Periodic rebalancing or re-alignment of the MeritorQ portfolio is as necessary as watering a plant periodically to help it grow – do it too often and the plant may rot; on the other hand, never do it and the plant dies. In MeritorQ we identify quality yet relatively undervalued companies (our newsletters Forensic Accounting Using Quant Methods Boosts Returns and The Value of Free Cash Flows explain at length about this). Rebalancing MeritorQ allows investors to benefit from: (1) Mean reversion in Price to Free Cash Flow multiples, (2) Invest in the next set of undervalued stocks; and (3) Reduce concentration risk. Thus, periodic rebalancing, as we like to call this refresh, not only helps in improving performance but also functions as a risk-mitigation tool.

What is rebalancing and why do we need it?

Rebalancing can be understood as a realignment of the portfolio to restore balance. For instance, as per the seasons and weather conditions, you need to alter the kinds of food that you would consume; during summer you would probably go heavy on roughage and water and maybe cut down on fats and carbohydrates, whereas during winters, you may wish to consume more fats and carbohydrates.

Likewise, rebalancing can be thought of as a periodic portfolio refresh to keep an investment strategy aligned with overall investment objectives. This alignment could take different forms, for example, investors might choose to rebalance to reflect new information on prices or fundamentals of portfolio companies, among others. In MeritorQ, rebalancing involves refreshing the portfolio as of the first trading date of April and October basis the investment checklist, as discussed in our January newsletter, “MeritorQ: The Power of Checklists”. Because rebalancing necessarily involves portfolio trades, the cost of rebalancing needs to be compared with the intended benefits.

How does rebalancing help investors?

Rebalancing of portfolios is more common than one would presume – intuitively investors do load up on securities which may have witnessed a sharp fall (for example the Covid induced crash in March 2020). Yet higher turnover is perceived as a one-way street with higher churn equaling higher costs for the investor. Not rebalancing during the investment horizon creates the risk of the investment strategy drifting too far from its investment objectives and not reflecting new information.

Rebalancing in this context is therefore like that pungent spice in food – put too much of it and it can ruin the taste (like the costs from higher portfolio turnover), and if not added at all, the food may taste bland (akin to the disappointment from lower returns).

Regularly investing in quality undervalued companies’ basis their free cashflows

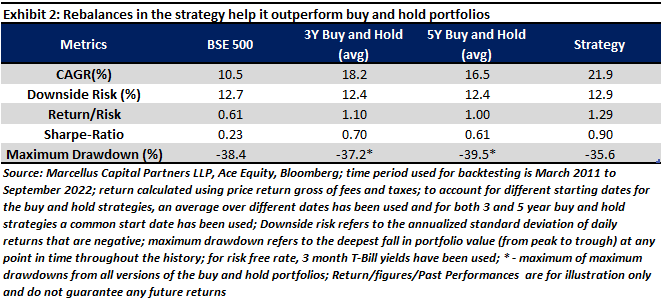

To understand why frequently rebalancing the portfolio is beneficial, let’s look at the counter case – what if one buys and holds a portfolio (created based on MeritorQ’s construction rules) for a certain period of time without touching the portfolio at all in between. Let’s say, you invest in a 3-year duration portfolio, hold it for the entire duration and then liquidate to invest in the next 3-year portfolio. We created all possible combinations of these 3-year buy and hold portfolios, with different starting dates, between September-2006 to September-2022. This is represented visually in the following exhibit.

Now, let’s say, you also do this for a 5-year holding period – i.e., you buy and hold a portfolio for 5 years using the same process as above. Assuming a common starting point for these strategies and taking an average of the different time periods when the unique portfolios begin and run, we can clearly see (in the exhibit2) that a strategy like MeritorQ (which is rebalanced semi-annually) outperforms the 3-year and 5-year ‘buy and hold’ portfolios, not only on absolute returns basis but also on risk adjusted returns basis.

Since we select and allocate more to relatively undervalued companies in MeritorQ, the returns of the strategy are partly driven by investing from the reversion to mean of out of favor or undervalued stocks (measured on a relative basis using Price to Free Cash Flows). As explained in our November 2022 newsletter, “MeritorQ: The Moneyball of Quality Investing”, the selection and position sizing steps add roughly 3.6% points to overall back tested performance. Our screening steps – where we look for companies with clean accounts, consistent profitability, and low leverage – ensure that undervaluation is more due to transitory factors like a recent loss of market share, negative sentiment around the stock or sector etc. than due to deteriorating fundamentals. For MeritorQ, therefore, the extent and speed of mean reversion in price to free cash flow across leading up to each rebalance, partly drives both the strategy returns as well as the turnover.

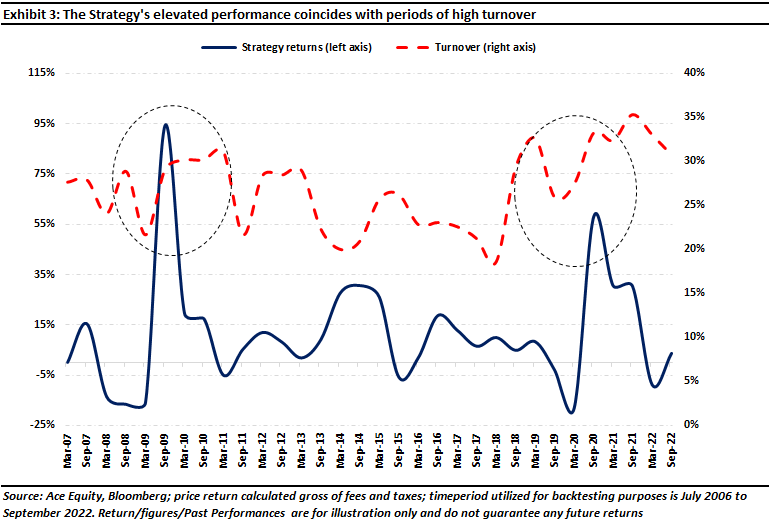

Turnover in MeritorQ comes from both:

- Overvalued stocks being replaced by more undervalued ones, and

- From having their allocation reduced depending on the extent and speed of mean reversion.

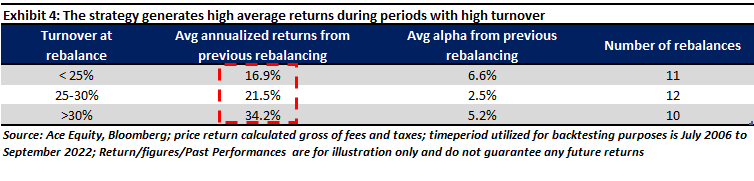

Exhibits 3 and 4 show this in more detail by comparing the returns between the semi-annual rebalancing dates and the one-way turnover on these dates in MeritorQ. Exhibit 3 shows that higher turnover around major turning points like the Global financial crisis or Covid crisis, are generally followed by higher alpha. Exhibit 4 emphasizes that historically in MeritorQ increased turnover has generally been accompanied by better returns. Key takeaways for investors are that while we have observed historical one-way turnover for the strategy is around 55%, turnover could be higher than this number during certain years. This higher turnover is, however, justified because, as exhibit 4 shows, higher portfolio turnover implies a higher probability of strong strategy returns.

| Rebalancing reflects changes in company fundamentals over time

A company’s worth is not understood predominantly by how its share price has moved, but rather by its ability to generate and sustain free cash flow in the future which in turn depends on profitability, reinvestment, and longevity of the business. In fact, empirical evidence points to the fact that over the long run, stock prices are driven by the company’s fundamentals.

In MeritorQ, we use a set of fundamental screening steps that ensure that we end up owning quality companies and, in the process, avoid value traps, that is, companies whose undervaluation is due to fundamental factors like deteriorating profitability or higher bankruptcy risk. Recall that the first screening step in MeritorQ looks for companies with clean accounts, where using a set of 11 ratios for non-financial companies, we weed out the potentially problematic companies from the universe. In fact, as recently as 2021, Procter and Gamble Health* (hereon P&G) made it past the forensic step. However, in 2022, the same company could not pass the screener. This was mostly due to its lower score on the ratios which determine how much it has been reinvesting in its business vis-à-vis how much operating cash flow the firm generates, the volatility in income other than that which comes from its core operations, how efficiently it sweats its assets and so on. Thus P&G was screened out in 2022.

Another screen that we use assesses leverage, where we eliminate companies with high debt. A case in point is when Crompton Greaves Consumer Electricals* (CGCE) was screened out in 2022 (this stock had made it in in 2021) as its debt more than tripled from Rs. 480 crores to ~Rs. 1600 crores, with its debt to equity more than doubling from ~0.3x to ~0.7x from 2021 to 2022, whereas its revenues and operating income rising only 1.1x and 1x respectively. This got flagged in our screen and the stock was not taken further into consideration for portfolio formation in the back test.

Note that the complete fiscal March year-end financial data for most Indian companies is available by end of September and hence reflected in October rebalance. The second rebalance in April (exactly six months later) primarily considers changes in relative valuation.

Reducing concentration risk

Excessive concentration in a rules-based strategy like MeritorQ is risky as unlike discretionary strategies we do not have leeway to reduce exposure during adverse events. In MeritorQ, since overvalued stocks which have their allocation reduced or removed at each rebalance tend to be those whose prices have appreciated, the rebalancing mechanism acts as an automatic check against excessive concentration in a single stock or a set of stocks.

In fact, we have observed that allocation to a single stock has never exceeded 16% as of any month end over the 16 years of back test from July-2006 to September-2022. We also observe that whenever allocation towards a stock becomes too large (i.e., greater than 10%) due to strong price appreciation, generally its allocation is reduced in over subsequent two rebalances. A case in point is that of eClerx Services*, which was part of the back tested portfolio in 2021. Its weight had swelled up to ~11% by August 2021 and remained over 10% until end of September 2021, which is when the next rebalance happened and its weight was reduced to just over 4%. eClerx’ free cashflows turned negative Rs. 550 crores in FY21 and this was reflected in its weight reduction during the first rebalance. In the next rebalance (i.e., in March 2022) the stock was removed.

The semi-annual rebalancing in MeritorQ, therefore, is a key ingredient which works together with other portfolio construction steps to enhance risk adjusted returns of the strategy.

To invest in MeritorQ through Smallcase, please go to https://marcellus.smallcase.com/

If you would like to know more about MeritorQ, please write to help.ia@marcellus.in

* The securities quoted are for illustration only and are not recommendatory |

|

|

Disclaimer: If you want to read our other published material, please visit https://marcellus.in/meritorq-advisory/

Copyright © 2023 Marcellus Capital Partners LLP., All rights reserved

Note: The above material is neither investment research, nor investment advice. Marcellus Capital Partners LLP (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as an Investment Adviser. SEBI Registration No., membership of BASL and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors. If any recipient or reader of this material is based outside India or US, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Marcellus and/or its associates, employees, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material.

This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.

Data/information used in the preparation of this material is dated and may or may not be relevant any time after the issuance of this material. Marcellus takes no responsibility of updating any data/information in this material from time to time. The recipient of this material is solely responsible for any action taken based on this material. The recipient of this material is urged to consult their own legal and tax consultants/advisors before making any investments.

All recipients of this material must before dealing and or transacting in any of the products referred to in this material must make their own investigation, seek appropriate professional advice and carefully read risk related documents or disclosures provided by Marcellus, as applicable. Actual results may differ materially from those suggested in this note due to risk or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India and other countries globally, inflation, etc. There is no assurance or guarantee that the objectives of the investment strategy/approach will be achieved.

This material may include “forward looking statements”. All forward-looking statements involve risk and uncertainty. Any forward-looking statements contained in this document speak only as of the date on which they are made. Further, past performance is not indicative of future results. Marcellus and any of its directors, officers, employees and any other persons associated with this shall not be liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner whatsoever and shall not be liable for updating the document.

Investment in securities market is subject to market risks. Read all the related documents carefully before investing.

The securities quoted are for illustration only and are not recommendatory.

Registration granted by SEBI, membership of BASL and certification from National Institute of Securities Markets (NISM) in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

Name of Investment Adviser: Marcellus Capital Partners LLP; CIN: AAN-4864; BASL membership number: BASL1879; Registered office and Correspondence address: 929 – DBS Business Center, Ground Floor, Kanakia Wall Street, Chakala, Andheri Kurla Road, Andheri (East), Mumbai – 400093; Telephone – +91(0) 22 6267 6872; SEBI Registration number – INA000017204; Principal officer: Mr. Krishnan V R, Contact No – +91 22 6931 5383, Email Id: krishnan@marcellus.in Compliance officer/grievance officer: Ms. Mansi Bhogal, Contact No: +91(0) 22 6931 5383 Email Id: mansi@marcellus.in; Grievance: grievance.ia@marcellus.in

Regards, Team Marcellus

If you want to read our other published material, please visit https://marcellus.in/pms-investment-blog/

Copyright © 2026 Marcellus Investment Managers Pvt Ltd, All rights reserved