| Introduction: China and India’s contrasting fortunes

With the recent ‘elections’ to the Chinese Communist Party’s Politburo resulting in the exit of all economic reformers from the Politburo and their replacement by military men and spies loyal to Xi Jinping, scarcely a day passes now without a Western government acting to ‘contain’ China. Alongside this, China’s never ending Covid-19 lockdowns – thanks to the lack of a credible Covid vaccination campaign – are exacerbating the economic slowdown in the country.

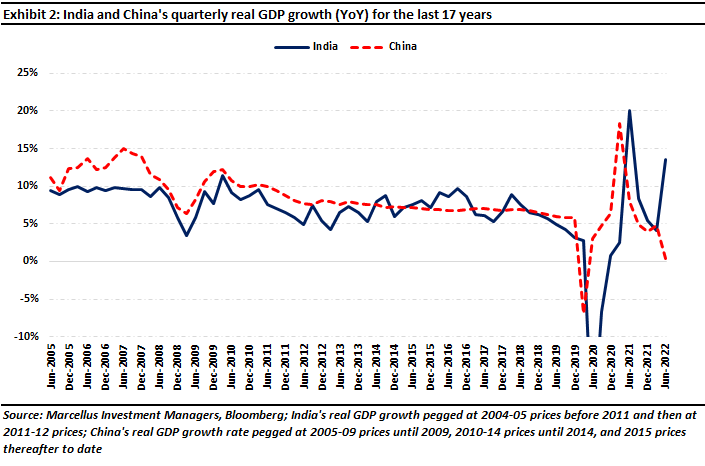

Even as China experiences social, political, and economic turmoil, the Indian economy seems to be in fine fettle – Exhibit 2 visually demonstrates the contrasting fortunes of Asia’s two biggest economies. The Government of India’s tax collections are growing at 34% YoY, more than twice as fast as the nominal GDP growth. Credit growth in the banking system is running at 18% YoY, the highest in a decade. Motor car and truck sales are growing at 13-26% YoY (source: Society of Indian Automobile Manufacturers, 2022).

More importantly for India, as China unravels, the possibility grows by the passing month that large chunks of the Chinese economy will migrate to other, more stable, countries including (but not restricted to) India. As Peter Zeihan writes in his recent bestselling book ‘The End of the World is Just The Beginning: Mapping the Collapse of Globalization’ (2022), “China absolutely faces deindustrialization and deurbanization on a scale that is nothing less than mythic…India, with all its endless internal variation, hopes to take a bite out of everything.”

The question therefore is which segments of the Chinese economy can India aspire to yank away.

Smartphones and the ancillaries related to it

- In contrast India exports a mere $6 bn of smartphones (sources here and here), and

What is India’s ‘right to win’ here? In other words, why do we believe India can be competitive in the large-scale manufacture of smartphones? Given that the gap between India and China’s exports in smartphones is massive and India still imports around 60% of smartphones from China, just internalising its $27bn p.a. of smartphone imports from China will give India the first layer of manufacturing presence in this sector. In this context, the $1.1 bn p.a. of Production Linked Incentives (PLI) can help shift the manufacture of India’s domestically consumed smartphones from China to India.

Over and above the domestic consumption of smartphones, we already know from Apple’s announcements that: (a) over the last 8 months, it has already exported $1.3 bn worth of iPhones from India and plans to shift over the next couple of years a significant part of its iPhone production to India; (b) it plans to make its AirPods in India; and (c) it is having trouble making the other ~$200 bn of iPhones in Foxconn’s factories in China due to Covid lockdowns.

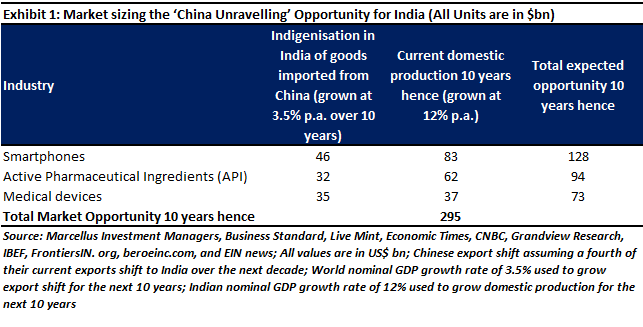

Opportunity size: As explained in the preceding para and according to a Bloomberg report, Apple plans to shift 25% of its iPhone production to India by 2025), which is approximately $50 bn (i.e., 25% of total iPhone production). Even if Apple ends up shifting only half of this target, which amounts to $25 bn per annum of iPhones (iPads and AirPods are over and above this) to India, it will give India a close to $60bn per annum smartphone manufacturing sector over the next couple of years.

In the longer term, if we assume that a fourth of China’s exports shift to India over the next decade and the Indian domestic market continues to grow at 12% p.a. (at nominal GDP growth rate), an opportunity of close to $130 bn will be created in India in the smartphone industry in the next 10 years.

Have we seen investments being announced in this space?

APIs and the ancillaries related to it

What is India’s ‘right to win’ here? As the West gets increasingly apprehensive about its dependence on China for APIs, the next natural preferred location of choice for API production is India given: (a) the production capacity that already exists in the country; (b) the process chemistry knowhow that already exists in India; and (c) that no other country barring India and China produce API on a large scale.

A second dimension to consider, is that not only can India displace China to some extent as an API supplier to the West, but India can also reduce its own dependence on China for APIs.

Opportunity size: if we assume that over the next decade a fourth of Chinese API exports transfer to India, and India’s domestic consumption to increase steadily at 12% p.a. (at nominal GDP growth rate), the sector has the potential to expand to $94 bn in a decade hence.

Have we seen investments being announced in this space?

- The government of India approved a PLI scheme of around $2 bn in 2021. To this end, 35 APIs which had a 90% import dependence (mainly from China) are now being manufactured in 32 different plants in the country. Around 55 companies in this space, as a result, have benefitted from this scheme

- Laurus Labs, a company involved in production of APIs for specific generic drugs, has invested $600 mn each in API manufacturing and formulation facilities until now

Medical devices and the ancillaries related to it

What is India’s ‘right to win’ here? Given the mismatch in size between India and China’s medical device industries, clearly India cannot be cost competitive in this sector even with $2.5 bn of PLIs kicking in. However, India’s trump card is that Western governments are wary of their reliance on China for diagnostic and therapeutic medical devices. In 2016, therapeutic devices (like orthopaedic appliances and parts, hearing aids, artificial joints, pacemakers etc.), which typically are either inserted in the human body or are at least in close contact with it, accounted for around 31% of all medical devices exported by China, with both therapeutic and diagnostic equipment constituting about 52% of all medical devices exported by the country. The same Covid related production issues which are impacting Apple in China are also impacting the production of medical devices in China.

In addition, the increasingly erratic behavior of China’s legal system when dealing with entrepreneurs who are not in Xi Jinping’s good books has also alarmed MNCs and made them wake up to the fact that they have zero IP protection there. As a result, Western manufacturers and users of medical devices are keen to reduce their dependence on China and make cost a secondary consideration. This gives India an opportunity to grow its domestic production from the current pitifully small figure of $2 bn.

Opportunity size: Even if one assumes that over the next decade, only a fourth of China’s exports migrate to India and India’s domestic consumption of medical continues to grow at 12% per annum (i.e., nominal GDP growth), a decade hence this sector could be crossing $70 bn in size in the next 10 years.

Have we seen investments being announced in this space?

- “In July 2022, Godrej Appliances launched the new InsuliCool product range – Godrej InsuliCool and Godrej InsuliCool+, which are innovative cooling solutions especially designed for insulin storage, in order to address the challenge faced by diabetic patients with respect to insulin storage at recommended temperatures.”

Marcellus’ current investments to capitalize on this $300bn opportunity.

Tarsons Products, a company that manufactures quality plastic labware, is a case in point for the benefit that Indian companies can derive due to incremental business coming into the country due to the China + 1 dynamic playing out. For Tarsons, the competition in the export markets is from global competitors, including Chinese players. Now, as the Chinese struggle, Indian companies like Tarsons are in a prime position to leverage this situation and establish their hegemony in not only the domestic space (which it already is doing), but also all across the globe, thus creating a massive opportunity for the company and its shareholders. As we had pointed out in our October 2022 Little Champs Portfolio (LCP) newsletter – The Little Champs Are Prepared for Western Turmoil, “Over the past decade, Tarsons has successfully replicated its domestic competitive advantage in the global market, i.e., its USP to sell high quality products at lower price points. Given the size of the Global Plastic Labware industry (US$) 8.4bn, Tarsons has a long growth runway… (as a result) New manufacturing facility in West Bengal (is) to be commissioned by middle of 2023.”

GMM Pfaudler is another example of this dynamic playing out. GMM manufactures the glass lined reactors that API manufacturers and pharma companies need to make their products. The company recently acquired:

- Assets of DDPS India (the Indian subsidiary of a French glass lined reactor manufacturer, De Dietrich) for €6.25 mn

- A 54% stake in Pfaudler’s global business for US$27.4 mn; and

- Assets of HDO Tech for augmenting heavy engineering capabilities

This has essentially translated into GMM being the leader in Glass-Lined Equipment (being ~2x the size of its closest peer) not only in India, but across the globe with massive economies of scale alongside high productivity and low-cost labour (GMM’s plants in India are thrice as productive as their plants in USA) as compared to the global behemoths.

Our October 2022 Little Champs Portfolio (LCP) newsletter – The Little Champs Are Prepared for Western Turmoil, gives details of the extent of GMM’s dominance – “GMM has been for long the domestic leader in the supply of glass lined equipment (GLE) in India. The Company recently acquired the global business of its parent Pfaudler which makes the combined entity the dominant player in the global GLE industry.”

Alkyl Amines, leader in production of chemicals like aliphatic amines, acetonitrile, and dimethylamine hydrochloride (DMA HCL) which are the key components in a multitude of pharmaceutical products, has been using its position as the lowest cost producer to its benefit. Because of the aforementioned dynamic playing out in the API industry, the chemicals that are produced by companies like Alkyl will become ever more critical for India. Unsurprisingly, Alkyl is investing in new plant & capacity as it gets ready for the demand ramp-up: “(Alkyl has) Commissioned new Acetonitrile plant in November 2021. Expansion of Aliphatic Amines’ capacities at existing plants to the tune of Rs3.0-3.5bn… Through constant capacity expansions and being one of the lowest cost producers globally, Alkyl ranks amongst the top 3 global players in some of its products like Acetonitrile, DMA HCL, etc.” (source: The Little Champs Are Prepared for Western Turmoil, 2022).

Divi’s Laboratories, a leading manufacturer of generic APIs and nutraceutical ingredients, has again utilized its position of being a reliable and timely supplier to Big Pharma, establishing its superiority in the space. Its ability to deliver products as per specified quality parameters within the contracted time and that too at a very large scale underpins the success of Divi’s Labs. Assured supply is the most critical aspect for any major pharmaceutical company that typically outsources their API production. A delay in supply or challenges in quality would have significant adverse impact on their brand reputation and market share in their respective markets. Further, issues in quality of API also poses the risk of punitive regulatory action. Therefore Divi’s, with its track-record of quality supply in a time bound manner, has entrenched deeply in its client’s supply chains for relevant products.

Furthermore, Divi’s is amongst the few API players globally (outside China) who have undertaken backward integration of their major key starting materials. This helps them control costs and also provides assurance of continued supply. Due to this backward integration (coupled with continuous debottlenecking of plants), Divi’s is the global cost champion for many of its APIs such as naproxen, dextromethorphan, and levetiracetam. Given the backdrop of the shift in API manufacturing to India, companies like Divi’s can win big. |