OVERVIEW

POPULAR ARTICLES

5 sets of factors make sensible saving & investing in your 50s even more important for Indians than for people in the developed world: 1) rapidly rising life expectancy, 2) surging healthcare & hospitalisation costs, 3) steadily rising cost of paying for children’s overseas education, 4) clear signs that AI will lead to job cuts for mid-senior level employees, and 5) most Indians have most of their assets in physical assets like real estate & gold which may not generate comparable long-term returns relative to financial assets. In this note we address each of these issues. Our free goal planning & asset allocation service (plan.marcellus.in) helps you address these challenges calmly and methodically.

Target corpus required at age 60, India-adjusted [note: SWR stands for Safe Withdrawal Rate i.e. the percentage of retirement savings you can withdraw annually—adjusted for inflation—without exhausting your portfolio over a set period]

|

Annual expenses in retirement (today’s ₹) |

Required corpus at India SWR of 3.5% |

|

₹12 lakh (middle class) |

₹3.5 crore |

|

₹18 lakh (affluent) |

₹5.3 crore |

|

₹24 lakh (premium) |

₹7 crore |

The world over, the retirement countdown clock ticks down in your 50s

Across the world, it is well understood that your 50s are the most important decade of your financial life. You’re earning peak income, but the runway to retirement has shrunk to a single decade. Compounding can no longer rescue mistakes.

Because compounding has done most of what it will do, mistakes can no longer be corrected by time, and the gap between what you have and what you’ll need becomes mathematically visible.

The fact that the window of time is narrowing is the single hardest thing to internalise for those in their 50s. A 30-year-old saving ₹10,000 a month at 12% p.a. compounds to about ₹3.5 crore by 60. A 50-year-old starting from zero with ₹10,000/month at 12% p.a. compounds to about ₹23 lakh — less than 7% of the same person who started 20 years earlier. The asymmetry is brutal.

To build a $1 million nest egg by age 65, assuming 8% returns:

· Starting at age 25: $300 per month is enough

· Starting at age 35: $700 per month is enough

· Starting at age 45: $1,700 per month is enoug

· Starting at age 50: $3,000 per month is enough i.e. 10x what the 25-year-old saved.

In rupee terms, an Indian starting at 50 with no retirement savings and targeting a realistic ₹5 crore corpus by 60, assuming 12% pre-tax equity returns, needs to save roughly ₹2.2 lakh every single month for 10 years. That’s a big ask for most middle-class Indians.

Leaving aside the narrowing of the time window, the other challenge that investors the world over face in their 50s is that the paucity of time makes it harder to recover from a market crash. A market crash in your 30s is recoverable; the same crash within 5 years of retirement can destroy a retirement.

Two brothers each start retirement with $500,000 and withdraw $30,000/year (the classic 6% rate). Same average return, same withdrawal — different sequence. Brother Steve gets bad returns at the end; ten years in he still has $874,000. Brother Bill gets bad returns at the start; ten years in he has $96,318. Same math, dramatically different outcome.

With equity-heavy portfolios in your 50s are exposed to this risk for 10-15 years on each side of retirement. If the Nifty falls 40% the year you retire and you’re forced to sell equity to fund expenses, you crystallise losses you can never recover. This is why every credible glide-path framework (Vanguard, Morningstar India, Outlook Money) calls for de-risking gradually starting in the early 50s.

All of these however are standard challenges that retirees-to-be face the world over.

India creates FIVE extra challenges for 50–60-year-olds

Indians in their late 30s to early 50s are increasingly the ‘sandwich generation’ — financially supporting ageing parents (no Indian social security floor) and dependent children (overseas-education costs at ₹50-80 lakh) at the same time.

5 sets of factors make sensible saving & investing in your 50s even more important for Indians than for people in the developed world: 1) rapidly rising life expectancy, 2) surging healthcare & hospitalization costs, 3) steadily rising cost of paying for children’s overseas education, 4) clear signs that AI will lead to job cuts for mid-senior level employees in IT Services and Banking & Financial Services, and 5) most Indians have most of their assets in physical assets like real estate & gold which may not generate comparable long-term returns relative to financial assets. In this sub-section we address each of these issues.

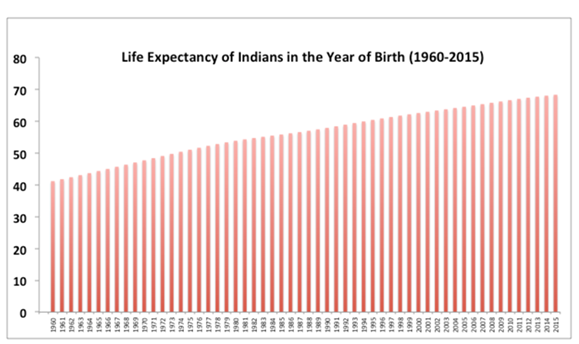

Firstly, life expectancy is rising steadily in India. Life expectancy at 60 today implies 20-25 more years to fund. India’s life expectancy at birth is now 72.48 years (2025), up from 41 in 1950.

Crucially, life expectancy conditional on reaching 60 is far higher than life expectancy at birth. A 60-year-old urban Indian today can realistically expect to live to 80-85, and women longer.

Source: World Bank

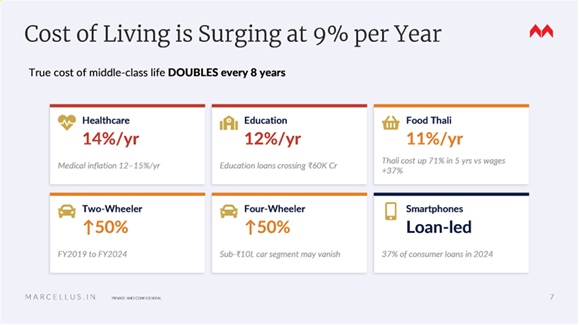

Secondly, medical inflation in India is running at 13-14% per year — roughly three times general CPI. Average hospitalisation claim value rose from ₹62,548 to ₹70,558 in a single year. India currently holds the highest medical inflation rate in Asia.

More generally, cost of living is now ramping up rapidly for middle class India (as explained in our chapter on this subject in our bestseller, “Breakpoint: The Crisis of the Middle Class and the Future of Work” (see the exhibit below).

The practical impact of this on retirement planning is very significant. The “safe withdrawal rate” refers to the amount a retiree can spend annually without adversely depleting her retirement corpus (in a manner which jeopardizes her standard of living in the years to come). The Indian-adjusted safe withdrawal rate is 3.5% (vs the global 4% rule), meaning a 50-year-old today needs 28-30x annual expenses to retire safely — not the textbook 25x — because India’s higher inflation and zero social security floor demand a bigger cushion.

Thirdly, the HSBC Quality of Life Report 2024 (surveying 11,230 affluent individuals across 11 markets) found that an Indian parent’s overseas-education spend depletes 48% of their retirement savings for a 3-year degree, and up to 64% for a 4-year degree — the highest of any market HSBC surveyed . The average outlay per child studying abroad is ₹55 lakh per year. For more on this subject, please read our May 8 Parents Are Dipping Deep into Their Retirement Savings to Pay for their Kids’ Education blog on this.

Fourthly, Indian household assets are 66% locked in real estate and gold, only 5% in equity and 6% in insurance + pension combined (Jefferies India household balance sheet study). With less than 15% of their investments in financial market linked investments, Indians in their 50s are not able to capture fully the ability of good financial assets to deliver inflation busting returns in the long run.

And finally, AI is increasingly impacting employment trends for mid- to senior-level roles in India Inc. TCS announced 12,200 job cuts in 2025 — the biggest in its 50-year history — overwhelmingly hitting employees with 10+ years of experience i.e. those in their 40s and 50s. Analysts estimate 400,000-500,000 Indian IT jobs at risk over the next few years.

CEO K. Krithivasan called it ‘the toughest decision of my career’. Phil Fersht of HFS Research told Mint: ‘The impact of AI is eating into the people-heavy services model and forcing service providers to rebalance their workforces.’ Analysts at Business Standard / The Perfect Stories warned that 400,000-500,000 Indian IT jobs may be at risk over the coming years due to automation, AI, and pricing pressure (clients demanding 20-30% price cuts).

Wipro, HCL Tech and Infosys have either started senior-level releases or drastically slowed hiring. The implication for someone in their 50s: a job loss at 53 may not be followed by a comparable job at 54. ‘Quiet firing’ through bench rules — TCS now demands 225 billable days per year, max 35 days unallocated — disproportionately affects 45-50+ employees whose skills haven’t been refreshed.

Note- Incidental references (e.g., HCL) is used solely for illustration and reference only within the context discussed.

Given the gravity of the 5 factors highlighted above, it should not come as a surprise therefore that 90% of urban Indians over 50 regrets not starting retirement planning earlier.

In spite of all of these 5 reasons for focusing actively for sensible investing, for reasons we don’t fully understand, only 37% of Indian households have a retirement plan in 2025 — down from 67% in 2023.

So, what should 50–60-year-old Indians do?

In any retirement plan, there are two important dimensions to keep in mind: a) what is the size of the total pot that you need to build, and b) how should that pot be allocated across various assets. Let’s start with understanding the size of the pot that you need to aim for.

The Trinity-Study-derived ’25x rule’ (save 25x annual expenses, then withdraw 4% a year) was calibrated on US market history with US inflation (~3%) and US Social Security as a backstop. Neither assumption holds in India. As mentioned above, the India-adjusted safe withdrawal rate is 3.5%, implying a 28-30x multiple. For early retirees (40-year horizon) the multiple is 31-33x.

Now, let’s move to asset allocation. Brinson, Hood & Beebower (Financial Analysts Journal, 1986) found that 90% of variability in portfolio returns is explained by asset allocation, not security selection. For someone in their 50s, the glide path matters more than fund picks.

India-appropriate glide paths(consensus across Outlook Money, Morningstar India, Finnovate, Jiraaf)

|

Age |

Equity % |

Debt % |

Gold % |

Cash / liquid % |

|

30-40 (peak accumulation) |

70-80% |

15-25% |

5-10% |

2-5% |

|

40-50 (transition) |

60-70% |

25-35% |

5-10% |

2-5% |

|

50-55 (early de-risk) |

50-60% |

30-40% |

5-10% |

5% |

|

55-60 (heavy de-risk) |

40-50% |

40-50% |

5-10% |

5-10% |

|

60+ (retirement) |

25-40% |

50-65% |

5-10% |

5-10% |

Solution from Marcellus: Goal-based asset allocation

Marcellus offers a free goal planning and asset allocation framework wherein you can reach out to us and get a detailed 4-page financial report free of charge.

We work with a three-step approach to help our clients diversify globally:

1. Map your life goals to financial goals. How much do you need for near, medium, and long-term goals?

2. Allocate your investments across multiple uncorrelated asset classes. Avoid over concentration, illiquidity and disproportionate risk-reward. Get the allocation right based on your needs and your risk tolerance.

3. Remain disciplined. Continue to save and channel savings to investments. Review and rebalance regularly.

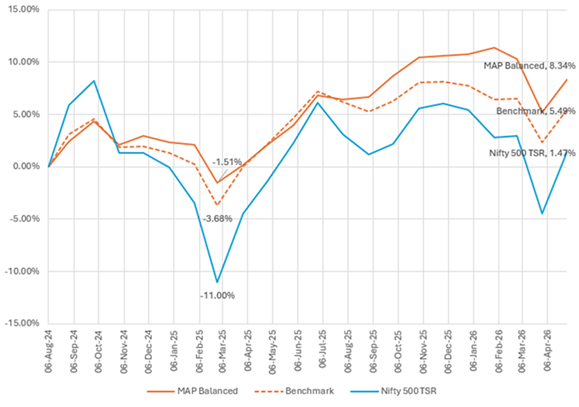

Marcellus’s ‘MAP-Balanced’ which has delivered 8.34% returns since inception in Aug-24 to April-26 net of all fees and costs against 1.47% of Nifty 500 TSR (see the chart below).

Source: Marcellus Investment Managers; Marcellus Performance Data shown is net of fixed fees and expenses charged till 31st March 2026 and is net of Performance fees charged for client accounts, whose account anniversary / performance calculation date falls upto the last date of this performance period; Returns more than 1-Year are annualized; other time period returns are absolute. For relative performance of particular Investment Approach to other Portfolio Managers within the selected strategy, please refer to https://www.apmiindia.org/apmi/welcomeiaperformance.htm?action=PMSmenu. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the SEC, SEBI or any other regulatory authority.

If you would like to avail of this free service (with no-strings attached) then either scan the QR code below OR visit plan.marcellus.in.

Please note that this is neither a financial plan, nor an investment advise.

Click Here for details about our regulatory registration and licensing information.

Disclaimer:

Note: the above material is neither investment research , nor investment advice. The performance information mentioned is provided for illustration of asset allocation outcomes and should not be construed as indicative of future performance. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. All recipients of this material must before dealing and or transacting in any of the products/services referred to in this material must make their own investigation, seek appropriate professional advice. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer or an employee. This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.