OVERVIEW

POPULAR ARTICLES

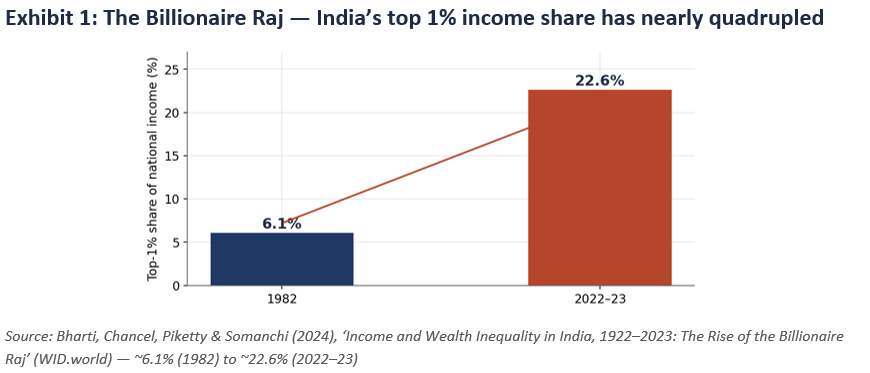

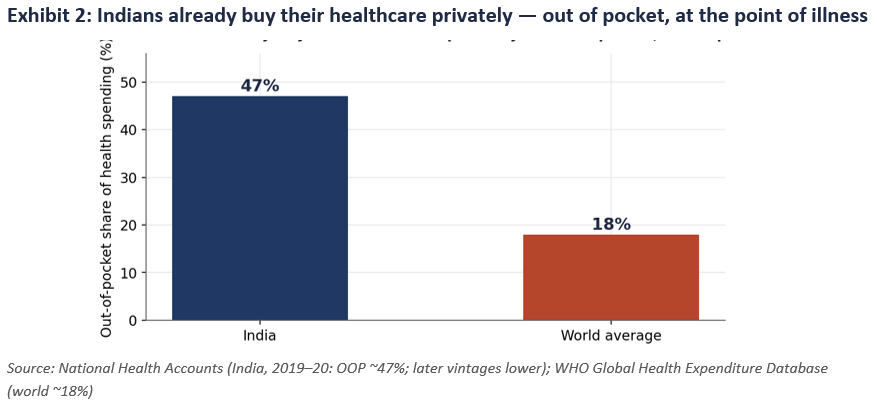

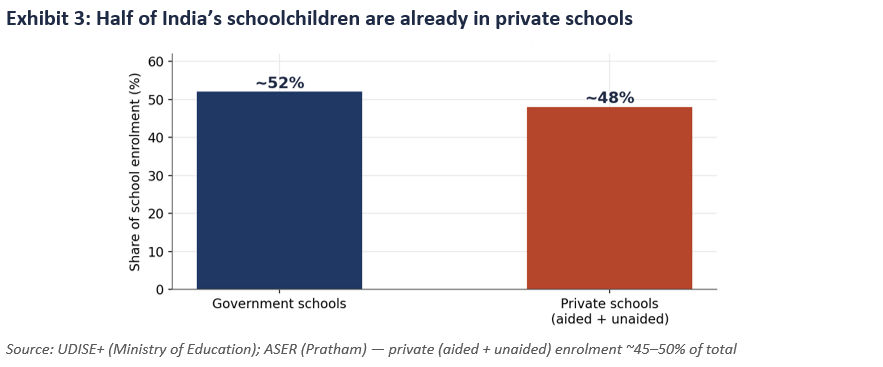

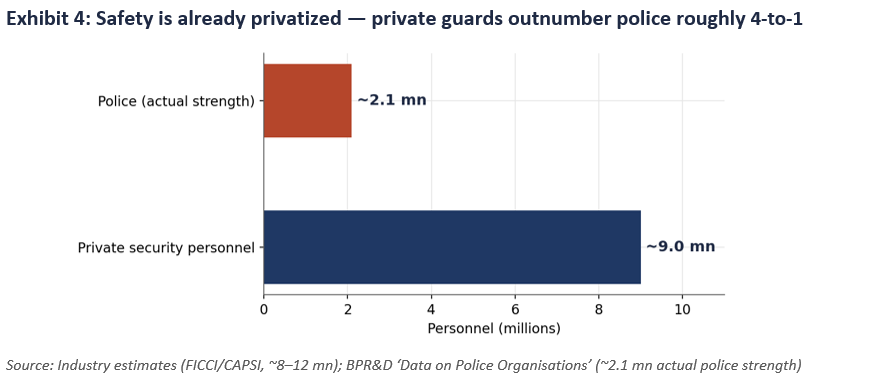

As fiscally squeezed nation states retreat from providing the essentials of life, the private sector steps in to provide public goods. In India, 47% of healthcare is paid out of pocket; roughly half of schoolchildren are in private schools; and 9 million private security guards compare against 2.1 million police. The wealth from this great privatisation accrues to a narrow elite — the top 1% now takes ~23% of Indian income and holds ~40% of India’s wealth. The rational response is to position your portfolio for the world you actually live in, not the one on the by: 1) Owning the private providers of public services; 2) Owning wealth managers & luxury good providers; and 3) Holding a significant part of your wealth outside the Indian stock market.

Contact with us through connect.marcellus.in if you would like to do any of these via us.

The Deal Every Indian Professional Thinks They Live Under…

Every Indian professional carries an implicit mental model of the country, installed so early that we never examine it. It goes like this: the state provides the essentials of life — schools for our children, hospitals for our parents, police for our streets — and in exchange we pay our taxes and keep our savings inside the domestic financial system. We argue endlessly about whether the state does this job well. We almost never ask whether it still does the job at all.

Our money reflects that unexamined trust. The typical affluent Indian portfolio is almost entirely in rupees and almost entirely in India — deposits, property, domestic equities. Economists call this ‘home bias’; in India’s case it is closer to home monogamy. It feels safe because, in the mental model, the state stands behind the whole system: that’s what we have been taught since kindergarten.

…Has Already Ended: Three Numbers That Prove It

1. Healthcare: 47%

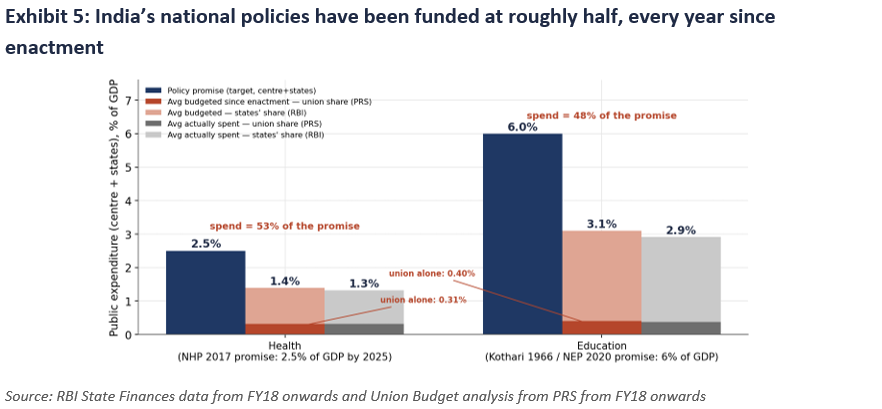

47% of Indian healthcare is paid for out of pocket — by families, at the point of illness — against a world average of about 18%. This is because the Indian state spends roughly 1.9% of GDP on health against its own National Health Policy target of 2.5%. The WHO has documented that these out-of-pocket payments push tens of millions of Indians below the poverty line every year. You or your employers already buy your family’s healthcare privately. We at Marcellus capitalize on these trends by investing in the shares of private sector insurers, private hospitals and privately owned diagnostics providers.

2. Education: ~50%

Roughly half of India’s schoolchildren are already in private schools — and the share has risen for two decades even among low-income rural households, as the Annual Status of Education surveys document year after year. The public spend on education runs at about 2.9% of GDP against the 6% target that has stood since the Kothari Commission recommended it in 1966 — a target reaffirmed, and missed, by every government since, most recently in the National Education Policy of 2020. You already buy your children’s education privately.

3. Safety: 9 million private versus 2.1 million state/public funded

India employs roughly nine million private security guards against an actual police strength of about 2.1 million — four private guards for every police officer, in a country whose police-to-population ratio (~150 per lakh) runs well below the UN-recommended 222. The guard at your gate, the one at your office, the one at the mall means that you already buy your safety privately.

Why the Deal Ended: A State That Cannot Completely Fund Its Policies

This is not a story about lack of intentions; it is a story about arithmetic. As we argued in Part 1 of this series (The Fading Nation State. Part 1: The Twilight of National Investing), a government that cannot tax mobile capital — corporate rates were cut nearly ten points in 2019 for fear investment would go elsewhere — and whose income-tax net covers fewer than forty million people in a nation of 1.4 billion, simply cannot close a three-percentage-point provision gap on health and education, however sincere its intentions.

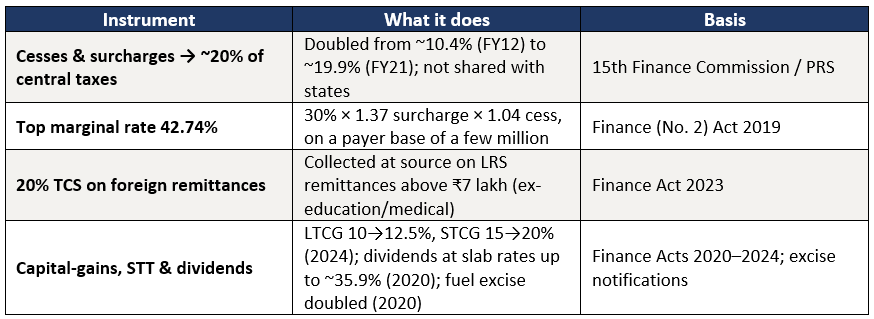

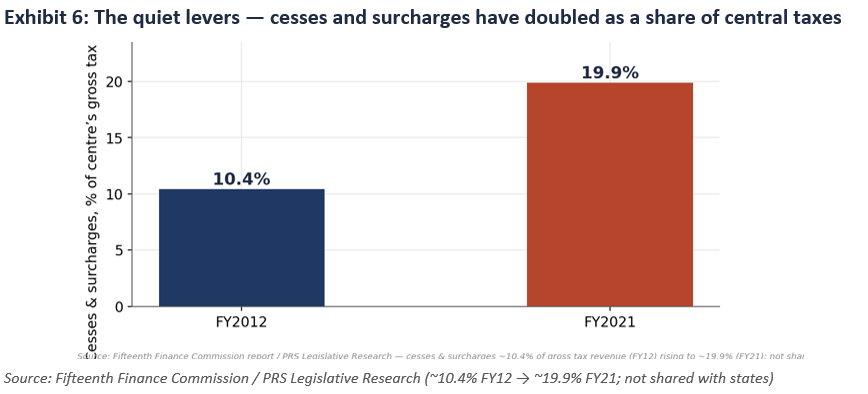

Here the story becomes uncomfortable. A state that no longer buys the middle class’s loyalty through provision — because that class has already exited to private schools, private hospitals and private guards — shifts, incrementally, to collecting from whatever cannot move. Consider the toolkit already captured in the Gazette of India:

Three Ways You Can Prepare for the World You Actually Live In

You are already living in the post-nation-state economy — paying privately for everything the state once provided for, while the state collects more from you at higher rates and stands tolling the exit. So, what should you do?

First, own the private providers of what you are already buying. Essentials purchased privately are relatively safer bets that the equity markets offer to investors with a growth kicker, with non-discretionary demand, pricing power, and a secular volume shifting as the state recedes. Hospitals, diagnostics, health insurers, education services, security services, and the businesses that sell water and power reliability — this is the listed expression of Exhibits 2 to 4. The one condition: these are trust businesses on morally charged ground, and the durable winners will be those who stay on the right side of the affordability line. Marcellus’ domestic PMS portfolios have large investments in hospitals, diagnostics, pharma and general insurance.

Second, own the consumption of those who gained. The wealth created by this great privatisation accrues to a narrow cohort — see Exhibit 1 — and concentrated wealth expresses itself exactly as Thorstein Veblen predicted 125 years ago: conspicuously. The global personal-luxury market has roughly tripled this century, and India is among its fastest-growing frontiers — which is why the world’s luxury champions, none of them listed in India, belong in an Indian investor’s opportunity set. Marcellus’ domestic portfolios benefit from the booming businesses of wealth managers in India. Our global portfolios have a hefty allocation to ultra-luxury companies who are doing booming business in India.

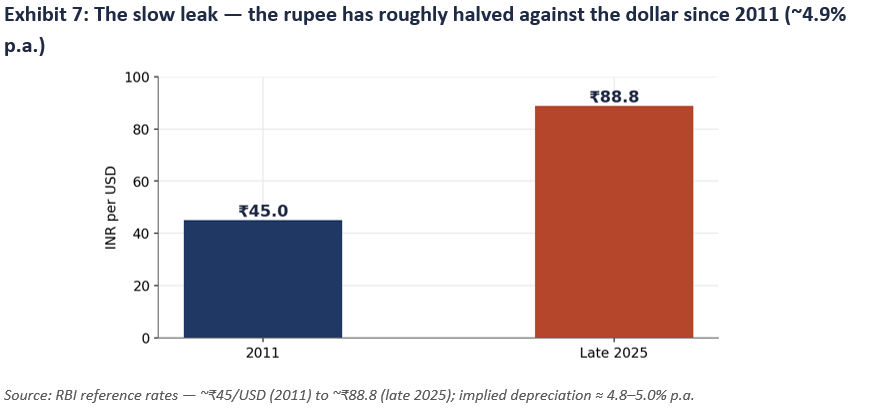

Third — and this is the insurance that makes the other two safe — hold part of your wealth outside India. Indian household portfolios are almost perfectly home-biased despite the classical finance result that global diversification improves risk-adjusted returns, and despite a rupee that has roughly halved against the dollar since 2011 — a drag of close to 4-5% a year on every rupee asset before any question of relative stock returns. The 20% TCS is a cash-flow drag, creditable against tax — read it as the hinges creaking, not as a reason to stay inside.

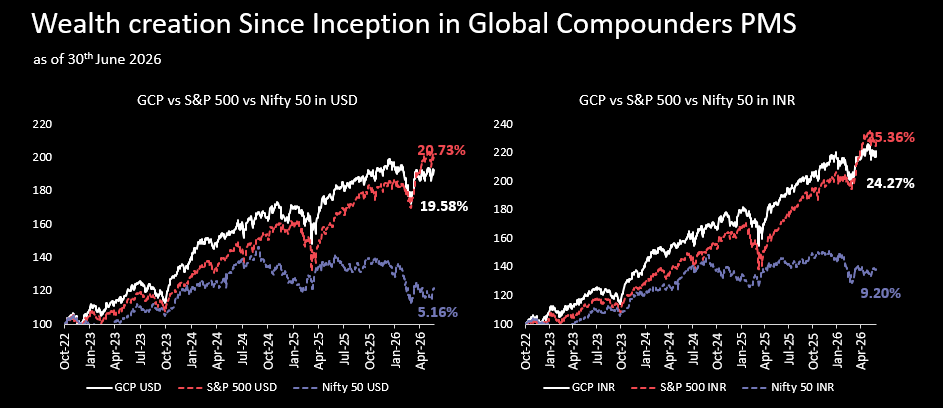

Through its offices in GIFT City, Gujarat, Marcellus offers multiple funds through which investors can access the world’s largest stock markets. Ticket sizes begin at around US$5,000 (approximately ₹4.5 lakh), subject to the specific product, regulatory classification and investor eligibility. Our flagship global product is the Global Compounders Portfolio, whose track record is shown below.

Global Compounders Portfolio — wealth creation since inception

Note: *Since Inception performance calculated from 31st Oct 2022. The date of inception is 31st Oct 2022, being the next business day after the account got funded on 28th October 2022. S&P 500 net total return is calculated by considering both capital appreciation and dividend payouts. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the IFSCA or US SEC. Performance is the combined performance of RI and NRI strategies. S&P 500 NTR is the benchmark for the strategy. Nifty 50 is provided for reference to illustrate the relative performance of the US and Indian markets. Past performance pertains to Marcellus’ GCP PMS strategy, not to this IFSC Retail Scheme and is not indicative of future results.

Marcellus GCP PMS is offered by Marcellus Investment Managers GIFT Branch in a segregated managed accounts format.

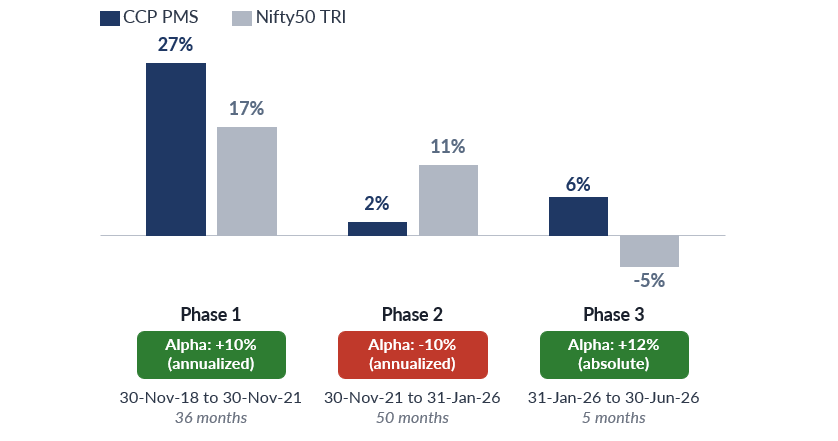

In our Consistent Compounders Portfolio (CCP), we invest in Indian providers of hospitals, diagnostics, pharma and general insurance. More generally, this portfolio focuses on investing in clean, well-managed franchises providing essential goods & services to Indian households and companies.

Consistent Compounders Portfolio — CCP PMS vs Nifty50 TRI, annualized returns by phase

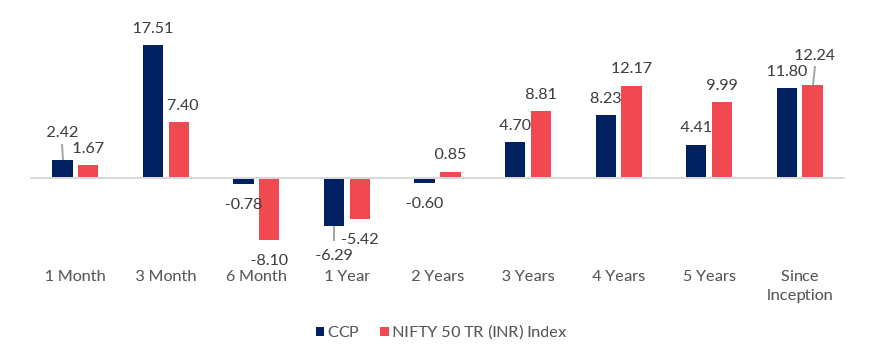

Consistent Compounders Portfolio — CCP performance vs Nifty50 TRI, by period (in %)

Source: Marcellus Investment Managers; Performance Data shown is net of fixed fees and expenses charged till the last quarter end and is net of Performance fees charged for client accounts, whose account anniversary / performance calculation date falls upto the last date of this performance period; 1 month, 3 months & 6 months returns are absolute; other time period returns are annualized. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the SEC, SEBI or any other regulatory authority.

*For relative performance of particular Investment Approach to other Portfolio Managers within the selected strategy, please refer https://www.apmiindia.org/apmi/, Under PMS Provider Name please select Marcellus Investment Managers Private Limited and select your Investment Approach Name for viewing the stated disclosure.

If you would like to invest with us, please scan the QR code below.

Thanks,

Saurabh Mukherjea

Click here for details about our regulatory registration and licensing information.

Disclaimer:

The above material is neither investment research, nor investment advice. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the International Financial Service Centre Authority (Fund Management) Regulations, 2025 (“IFSCA”) as Fund Management Entity – Retail, rendering Investment Management Services. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by SEBI as a provider of Portfolio Management Services and acts as an Investment Manager to an Alternative Investment Fund. Marcellus is also registered with US Securities and Exchange Commission (US SEC) as an Investment Advisor. No content of this publication including the performance related information is verified by SEBI, IFSCA or US SEC. If any recipient or reader of this material is based outside India or US, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and be able to access and use this material in any manner by anyone. This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form. Data/information used in the preparation of this material is dated and may or may not be relevant any time after the issuance of this material. Marcellus takes no responsibility to update any data/information in this material from time to time. The recipient of this material is solely responsible for any action taken based on this material. The recipient of this material is urged to read the Disclosure Document/Form ADV, Form CRS and any other documents or disclosures provided to them by Marcellus, as applicable, and is advised to consult their own legal and tax consultants/advisors before making any investment in the portfolio. All recipients of this material must before dealing and or transacting in any of the products referred to in this material must make their own investigation, seek appropriate professional advice and carefully read the Disclosure Document, Form ADV, Form CRS and any other documents or disclosures provided to them by Marcellus, as applicable. Actual results may differ materially from those suggested in this note due to risk or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions globally, inflation, etc. There is no assurance or guarantee that the objectives of the investment strategy/approach will be achieved. This material may include “forward looking statements”. All forward-looking statements involve risk and uncertainty. Any forward-looking statements contained in this document speak only as of the date on which they are made. Further, past performance is not indicative of future results. Marcellus clients, Marcellus clients, employees, and/or its associates, including the authors of this material (and their relatives), may have financial interests by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus and any of its directors, officers, employees and any other persons associated with this shall not be liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner whatsoever and shall not be liable for updating the document. This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.