The degree to which a firm institutionalizes it’s systems & processes is one of the biggest sources of differentiation between a high quality versus a mediocre franchise. Hence in Marcellus’ Longevity Framework, our research on “succession planning” focuses on softer aspects such as the institutionalization of the business, the quality of the independent Board Directors and clarity on the next generation family successors’ roles. Most Little Champs portfolio companies have made rapid strides in succession planning in recent years thanks to a well thought through succession roadmap, the proliferation of professionals in key roles, the democratisation of company ownership through stock options and through high-quality independent director appointments.

Performance update for the Little Champs Portfolio

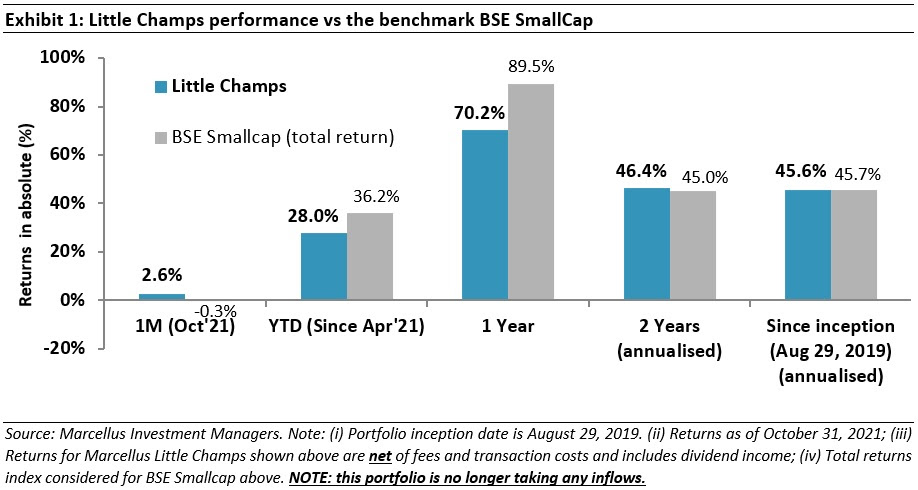

At Marcellus, the key objective of our Little Champs Portfolio is to own a portfolio of about 15-20 sector leading franchises with a stellar track record of capital allocation, clean accounts & corporate governance and at the same time high growth potential. While we intend to fill our portfolio with winners, we want to be sure of staying away from dubious names where we are not convinced about the cleanliness of accounts or the integrity of the promoters (even though the business potential may sound promising) as the fruits of company’s performance may not get shared with minority shareholders. We intend to keep the portfolio churn low (not more than 25-30% per annum) to reap the benefits of compounding as well as minimize trading costs. The Little Champs Portfolio went live on August 29, 2019. The performance so far is shown in the below table.

The criticality of succession planning in assessing the longevity of a franchise

Smaller companies are by and large family owned and family run businesses usually involving a single person at the helm of the affairs. This person, in most cases is the Founder of the company, would have shaped the journey of the company single-handedly through many ups & downs. Thus in many cases, the Founder’s skills (technical, sales and/or managerial) would have been the defining competitive advantage of the company thus far. While such a single person construct might have worked well so far, as the company expands, the rising business complexities (managing newer units, newer geographies, etc) would require delegating key responsibilities to a wider set of people and possibly even passing on the leadership mantle at an appropriate time to the next generation leader(s).

However, there are many challenges involved in transitioning towards a decentralised management construct in smaller companies. Here are a few of them:

- Reluctance on the part of the founder(s) to yield power and delegate responsibilities. This reluctance could either arise due to doubts (on the Founder’s part) regarding the capability of others or due to a belief regarding the irreplaceability of one’s own self. The stronger the cult of the Founder(s), the more difficult it is to institutionalise the business or to even start the process of doing so. In such cases, quite ironically, the strength and long tenure of the Founders itself poses the biggest hurdle in the way of the succession planning.

- Complication arising from the family ownership. The default construct in family-owned smaller companies is that the promoter’s kin, most likely her children, would assume the management of the company. This is not necessarily bad if the next generation family member(s) are sufficiently qualified and adequately groomed before they take up the leadership mantle. However, if that is not the case, it results in the company being adversely impact [and more so if the business is getting more complex in terms of size and scale]. On the other hand, it may also be very much possible that next generation family member(s) may not share the same passion about the business and may in fact be reluctant to join the company. This could create a leadership crisis if the promoter has not assessed the situation on a timely basis and is reluctant to let management control beyond the family. Yet another complication is multiple contenders within the family for the role of being the next gen leader.

- Difficulty in attracting top quality talent. Another challenge for smaller companies is even if the promoter is willing to onboard outside talent for critical roles, the smaller size of the companies and relatively unknown brand (beyond the industry ecosystem it belongs to) makes it difficult to attract and retain the right talent. This could apply for both professional management roles as well as getting on board independent directors with strong credentials.

These three issues – if not handled properly – can have a significant adverse bearing on the long-term growth potential and competitive advantages of the company. While the growth & competitive advantages of the company can be quantified, evaluating the succession planning aspect of investee companies involves a high degree of qualitative assessment. Furthermore, in the short run, “succession planning” may not seem to pose a significant risk. As a result succession planning & management continuity is an often-overlooked subject in investment research [implying that the share price of the company usually does not reflect this risk]. However, from a longer-term perspective, say beyond five years, it wouldn’t be an exaggeration to say that the degree of a company’s institutionalisation could be single biggest source of differentiator between a high quality versus a mediocre.

The Marcellus’ succession planning framework

In our October 2021 newsletter, we discussed our proprietary Longevity Framework which looks at quantitative and qualitative aspects surrounding the longevity of a company’s free cash flows. We explained that the two important tools of longevity include the lethargy and succession planning frameworks.

The lethargy framework analyses capital reinvestment initiatives being undertaken at periodic intervals by the firm to deepen its existing competitive advantages, add new revenue growth drivers and radically disrupt its own industry. We discussed the lethargy framework in detail in the October 2021 newsletter. We will focus on the succession planning framework in this month’s newsletter.

|

|

In general, the Marcellus succession planning framework tracks softer aspects such as institutionalization of the business at different levels i.e. decentralization of decision making amongst members of the Board, CXOs, as well as ground level execution through systems and processes. Specifically speaking, we evaluate the following key aspects while assigning scores to individual companies under the succession framework:

- To what extent has the promoter delegated day-to-day execution of activities?

- Does the company have a Chief Executive Officer (CEO) who is a non-promoter?

- Is there a team of well qualified and/or experienced professional management across key functions?

- Is the reporting structure in the organisation driven by the function or the family relationships?

- Do the next generation family members gradually move up the organisational hierarchy or are brought in directly at the top?

- How does the company incentive its managers/employees relative to its peers and relative to promoters’ pay-outs?

- Average tenure of the managers in the Company? Attrition rate vs the peers?

- Is there a continuous grooming of next generation managers in the Company? How often does any attrition in the key roles get filled by internal talent vs external hire?

- Quality of the Board of Directors – Do they have strong independent credentials (or are they the promoter’s lawyer/accountant)? Are they linked to promoters in any way (for instance – directorships in other promoter group companies)? Is there an adequate rotation of independent directors?

- Is the strategic decision such as capital allocation taken by the promoter himself/herself or through a proper screening committee? What role do the independent directors have in key strategic decisions?

In addition to the above, especially relevant for Little Champs portfolio is getting a sense of the succession planning within the family – whether the roles and responsibilities within the next generation family members are unambiguously defined so that there no disputes when the family patriarch moves out of the picture eventually.

The succession framework described above is more or less similar for all our portfolios (including Little Champs). However, one may argue that given the modest size of the Little Champs companies and given the stage of their evolution, whether it is reasonable to evaluate them on the similar parameters as much larger companies. Our view is that the importance of succession planning shouldn’t be discounted for smaller companies; in fact, the path to institutionalisation becomes all the more relevant for smaller companies due to heavy dependence on a single person (or a small group of persons). We also believe succession is somewhat inextricably linked to corporate governance and capital allocation – both important risks in small caps as discussed in our earlier newsletters. Furthermore, whilst a company in its current shape and form, may not have answers to all the questions highlighted above, what is more important is whether the Founders acknowledge the importance of succession planning and have the right attitude and clarity of thought to bring about required changes over the coming years.

Little Champs have, by and large, smoothly navigated the tricky issue of succession planning

The good news is that most Little Champs companies score reasonably well on the succession planning framework. A large number of portfolio companies get a score of atleast 5 out of a maximum 10 (median succession score of 5 for the 14 Little Champs portfolio portfolio) on the succession framework which is quite credible given the size and stage of their evolution. To put this into perspective, the median succession planning score for the 14 companies in our Consistent Compounders’ Portfolio is 6.5. The following aspects of Little Champs’ succession planning stand out in comparison with broader small-caps.

A. Well-thought through grooming of next generation family members

Like most of their smaller cap counterparts, Little Champs portfolio companies are predominantly family owned and family run organisations. However, what sets them apart is:

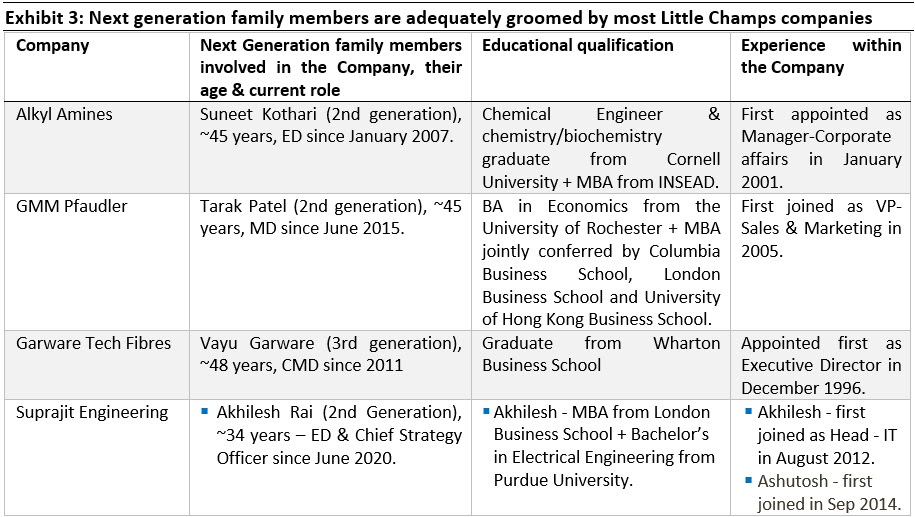

- The involvement of the next generation family members in the business at a very young age and at relatively junior positions to start with. As these individuals move up the ranks typically working across different functions, they gain extensive experience. This places them in good stead as they get ready to occupy the top positions. Exhibit 3 illustrates this for the Little Champs portfolio companies.

- Besides the above, Little Champs have been successful in clearly delineating the roles and responsibilities amongst different family members either within the group or within the company as can be seen in the case of Mold-Tek Packaging, Suprajit Engineering, Lumax Industries, Ultramarine & Pigments and Fine Organics in Exhibit 3.

|

|

Some of the Little Champs companies not mentioned in Exhibit 3 miss out due to valid reasons as explained below:

- Aavas Financiers: The company is majority owned by Private equity investors.

- V-Mart: Is promoted by first generation entrepreneur Lalit Agarwal who himself is just 51 years of age.

- Amrutanjan: S. Shambu Prasad, then ~30 years old, joined the company as non-executive director in 2004. He took over as MD in 2005 due to the demise of his father S Radhakrishna.

B. Professionalisation of the management team

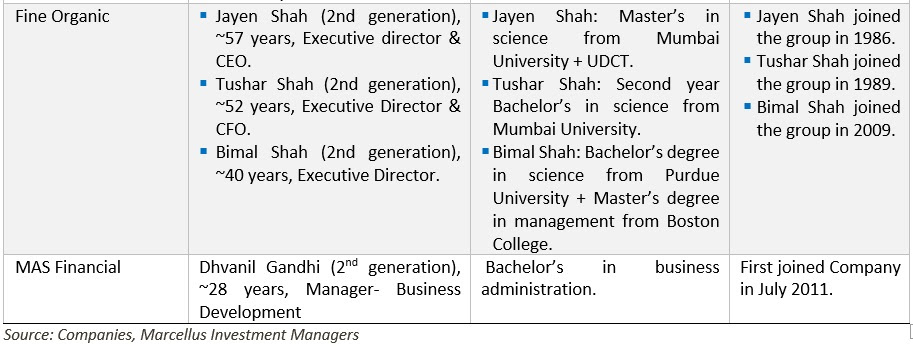

Quite impressively, Little Champs portfolio companies have in the recent years, appointed professionals as the Chief Executive Officers. In addition, in these firms, professionals are heading key functions like R&D, operations, sales, etc. In fact, most of these initiatives has been driven by the next generation leaders of the family. We illustrate some examples of Little Champs companies with professional CEOs in Exhibit 4.

In what is a very competitive market for top talent, we believe that the following factors have enabled Little Champs companies to attract high quality professionals into their organisations:

- Employee ownership plans: An important tool employed increasingly by Little Champs portfolio companies in the recent years is to give the non-promoter professionals a share in the ownership of the Company. This is being achieved primarily through Employees Stock Options Plan (ESOP) or Employee Stock Appreciation Rights (ESAR)- both of which are effective tools to attract and retain scarce talent & give high potential employees an opportunity to participate in the upside in company’s value generated through their skills & efforts. As of today, nearly 50% of the Little Champs portfolio companies have an employee ownership plan in place as shown in Exhibit 5.

- Long term growth career prospects: It helps that Little Champs companies are market leaders within their niche sectors. Furthermore, these companies have been at the forefront of product & process innovations, operational excellence, etc which plays an important part in attracting talent. Our interactions with these companies’ management indicate that effective communication of the company’s long term growth strategy and thereby the employees’ career advancement and a culture of empowerment are as, if not more, effective as incentivisation.

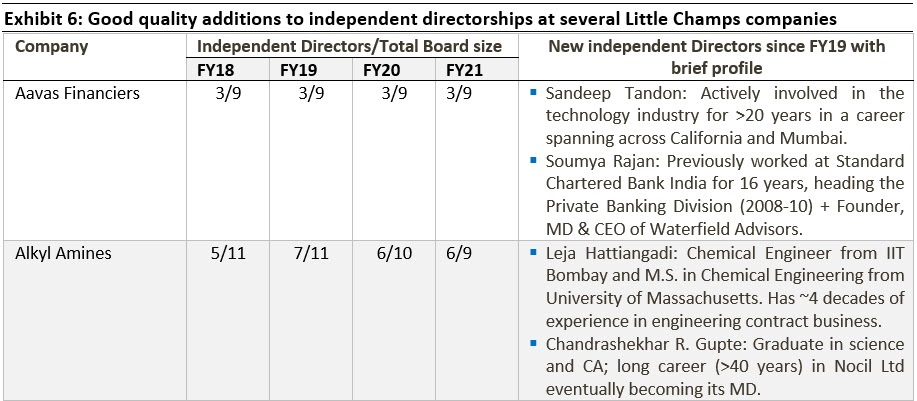

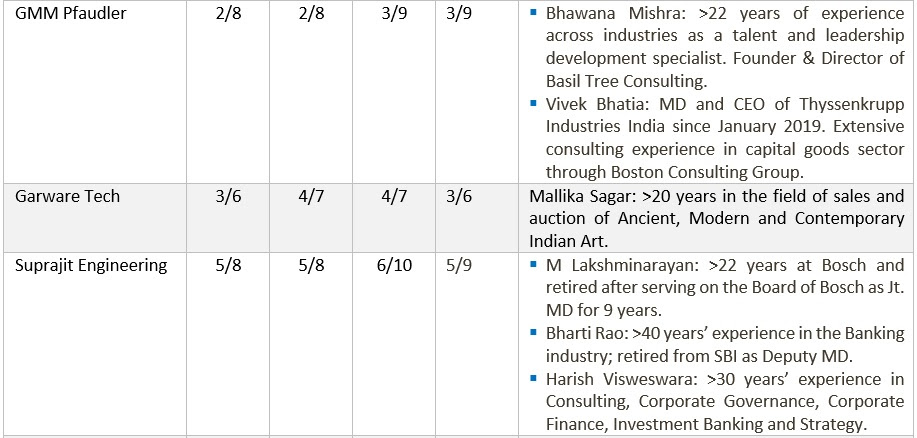

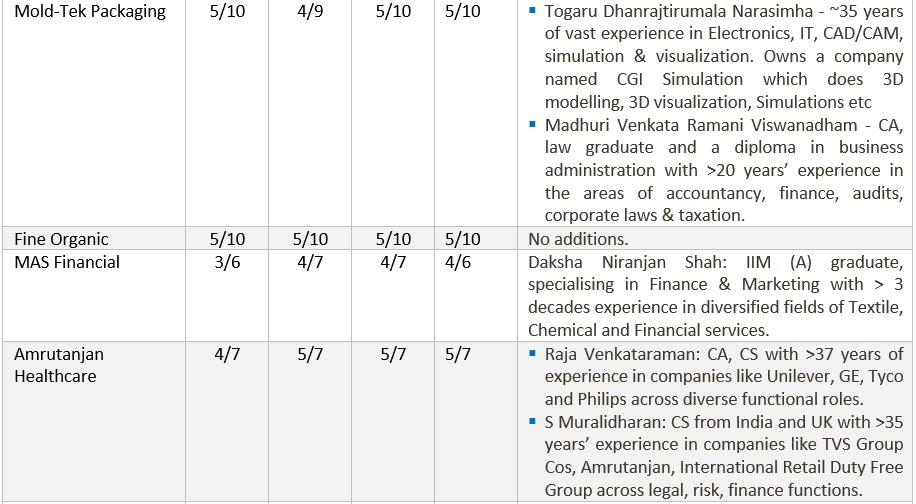

C. Significant improvement in the Independent Board quality in the recent years

Another positive development in the Little Champs portfolio companies is a significant improvement in the quality (relevance, diverse set of expertise, etc) of the independent Board Directors over the last 2-3 years. A high-quality Board plays an important role in positively influencing the key strategic including capital allocations decisions. It can in fact play a central role in guiding the succession planning exercise within the organisation.

Conclusion

Whilst all good investors focus on analyzing a listed company’s financial statements and its pre-existing moats, we believe that where great companies distinguish themselves from good companies is in their ability to build systems & process that either help them attack opportunities others cannot see or mitigate risks that others cannot comprehend. In general, our Longevity Framework helps us quantify the ability of great companies to pull away from the competition by doing things that the competition cannot replicate.

More specifically, within the Longevity Framework, “succession planning” analysis allows us to capture how the Little Champs companies have made rapid strides in recent years thanks to a well thought through succession roadmap, the proliferation of professionals in key roles, the democratization of company ownership through stock options and through high-quality independent director appointments.

|

|

Disclaimer: Copyright © 2026 Marcellus Investment Managers Pvt Ltd, All rights reserved

Note: the above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer or an employee.

This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.

Regards, Team Marcellus

If you want to read our other published material, please visit https://marcellus.in/pms-investment-blog/

Copyright © 2026 Marcellus Investment Managers Pvt Ltd, All rights reserved