| Failures in any domain can be broadly attributed to two reasons:

1) Due to ignorance: Failures caused by lack of awareness or non-acknowledgement. These are typically errors of omission.

2) Due to ineptitude: Failures caused by not completing or executing the process properly. These are typically errors of commission.

Failures due to ignorance are a lesser problem today due to availability of trained professionals and specialists in nearly all domains. Failure due to ineptitude, in most cases, are completely avoidable and more of a concern in contemporary life given the growing complexity in almost all domains.

In “The Checklist Manifesto: How to Get Things Right” (2009), author Dr. Atul Gawande talks about the importance of having a checklist in almost any discipline to reduce failures due to ineptitude. As Dr. Gawande highlights in the book, checklists are useful for breaking down complex tasks into manageable steps and then ensuring that these steps are being followed in a consistent manner to avoid mistakes. Before we demonstrate the application of checklists to our quant investing process, using Dr. Gawande’s bestselling book, we exemplify the use of checklists in three other industries – Aviation, Medicine, and Construction.

Aviation

Checklists have been used since for many decades in aviation. The complexity of modern commercial airliners has grown to a point where it is too difficult for a pilot (even with a co-pilot) to memorize and handle all the complex tasks of flying the plane safely and reliably. Boeing, one of the largest airplane manufacturers in the world, pioneered the use of checklists for flying the B-17 bombers in the late 1930s. These bombers proved instrumental in the Allied bombing of Germany during WWII. Today airline pilots rely on checklists universally for routine tasks like take-off, landing, taxiing on the runaway, and dealing with emergency situations, among others. Checklists ensure that the pilots follow all procedures in completing these tasks precisely and unfailingly.

In 2009, the world was captivated by the scenes on TV of a plane in the Hudson River as passengers stood on the wings waiting to be rescued. Despite the loss of both engines shortly after take-off, all the passengers and crew of US Airways flight 1549 were saved because of the quick actions of Captain Chesley “Sully” Sullenberger who landed the plane on the river.

One of the first things Captain Sully asked his co-pilot to do upon the loss of thrust in both the engines was pull out the checklist. Unlike the story reported in mainstream media which made out Sully as the sole hero, Sully himself credited teamwork and adherence to protocol, not his skill flying the plane, for saving lives on that day. The story of US Airways Flight 1549 is a great example of the power of the checklist.

Medicine

In 2001, Peter Pronovost who was a critical-care specialist at Johns Hopkins Hospital noticed that about forty thousand people in the United States died each year from infections caused by central line catheters i.e., intravenous tubes placed in patients as part of their treatment. These deaths typically showed up as post-surgery complications but were completely preventable. Yet the number of people dying from these infections was equal to the number of women dying from breast cancer each year in the US.

To address this, Pronovost came up with a checklist to take care of simple but important tasks like ensuring hygiene at the time of inserting the line like washing hands, ensuring the patient’s skin is washed with antiseptic, ensuring the patient is covered with sterile drapes, and checking the line regularly for any infection etc., hence reducing the likelihood of line infections. This resulted in up to 66% reduction in the rates of catheter-related post-surgery infections. Pronovost’s celebrated study can be accessed here.

Dr. Atul Gawande, a surgeon himself, and a team of researchers studied if surgeons might perform better with checklists in operating rooms. The list had some basic reminders, such as confirming that blood and antibiotics were on hand and making sure everyone in the room knew each other by name.

They tested the safety checklist at eight hospitals and found some striking results: The average number of complications and deaths dipped by 35%. Based on Dr. Gawande’s work, the WHO has devised a simple surgical checklist that has been adopted in more than 20 countries as the standard of care.

In general, researchers have found that simply having the doctors and nurses in the ICU create their own checklists (for what they thought should be done each day) improved consistency of care to the point that the average length of patient stays in intensive care dropped by half.

Investing

In the late 1990s, a researcher called Geoff Smart studied how venture capitalists assess senior managers of prospective new venture investments prior to making a final investment decision. These venture capitalists must give a yes or no to high-risk, multi-million-dollar investments in unproven start-ups, in the hope of finding the next Google or Apple.

Smart learnt that finding a good idea is apparently not that difficult but finding an entrepreneur who can execute a good idea is a different matter entirely. You need a person who can take the idea from proposal to reality, work the long hours, build a team, handle the pressures and setbacks, manage technical and people problems alike, and stick with the effort for years on end without getting distracted or going insane. Such people are not only rare, but they are also extremely hard to spot.

Smart identified different ways the venture capitalists use to identify such people. These were styles of thinking, really. He called one type of investor the “art critic”. These investors assessed entrepreneurs almost at a glance, the way a critic can assess the quality of a painting – intuitively and based on experience. “Sponges” took more time gathering information about their targets, soaking up whatever they could from interviews, on-site visits, references and the like. Then they followed their gut. The “prosecutors” aggressively interrogated entrepreneurs; “suitors” focused more on wooing people than on evaluating them; “terminators” saw the whole effort as doomed to failure and skipped the evaluation part. They simply invested in what they thought were the best ideas, fired the entrepreneurs they found to be incompetent and hired replacements. And then there were the “airline captains”. Studying past mistakes and lessons from others in the field, they built formal checks into their process. They forced themselves to be disciplined and not to skip steps, even when they found an entrepreneur, they “knew” intuitively was a real prospect. Why were these last, methodical types labelled “airline captains”? Because as we discussed in the previous section, four generations after the first aviation checklists went into use, today they are deemed necessary to get giant, complicated machines off the ground and fly over oceans and continents with minimum risk to passengers.

Smart tracked the venture capitalists’ success over time, and it became clear that the airline captains had by far the most effective style. Those investors taking the checklist-driven approach had a 10% likelihood of later having to fire senior management for incompetence or concluding that their original evaluation was inaccurate. The other cohorts had at least a 50% likelihood. These results showed up in terms of differences in investment performance too. The airline captains had a median return of 80% on the investments studied, compared to 35% or less for others. Those with other styles were not failures by any stretch – experience does count for something. But those who added checklists to experience proved substantially more successful.

Smart’s most interesting discovery was not the relative success of the airline captains. Rather, it was that most of his subjects were either art critics or sponges – intuitive decision-makers instead of systematic analysts. Only one in eight took the airline captain approach. Smart’s full study can be found here.

Applying checklists to create the MeritorQ quant investing process

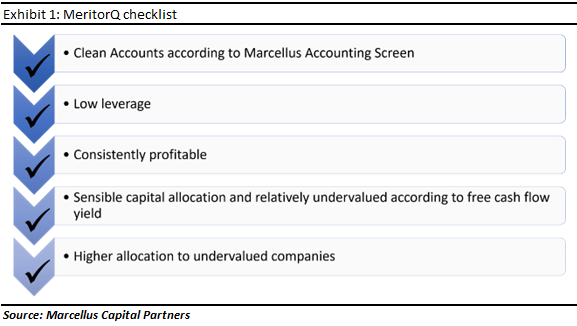

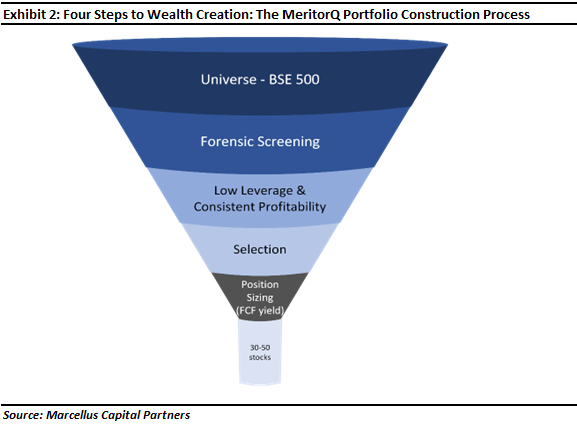

In a similar vein, the investment rules in MeritorQ (shown below) can be thought of as automated checklist applied regularly with minimal discretion. Investment checklists help in reducing mistakes and outperform consistently by sticking to an objective, systematic process.

Good investing is as much about avoiding wealth destroying companies as picking winners. MeritorQ’s rules-based approach can be thought of as a checklist. The steps in this checklist (as shown in Exhibit 1), start from the BSE 500 universe and proceed as follows:

Clean Accounts according to Marcellus Accounting Screen: As we have highlighted previously in our books and in our newsletters, companies with governance issues and accounting irregularities in a broad-based index like the BSE 500 can lead to permanent loss of capital. So, we remove earnings manipulators and other such companies in this step.

Low leverage: High leverage can be a double-edged sword, given the proclivity of highly leveraged firms to unravel just as quickly as they rise to the top. Given the focus in MeritorQ is to generate consistent returns, we thus remove highly leveraged companies in this step.

Consistently profitable: This step ensures that companies with very cyclical businesses and those which have not demonstrated a track record of sustainable profitability are removed.

Sensible capital allocation and relatively undervalued: This step allows us to select cheap as well as quality companies, while avoiding value traps or overpaying for quality.

The last step in MeritorQ’s checklist then assigns higher allocations to more undervalued companies in the final portfolio.

All these steps have been rigorously back tested over the last 16 years and backed up by empirical evidence for their effectiveness in other markets as well. For example,

- As discussed here, over last roughly 95 years for which data is available for US stocks, the excess returns of from investing in value stocks has averaged 4.2% per year in the US. Similar, “value” premium has been shown to exist in Japan, Europe and other global markets as well.

- As discussed in this study, most of Warren Buffet’s returns can be explained by his focus on cheap, safe and quality stocks combined with the use of leverage. Except for leverage we employ a similar strategy in MeritorQ.

We go through this checklist twice in a year in April and October to create new portfolios, which we call rebalancing. Doing this allows us to reflect any changes in business fundamentals while also regularly picking up undervalued companies and selling those which have reached their fair value.

As Warren Buffet once said, “Investing is simple but not easy”. Most of us don’t spend time dwelling on our errors. But if we did, we could create checklists that would eliminate those errors. To adopt a checklist is to embrace humility and admit our own fallibility.

As we discussed in our previous newsletter dated December 2022, Strength Lies in Numbers, none of us are immune to biases and heuristics while taking investment decisions. MeritorQ’s disciplined checklist approach ensures that the investment rules are applied without any exceptions while avoiding ad-hoc timing based on market conditions (since these rules are applied regularly at a fixed semi-annual frequency).

Further, selecting undervalued stocks and overweighting them in the portfolio combined with regular rebalancing and automated checklist approach of MeritorQ, can help investors address cognitive biases and capitalize on the behavioral and analytical errors of other investors.

Since its launch on 25th October 2022, MeritorQ has generated 0.65% return whilst the NIFTY 500 Total Return Index has returned 2.02% as of 30th December 2022. The returns for MeritorQ are stated in terms of price returns and calculated net of advisory fees, gross of taxes, brokerage charges or any other transactional cost. Performance data is not verified either by Securities and Exchange Board of India or U.S. Securities and Exchange Commission.

To invest in MeritorQ, please go to https://marcellus.wealthdesk.in/wealthbaskets

If you would like to know more about MeritorQ, please write to help.ia@marcellus.in. |