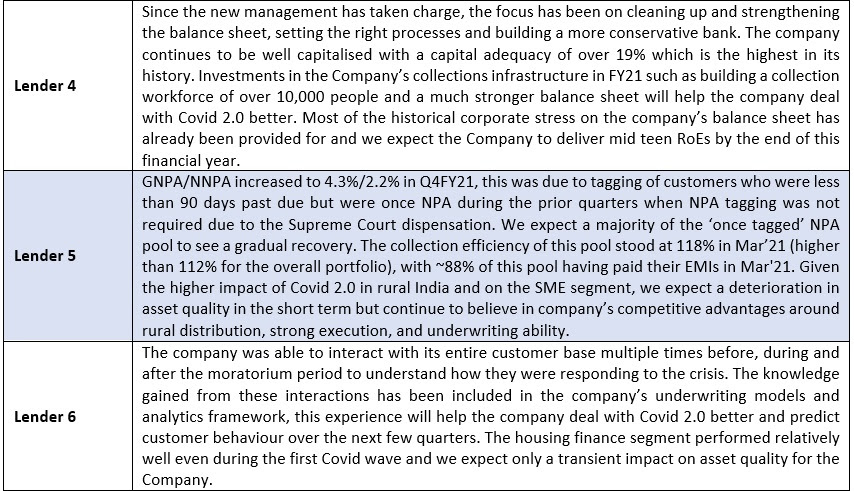

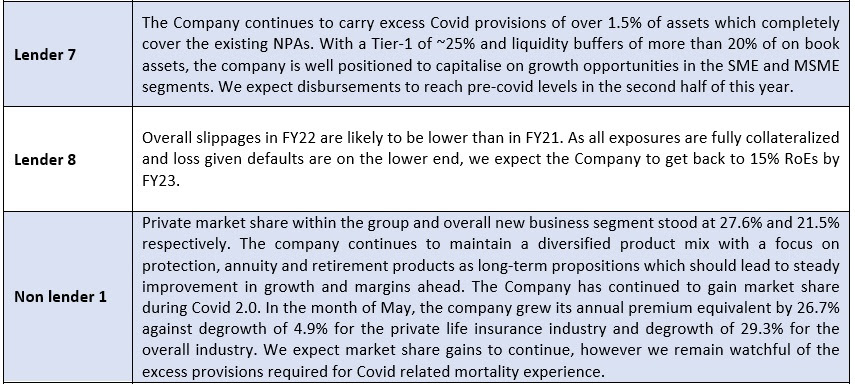

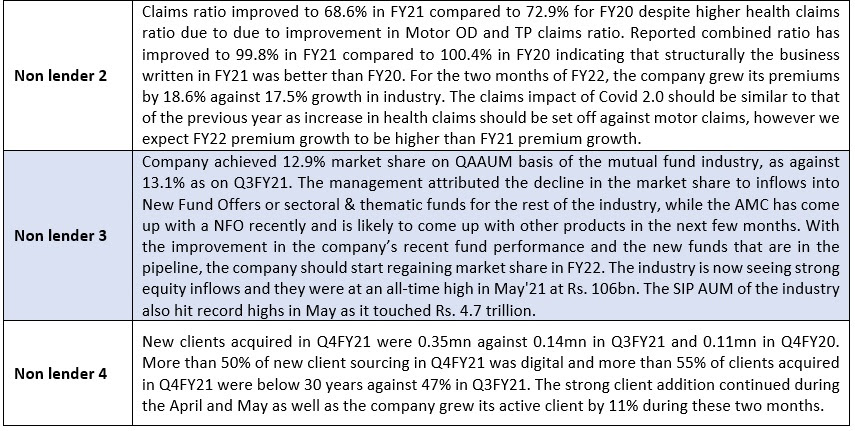

Impact of the second Covid wave on the Kings of Capital portfolio

We believe the disruption and financial impact of the second Covid wave on the KCP lenders will be much lower than the first Covid wave. Not only were the lockdowns during the second wave less severe, but having gone through such a disruption, the lenders were also better prepared to deal with Covid 2.0. We expect a marginal increase in NPAs especially for those lenders which have a larger restructured loan book and are focusing on the more vulnerable customer segments (SME and unsecured segments). Given that the KCP lenders have adequate provision buffers and excess Tier-1 capital, we believe that the incremental stress will be manageable and as highlighted in our May, 2021 newsletter (click here to read), long term investors can continue benefitting from the structural tailwinds available to private sector lenders. Below is our assessment of Covid impact on each of the portfolio companies.

|

|

Regards

Team Marcellus

Disclaimer: Copyright © 2026 Marcellus Investment Managers Pvt Ltd, All rights reserved

Note: the above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer or an employee.

This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.

Regards, Team Marcellus

If you want to read our other published material, please visit https://marcellus.in/pms-investment-blog/

Copyright © 2026 Marcellus Investment Managers Pvt Ltd, All rights reserved