OVERVIEW

POPULAR ARTICLES

Summary: With 1.3 million Indians studying at Western universities, India leads the world in sending its kids to study abroad . While you would expect that of the world’s most populous nation, what is unexpected is the level of financial stress that Indian parents are bearing to finance their children’s dreams of a better life. Most Indian parents are either dipping deep into their retirement savings to pay for their children’s fees or borrowing from NBFCs at high interest rates. As the high default rates on these loans suggest, Indian parents need a less painful way to pay their children’s fees. At Marcellus, we have focused on finding that “less painful way”.

“For Indian parents, sending a child abroad for a three-year degree could deplete 48% of their retirement savings, while a four-year degree may consume up to 64%.” – HSBC Quality of Life Report 2024, surveying 11,230 affluent individuals across 11 markets.

This 48-64% depletion of retirement savings is the highest of any market HSBC surveyed. HSBC defines “affluent” as individuals with $100,000 to $2 million in investable assets – precisely the demographic that is likely to be reading this message from Marcellus.

Ninety per cent of Indian parents in the survey said they intend to fund their child’s overseas education — the highest among markets surveyed. Seventy-eight per cent of Indian respondents either have a child studying internationally or aspire to.

While the aspiration that Indian parents show in wanting to give their children the best education that money can buy is commendable, the all-inclusive cost of a 3–4-year undergraduate degree in developed economies like the US, UK, Canada or Australia is around $250K. As we write this blog in May 2026, that translates into around Rs 2.5 crore i.e. the price of a small flat in the suburbs of Hyderabad or Bangalore. However, this number – steep as it is – is growing at a rapid rate and thus causing significant challenges for Indian families.

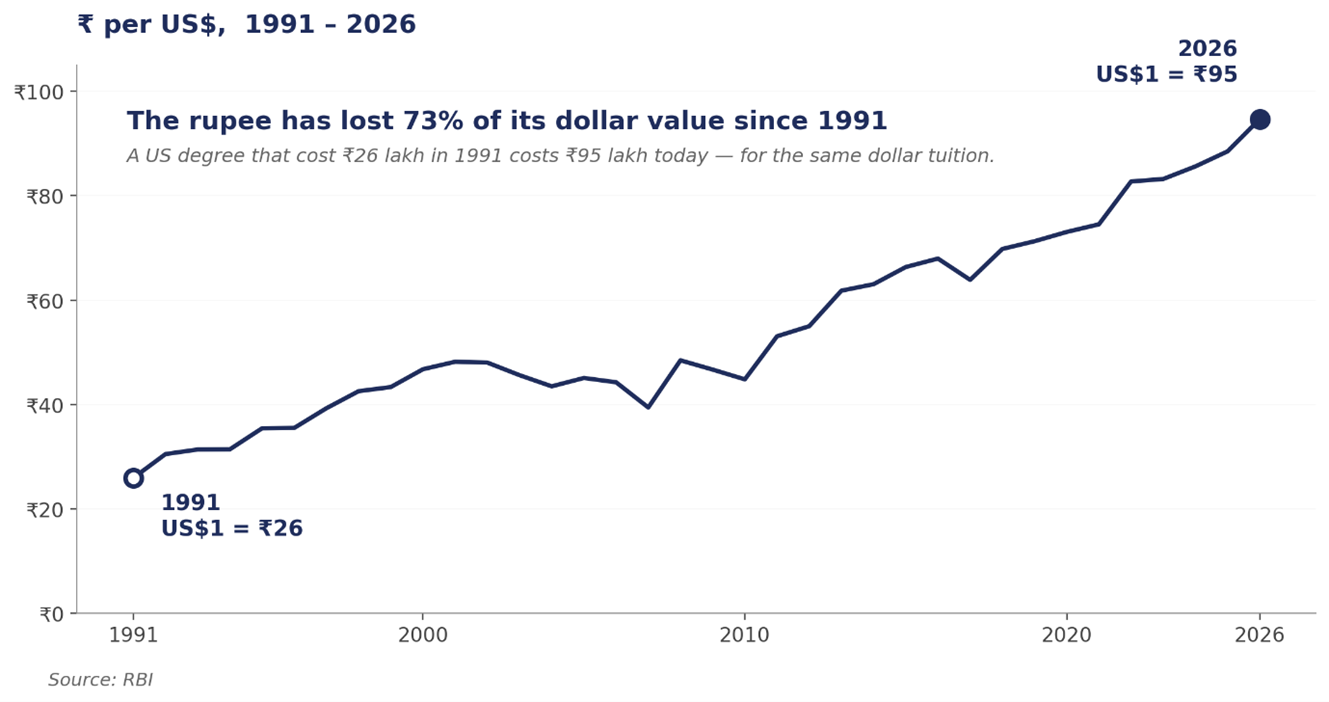

Problem 1: Relentless rupee depreciation jacks up cost of overseas education

Over the past year, the INR has lost 9% of its value to the $ thus pushing up the INR cost of an overseas education by a proportionate amount. However, this problem is neither new nor transient. Ever since the Indian economy liberalised in 1991, in every ten-year period since then the INR has lost around 40% of its value to the $. In other words, for an Indian parent who is trying to save money in INR for his daughter’s education abroad, the INR cost of this overseas education doubles every 12 years or so.

Problem 2: The ROI of overseas university education is falling

Inspite of the rising cost of overseas education, there is a simple reason why the vast majority of affluent Indians are keen to send their children to study abroad. As we have explained in our latest bestselling book, “Breakpoint: The Crisis of the Middle Class & The Future of Work”, it is increasingly difficult to get a job in India with an Indian degree. Azim Premji University’s latest study of Indian graduates shows that only 4% managed to get a white-collar job in the year of their graduation. In this context, an overseas degree helps an Indian student in two ways:

a) There is a reasonable probability that the Indian graduate can get a job in the developed market in which he/she graduates; and

b) Even if graduate were to return to India, while her Indian salary will be 1/5th or 1/10th of what she would earn in a developed market, her chances of getting a job in India are higher than that of a locally graduated desi student. Approximately 70% of Indian returnees from foreign degrees secure full-time roles within 6 months.

However, the logic outlined in the preceding two bullets is being challenged for a couple of reasons. Firstly, across the world, AI is gobbling up entry-level jobs. In Breakpoint, we have shown that the creation of white-collar jobs in India has come to a standstill in the past 3 years. In the West as well, even local graduates (who are citizens of that country) are finding it hard to get entry-level jobs. Secondly, because of the growing scarcity of jobs for graduates, developed economies are making it harder for Indian students to stay in their country once their studies are done

As is well known, Donald Trump is making it harder for Indian students to get jobs in America. In the UK, fewer than 10% of all international students convert from the 2-year Graduate Route to a Skilled Worker visa. The vast majority return home.

Canada’s PR pathway used to be its biggest selling point. As of 2025, the pathway has narrowed sharply due to study permit caps and Permanent Residency quota tightening. Express Entry CRS scores have risen, making it harder for students to qualify.

As more Indian students are compelled to return home to an overcrowded job market in India, the Return on Investment on an overseas degree is falling.

The combination of a falling rupee (and thus rising cost of overseas education) and the falling ROI on overseas education are pushing Indian families towards increasingly unattractive methods to pay for their offspring’s education.

Indian families are dipping deep into their retirement savings to pay for their children’s university education. As discussed at the beginning of this blog, even affluent parents are using up 50-60% of their retirement pot to pay for their children’s education. However, parents who do not have the luxury of sizeable retirement pots are having to turn to an even more demanding financing option, namely, borrowing from NBFCS at interest rates north of 12% p.a.

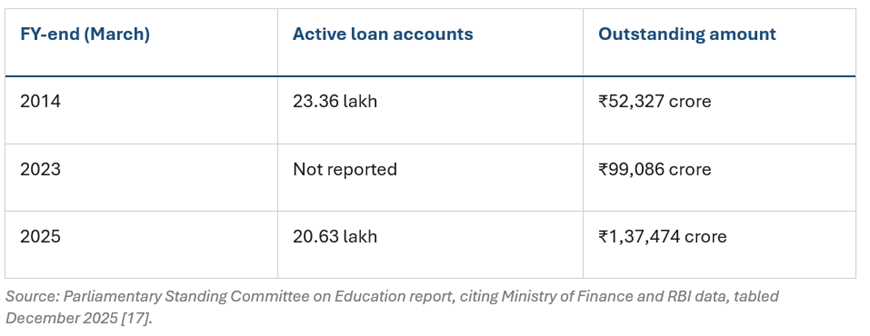

The education loan market in India has gone from a sleepy public-sector category to one of the fastest-growing retail credit segments in the past five years. The most authoritative recent figures come from a Parliamentary Standing Committee report tabled in December 2025.

Outstanding education loans — official figures

The outstanding figure grew 39% in just two years (₹99,086 crore in March 2023 to ₹1,37,474 crore in March 2025).

NBFC education loan AUM has been the fastest-growing retail asset class in Indian financial services. As per Crisil, NBFC education loan AUM grew 77% in FY24 and another 48% in FY25.

Given the high interest rates associated with these loans and given the challenged ROI of overseas university education, it should come as no surprise that as the RBI’s data education loans recorded the highest NPA rate among retail loans at 3.6%.

Solving the Education Financing problem

As highlighted above, most Indian parents are either dipping deep into their retirement savings to pay for their children’s fees or borrowing from NBFCs at high interest rates. As the high default rates on these loans suggest, Indian parents need a less painful way to pay for children’s fees. At Marcellus, we have focused on nailing down that “less painful way”.

The S&P500, the US stock market’s benchmark, has compounded returns over the past 30, 20 & 10 years at rates well in excess of 10% per annum. Assuming a 10% rate of return going forward, if an Indian family were to invest $50K in the US stock market when their child enters primary school, then 14 years later, when the same child finishes school, the parents will have a pot of nearly $200K ready to finance their children’s overseas university education for a 3-4 year undergraduate degree in USA, UK, Canada or Australia.

Marcellus has used its access to global assets to create three sets of solutions for Indian families who want to save sensibly for essential life goals such as retirement planning and overseas education for their children.

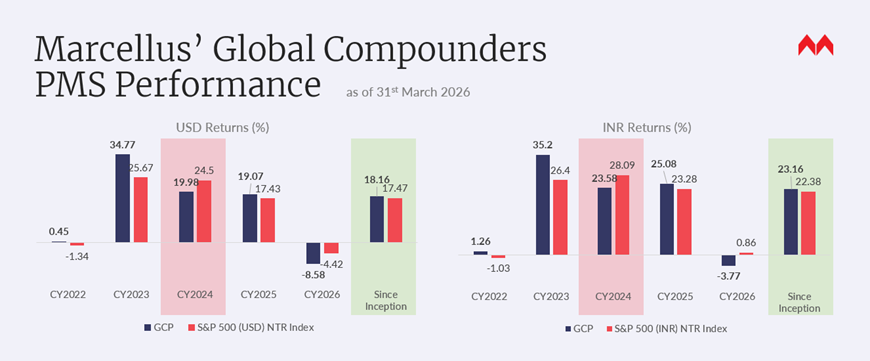

The first solution is our Global Compounders Portfolio (regulated by IFSCA) which was launched in October 2022 and invests in a mixture of North American, European and East Asian companies from our offices in GIFT City in Gujarat. This portfolio has compounded returns at 18% in US$ terms (net of all fees and costs).

Note: Marcellus performance data is shown gross of taxes and net of fees & expenses charged till end of last month on client account. Performance fees are charged annually in December. Returns more than 1-year are annualized. Marcellus’ GCP USD returns are converted into INR using USD: INR exchange rate from RBI – Link for the reference.

Note: * Since Inception performance calculated from 31st Oct 2022. The inception date is 31st Oct 2022, being the next business day after the account got funded on 28th October 2022. S&P 500 net total return is calculated by considering both capital appreciation and dividend payouts. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the IFSCA or US SEC. Performance is the combined performance of RI and NRI strategies.

Marcellus GCP PMS is offered by Marcellus Investment Managers GIFT Branch in a segregated managed accounts format.

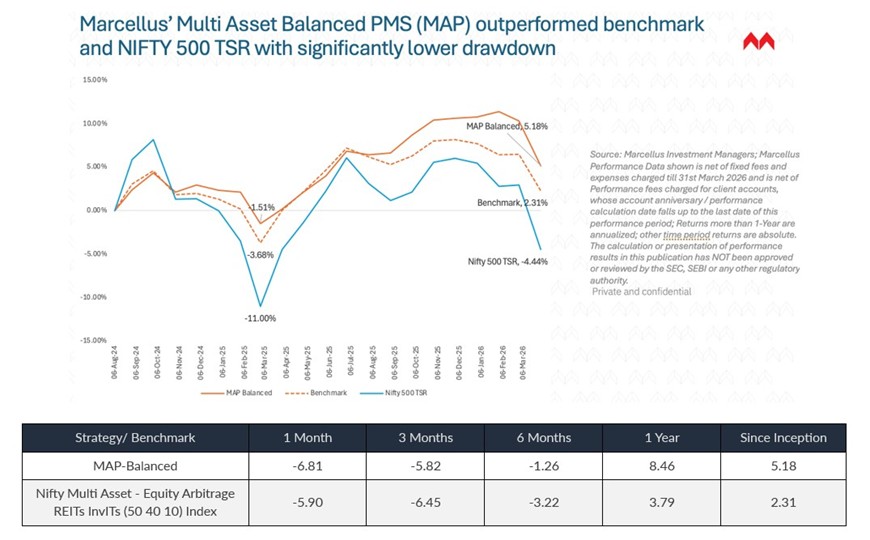

The second solution is a Multi-Asset Product (MAP) (Regulated by SEBI), which by diversifying across Indian Equities, Global Equities, Bonds and Precious Metals, produces smoother, more predictable returns. Our MAP PMS is available in three variants – Aggressive, Balanced and Conservative. For example, Marcellus’s ‘MAP-Balanced’ has delivered 5.18% returns since inception in Aug-24 to Mar-26 against loss of -4.44% of Nifty 500 – which you can see in chart below.

Source: Marcellus Investment Managers; Marcellus Performance Data shown is net of fixed fees and expenses charged till 31st March 2026 and is net of Performance fees charged for client accounts, whose account anniversary / performance calculation date falls upto the last date of this performance period; Returns more than 1-Year are annualized; other time period returns are absolute. For relative performance of particular investment approach to other Portfolio Managers within the selected strategy, please refer to https://www.apmiindia.org/apmi/welcomeiaperformance.htm?action=PMSmenu. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the SEC, SEBI or any other regulatory authority.

If you would like more information about our Multi Asset Portfolio strategy, please reach out to us by replying to this email.

The third solution is a free goal planning and asset allocation service wherein anyone could reach out to us and get a detailed 4-page financial report free of charge. If you would like to to avail of this free service (with no-strings attached) then either scan the QR code below OR visit plan.marcellus.in.

Please note that this is neither a financial plan, nor an investment advise.

Thanks

Saurabh Mukherjea

Disclaimer:

The above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the International Financial Services Centres Authority (IFSCA) as a Fund Management Entity No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. All recipients of this material must before dealing and or transacting in any of the products/services referred to in this material must make their own investigation, seek appropriate professional advice. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer or an employee. This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.