The holy grail of investing in stock markets is to buy companies which can sustain a healthy ROCE with growing capital employed, thereby delivering consistent earnings growth over long time periods. In this newsletter, we divide the Nifty50’s constituents into three buckets – A (no moats), B (shallow moats), and C (deep moats) based on their historical ROCE and revenue growth. Unlike the standard definition of riskreward framework (i.e. increasing returns come with rising risk), the Indian stock market offers an arbitrage. Bucket C companies not only delivered healthier returns vs the broader market, the risk involved was also much lower, similar to that of a Government bond!

“And the things best to know are first principles and causes. For through them and from them all other things may be known but not they through the things covered by them… But these things, the most universal, are perhaps the most difficult things for men to grasp, for they are farthest removed from the senses.” – Aristotle (384-322 B.C.E.), Metaphysics

First principles thinking in stock market investing would suggest the following:

- All investors (not speculators) in the stock market intend to make a healthy return on their investment

over long periods of time - The simplest way to understand what drives share price performance of a company is the following

mathematical equation: Price = (Price / Earnings) x Earnings - Out of the two components of share price movement defined in the equation above, over the long

term, while the earnings of a stock can compound, the P/E multiple does NOT compound. For instance,

you can find companies whose earnings grew from 10 units to 100, and then to 1000 and 10,000 over

a long time period. However, there are no stocks which saw their P/E multiple growing from 10x to

100x, and then to 1000x and 10,000x

A combination of the three bullets highlighted above would suggest that long term share price performance

of any stock is determined by its ability to compound earnings over the long term.

That brings us to the next question – how can one measure the ability of a company to compound its earnings over the long term? Using first principles, the most common way for a firm to compound its earnings over the long term is to first deliver healthy earnings on its capital employed (i.e. a healthy ROCE) and then redeploy part of these earnings back onto the balance sheet and hence grow the capital employed. Ongoing sustenance of a healthy ROCE on a growing base of capital employed then delivers sustainable growth in earnings over time.

Searching for evidence of such an engine of consistent earnings growth in the long-term historical financials of a firm, would therefore mean, looking at a combination of consistent and healthy revenue growth and ROCE of a firm.

In the Indian context, where the country’s nominal GDP growth (real GDP growth + inflation) has been higher than 10% consistently, and where cost of capital in the country has been around 15% consistently, the bare minimum that an investor would want from the management of his investee company is to beat these two benchmarks as the firm’s revenue growth and ROCE respectively. Sounds easy, but let’s see how many firms manage to deliver this.

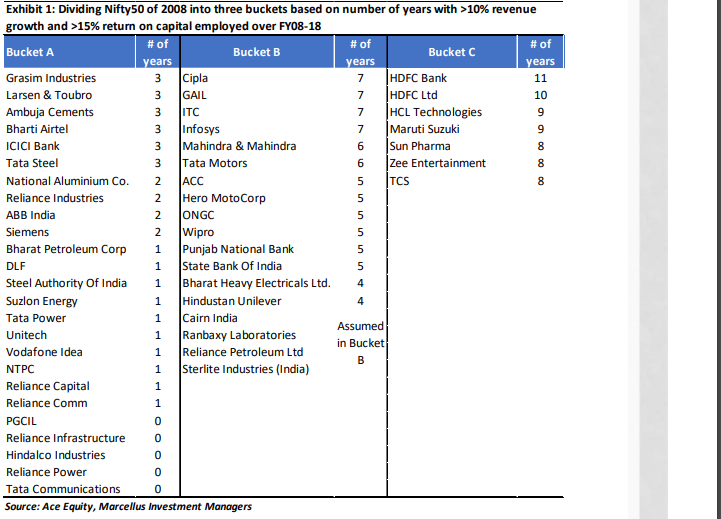

Analysing the constituents of Nifty50, as they existed in 2008

Sensex and Nifty50 are the most commonly used benchmarks in Indian stock market. So, let’s divide the Nifty50 constituents of a decade ago – 2008 – into three buckets based on their revenue growth and ROCE delivered over FY08-18

Companies who have delivered >10% revenue growth and >15% ROCE in less than

or equal to 3 financial years over FY08-18. These are companies which do not possess any moats, and hence

are not able to sustain healthy ROCEs.

Bucket-B (B for Buffett):

Companies who have delivered >10% revenue growth and >15% ROCE in more than

3 financial years, but less than or equal to 7 financial years over FY08-18. These are companies with shallow

moats that get challenged every now and then by aggressive competition.

Bucket-C (C for Compounders):

Companies who have delivered >10% revenue growth and >15% ROCE in more

than 7 financial years over FY08-18. These are companies which perhaps possess deep moats that are difficult

to break into.

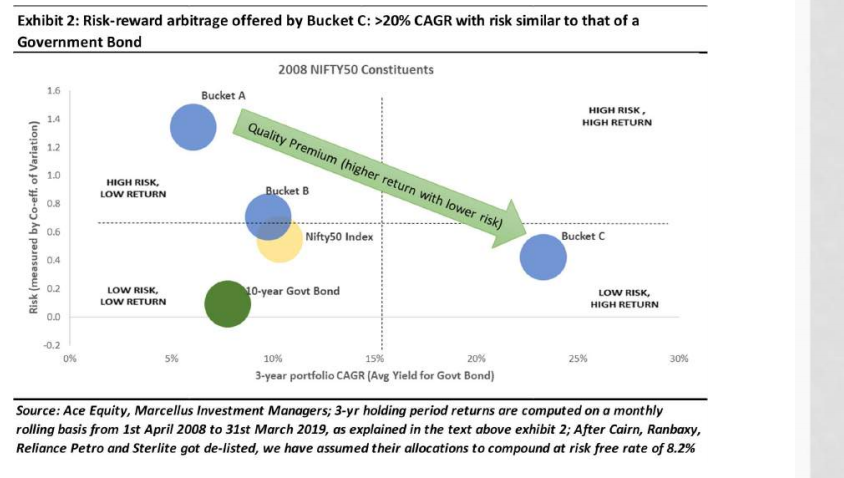

Next, let’s create equal weighted portfolios of stocks in each of the three buckets in 2008 and analyse the riskreward of a three-year holding period return of these portfolios. We use monthly rolling 3 year return data points i.e. (1st Apr 2008 to 31st Mar 2011), (1st May 2008 to 30th Apr 2011), (1st June 2008 to 31st May 2011) and so on. The exhibit below shows the outcome of this exercise. Alongside the three buckets, the exhibit below also includes data points for Nifty50 (i.e. the index as it has evolved over the past decade).

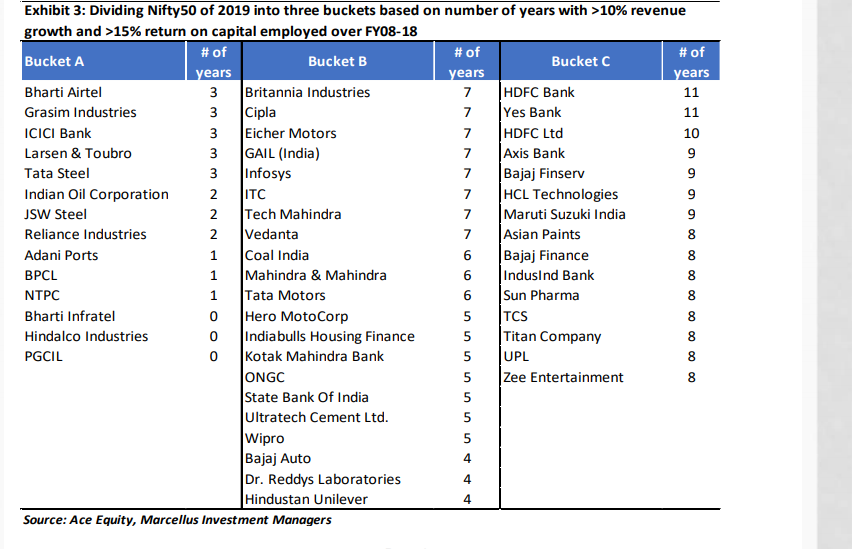

Analysing the constituents of Nifty50, as they exist in 2019

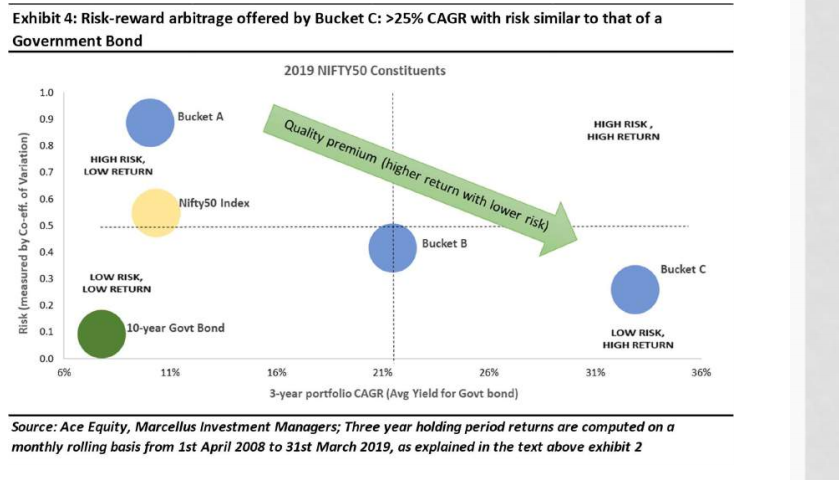

Even if one were to repeat the exercise highlighted above for today’s Nifty50 constituents, using their revenue growth and ROCE reported over FY08-18, and then look at the performance of today’s Nifty50 constituents over the past decade, the outcome is very similar to what we saw with 2008 Nifty50 constituents.

Investment implications

Following are the key conclusions emerging from the analysis above:

- Unlike the standard definition of risk-reward framework (i.e. increasing returns come with rising risk),

Indian stock market offers an arbitrage. Over the past decade, if you chose companies which delivered

>10% revenue growth and >15% ROCE in a reasonably consistent manner, not only did you get a much

healthier return vs the broader market, this return came with a much lower risk as well – similar to

that of a Government Bond! - Over the past decade, a portfolio of companies from Bucket C made redundant, the top-right quadrant

of Exhibit 2 and Exhibit 4. In other words, there would have been several investment philosophies over

the past decade which aimed at delivering >20% CAGR over a 3-year investment horizon by taking a

high risk in the form of spotting a ‘unicorn’ / multi-bagger amongst small caps, or by timing events

(general elections, macro-economic parameter), timing cycles, valuations etc. Any such investment

philosophy which involved higher risk in exchange for and 20-25% CAGR in returns, was worse off,

compared to companies in Bucket C which delivered lower risk for the similar or higher returns. - Regardless of when you did this exercise over the past 25 years, the Indian stock market has always

offered this arbitrage of generating low-risk and high-returns.

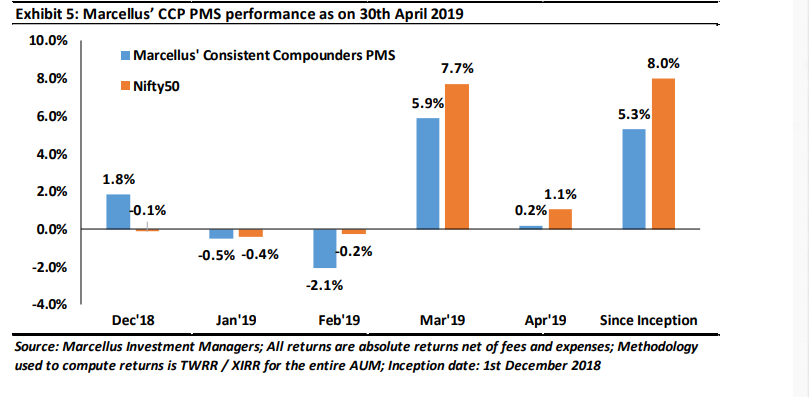

Marcellus’ Consistent Compounders PMS – Performance update

Marcellus’ Consistent Compounders PMS has a coverage universe of just over a couple of dozen stocks, which have historically delivered a high degree of consistency in ROCE and revenue growth rates. Our research process then involves, understanding the reasons why companies in our coverage universe delivered a great historical track record. Based on this understanding, we construct a portfolio of 10-15 companies with an intended average holding period of stocks of 8-10 years or longer. The latest performance of our PMS is shown in the chart below.

Regards

Team Marcellus

If you want to read our other published material, please click here

Note: the above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this email in any shape or form. Marcellus Investment Managers is regulated by the Securities and Exchange Board of India as a provider of Portfolio Management Services and as an Investment Advisor.

This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient if not the addressee should not use this message if erroneously received, and access and use of this e-mail in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. Any opinions or advice contained in this email are subject to the terms and conditions expressed in a duly executed contract or written agreement between Marcellus Investment Managers Private Limited and the intended recipient. No liability whatsoever is assumed by the sender as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus Investment Managers Private Limited may be unable to exercise control or ensure or guarantee the integrity of the text of the email message and the text is not warranted as to its completeness and accuracy.