All businesses face the event of succession of key management personnel, whether it be promoters or professionals. However, succession planning is a process that is not adequately engrained in the DNA of most organizations due to the variety of challenges involved in this process. As a result, many great businesses with strong competitive advantages fail to sustain in the long run. Our proprietary succession planning framework assesses all our portfolio companies around parameters such as the decentralization of power, the relevance of independent directors on the Board, and the empowerment of high quality CXOs in the organization. This assessment is one of the key inputs which drive our conviction around the longevity of a franchise, and hence on the prospects of consistent compounding of its share price.

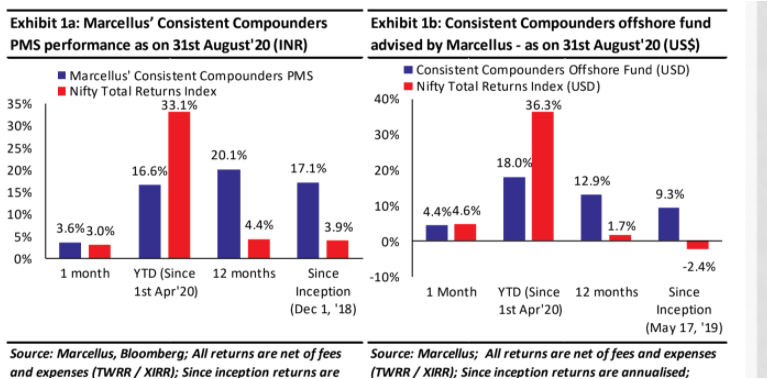

Performance update – as on 31st August 2020

We have a coverage universe of around 25 stocks, which have historically delivered a high degree of consistency in ROCE and revenue growth rates. Our research team of ten analysts focuses on understanding the reasons why companies in our coverage universe have consistently delivered superior financial performance. Based on this understanding, we construct a concentrated portfolio of companies with an intended average holding period of stocks of 8-10 years or longer. The latest performance of our PMS and offshore fund (USD denominated) portfolios is shown in the charts below.

Succession planning is a critical factor when it comes to the longevity of a franchise

We intend to have stocks in our Consistent Compounders Portfolio which do not just have strong competitive advantages. Instead, they should have strong and sustainable competitive advantages. Sustainability of strong competitive advantages gives longevity to a great franchise, which helps substantially reduce several risks, such as the risk of ‘timing’ of entry and exit from a stock, risk of volatility in the external environment (macro, competition, disruptions etc) impacting the franchise, and the risk of over-valuation in stock picking (because longevity is the most under-appreciated factor in a typical firm’s valuation). One of the drivers of longevity of a business is succession planning of key executives – CXOs and promoters – who drive ground level execution and strategic decision-making around capital allocation.

As businesses, customers, competitors, and the macro environment evolves over time, our bottom-up research works on our portfolio companies through two proprietary frameworks – a) the lethargy test framework which assesses the strength of the competitive advantages of our portfolio companies; and b) the succession planning framework which substantially contributes to our view on the longevity of the competitive advantages of our portfolio companies. These two frameworks also drive the allocation of a stock in our portfolio relative to other portfolio constituents. We discussed our lethargy framework in our last month’s newsletter (click here). In this newsletter we discuss our succession planning framework.

Passing the torch of leadership comes with its own set of challenges

Succession planning is not an event. It is a process that must be embedded in the DNA of an organization. However, implementation of a succession plan is challenging at multiple levels for most organisations.

When a business is small, it might be run by a leader (CEO or MD or promoter) with the persona of being omnipotent – someone who can do anything and can solve all problems. As such organisations grow bigger in size, the ‘omnipotent’ leader, might feel insecure about letting go off control, which becomes particularly difficult when the firm has built strong competitive advantages under the same leader. Moreover, if the leader builds a layer of CXOs and trains them as potential successors, then there is a risk that the trained CXOs who don’t get the top job will leave the firm to become CEOs of other organisations. Such exits can then leave a massive void in the organization.

The optimal timing of identifying a successor is also important. If the successor is identified too soon, then there is the risk of increase in attrition amongst other capable CXOs as they see themselves having hit a ceiling in their career progression. If the successor is identified too late, then she might be underprepared for the role and other senior managers in the team might not have built enough trust in her leadership capabilities.

Many businesses in India are run by promoter families. Such promoters might have a tendency to think about their sons and daughters as the default options for succession. Unlike some professionals who might have worked in the organization for 20-30 years, successors from the next generation of the promoter family might not have spent enough time at the ground level to learn about the strengths and weaknesses of the business, build trust and relationship with various stakeholders etc. Furthermore, there might also be more than one candidate from the next generation of the promoter family and this could create friction amongst family members.

Such challenges, if not addressed properly through an institutionalized and meritocratic succession planning process, can lead to strategic mistakes, deterioration in employee culture or lethargy and complacency in ground level execution and capital allocation.

Marcellus’ succession planning framework

“One of the things we often miss in succession planning is that it should be gradual and thoughtful, with lot of sharing of information and knowledge and perspective, so that it’s almost a non-event when it happens” – Anne M. Mulcahy, Former CEO and Chairwoman, Xerox

As part of our research process, we track and evaluate all portfolio companies on our proprietary succession planning framework, which has the following four parts to it:

Evidence of decentralization of power & authority:

There are three broad aspects of decentralization that we look for in a firm. Firstly, execution of day to day business should be done by a team of empowered professionals in an institutionalized manner (i.e. clearly laid out measurable timebound targets). Secondly, capital allocation decisions should not be controlled centrally by one man/woman. Instead, such decisions should be taken by a team of senior executives with active involvement of an empowered and independent board of directors. Thirdly, there should be high quality systems and processes in place (through tech investments or otherwise) to execute the business at a ground level (rather than extensive of manual interventions), as well as to help guide the business towards future growth opportunities.

Quality and tenure of CXOs in the organization:

For succession planning to be in the DNA of an organization, the heads of various functions (finance, sales, marketing, manufacturing, IT, HR, etc) have to be groomed & trained over a period of time. We prefer to see CXOs who have worked in the firm for more than 10-20 years, maybe across functions, and have risen through the ranks meritocratically; external recruitment of CXOs, by definition, is indicative of weak succession planning. While a firm may need to recruit externally to fill some roles, we prefer internal employees since they are already familiar with the company’s processes, strengths, goals and hence the DNA. Ability to train, retain and grow high quality talent is one of the key drivers for strengthening and evolving the moats of a business.

Board of directors:

Whilst it is easy to put together a board of directors for a company, it is difficult to build a high quality of board, with members who have relevant and diverse set of expertise, are truly independent and fully empowered i.e. able to take a viewpoint contrary to that espoused by the management. Such a high-quality board helps the firm in two broad areas – a) capital allocation related strategic decision making; and b) implementation and nurturing of succession planning at the firm by getting actively involved in the recruitment of CXOs in the firm.

Historical experience:

Whilst it is good to understand the construct of succession planning that exists at a particular organization, it is even better to see historical evidence of execution of succession at the CXO level without adverse impact on the organisation.

Asian Paints is one the best examples from our CCP portfolio of a company that covers all aspects of our succession planning framework reasonably well. For more than a decade now, execution of operations has been totally controlled by empowered professionals from the CEO level down to the middle management level in the firm’s hierarchy. Over the last 50 years, the firm has been hiring talent from the best universities as management trainees and has had an outstanding track record of training and retaining this talent pool for more than 20-25 years. As a result, most of its CXOs and KMPs have spent more than 20 years at Asian Paints across several functions. Tech investments and data analytics drive a large part of Asian Paints’ competitive advantage. All seven independent directors on the board of Asian Paints have highly reputed and relevant professional backgrounds (click here). And last but not the least, the firm’s historical track has been healthy and consistent despite: a) three instances of professional CEO changes over the last 15 years, b) three generations of Asian Paints’ promoter families have come and gone the last 70 years, c) one of the founding promoter families exited in 1997, and d) several CXOs have changed hands regularly.

HDFC Bank is one of our portfolio companies whose current competitive advantages are perhaps as robust as that of Asian Paints. However, HDFC bank gets a lower score than Asian Paints on our succession planning framework. When it comes to execution of its day to day business, HDFC Bank has one of the best systems and processes across India’s banking industry and has an army of professionals who have spent more than 15 years with the bank across various functions. Our interactions with various people who have worked at HDFC Bank for a long time period, suggest that the bank’s focus on systems and processes has made manual intervention redundant across most of its day to day functions. We believe the strengths of well-established SOPs, robust credit underwriting and a resilient balance sheet will hold HDFC Bank in good stead for the next few years as the company goes through a leadership transition. However, over the past three years, CXO level attrition has increased substantially and some of the CXO level roles are currently managed by individuals who have been external hires and have hence worked for less than 5 years in the bank. Whilst the quality of its board of directors is good (click here) with relevant experts from diverse backgrounds, the firm has not yet seen a leadership transition in its entire history of over 25 years.

Hence, although we expect HDFC Bank’s earnings growth to be higher than that of Asian Paints over the next 3-5 years, HDFC Bank’s portfolio allocation is smaller than that of Asian Paints in our Consistent Compounders Portfolio, primarily because of its weaker score on our succession planning framework.

Investment implications

“A leader’s lasting value is measured by succession” – John C. Maxwell in his book ‘The 21 Irrefutable Laws of Leadership: Follow Them and People Will Follow You’, 2007

As highlighted in our January 2020 newsletter (click here), the valuation of a firm needs to capture two broad parameters – a) strength of the firm’s competitive advantages which can drive healthy and consistent fundamentals over the next 3-5 years; and b) sustainability of the firm’s competitive advantages, which drives the longevity of healthy and consistent compounding of fundamentals beyond the next 3-5 years. Share prices of some great firms might reasonably factor in the first of these two parameters. However, it is the second parameter (longevity) which is often inadequately factored into valuations of great companies.

If nothing were to change inside or outside a firm, it would have been possible to deliver longevity of a franchise through its current competitive advantages. However, not only do we see changes in the external environment of a firm over time (like product-related disruptions, change in consumer preferences, competition, regulatory change, etc), every firm goes through changes in the internal environment as well, key amongst them being the shape and size of the firm’s management team. Hence, firms with succession planning deeply embedded in its systems and processes end up delivering substantial longevity to their business and hence shareholder returns over time.

Hence, these two factors – strength and sustainability of a firm’s competitive advantages – are the biggest drivers of stock allocations in our Consistent Compounders Portfolio. As firms in our portfolio either go through a succession event we not just focus on understanding the evolution of the firm’s competitive advantages, we also try to learn more about the effectiveness of succession planning at the firm, which then feeds into our longevity expectation for the business.

Regards

Team Marcellus

If you want to read our other published material, please visit https://marcellus.in/

Note: the above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this email in any shape or form. Marcellus Investment Managers is regulated by the Securities and Exchange Board of India as a provider of Portfolio Management Services and as an Investment Advisor. The performance related information provided herein is not verified by SEBI.