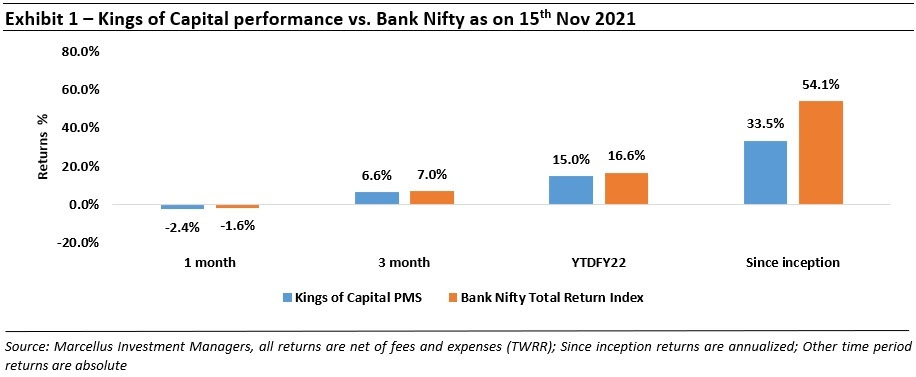

Since its inception about fifteen months ago, the Kings of Capital Portfolio (KCP) has delivered annualized returns of 34% vs. 54% for the Bank Nifty. The underperformance of the KCP portfolio is a factor of: (i) fund composition vs. that of the index – Bank Nifty consists of only banks vs. KCP has an allocation of only ~40% to banks; (ii) stock selection i.e. we have avoided turnaround stories; and (iii) the decade high volatility during the past year which saw a 48% drawdown for the Bank Nifty and then a recovery to the original highs all within a period of 12 months. In this newsletter we cover these three aspects and the fundamentals of the largest detractors of relative share price performance of the KCP portfolio (i.e. HDFC Bank, Kotak Bank, HDFC life and ICICI Lombard).

Performance update of the live fund

The key objective of our “Kings of Capital” strategy is to own a portfolio of 10 to 14 high quality financial companies (banks, NBFCs, life insurers, general insurers, asset managers, brokers) that have good corporate governance, prudent capital allocation skills and high barriers to entry. By owning these high-quality financial companies, we intend to benefit from the consolidation in the lending sector and the financialization of household savings over the next decade. The latest performance of our PMS is shown in the chart below.

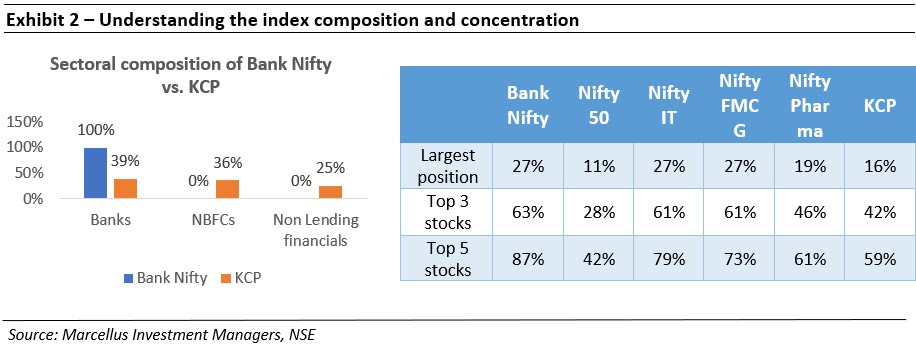

Understanding the Index vs. fund composition and concentration

- Composition: The Bank Nifty index is a sectoral index which as the name suggests consists only of banks. In contrast, in the KCP portfolio, the allocation to banks is only ~40%. As illustrated in Exhibit 2, ~60% of KCP is invested in NBFCs and non-lending financials (life insurers, general insurers, asset managers and brokers). The lenders in the KCP portfolio i.e. banks + NBFCs have delivered 55% annualized returns since inception which is similar to returns of the Bank Nifty. However, the non-lenders in KCP have delivered an annualized return of 17% leading to a lower blended return and relative underperformance vs. the Bank Nifty.

The share price returns of KCP banks, NBFCs and non-lenders since over the past year (since markets have surged) are as below:

NBFCs >> banks >> non-lending financials

On the other hand, the resilience during the Covid crisis in terms of lower share price drawdown was:

Non-lending financials >> banks >> NBFCs

- Index concentration: The Bank Nifty is a highly concentrated index not only compared to the Nifty50 but also compared to other prominent sectoral indices. HDFC Bank currently constitutes 27% of the index, the top 3 stocks i.e. HDFC Bank, ICICI Bank and SBI constitute 63% of the index and the top 5 stocks (the top 3 stocks + Kotak Mahindra Bank and Axis Bank) constitute 87% of the index. Given this level of concentration, there will be times like the past 15 months when a couple of large stocks in the index which are not a part of KCP (SBI and ICICI in this instance) do well leading to underperformance during that period.

Underperformance due to stock selection

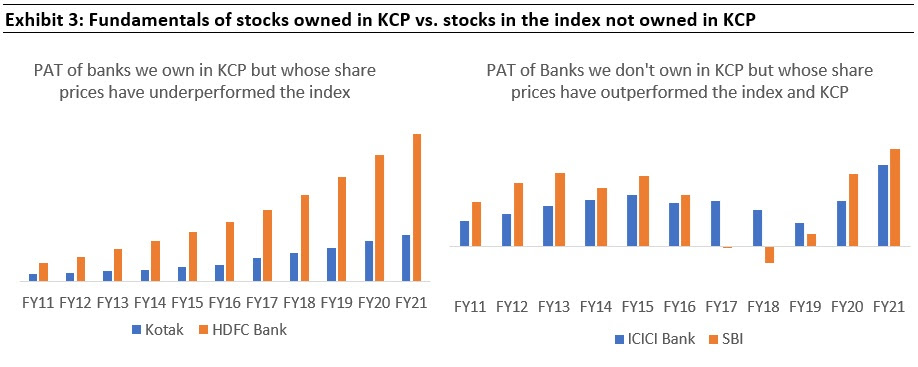

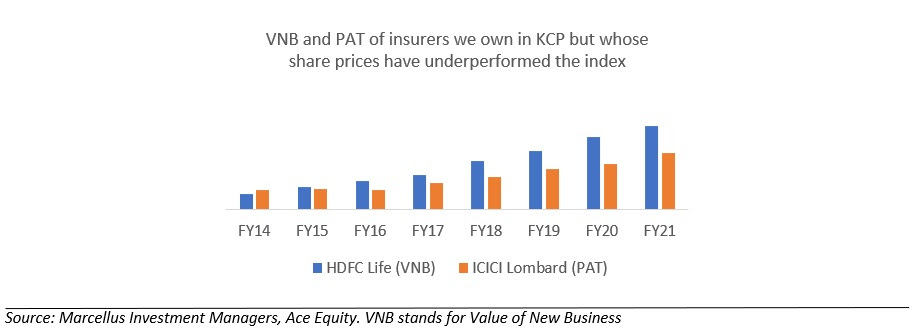

Fundamentals of the stocks which have underperformed: In Exhibit 3, we have illustrated the fundamental performance of the companies we own in KCP but whose share prices have underperformed the index over the past fifteen months. The fundamentals of the KCP portfolio companies have continued to compound consistently; however there has been no revival/ turnaround in their fortunes as seen in the fundamentals of SBI and ICICI Bank. This has led to the share prices of these stocks delivering healthy absolute returns but poor relative returns.

Drawdown of these underperforming KCP stocks during the Covid crisis: Given the healthy fundamentals of the stocks which have underperformed i.e. HDFC Bank, Kotak Bank, ICICI Lombard and HDFC Life, it does not come as a surprise that these four stocks saw the least drawdown during the Covid crisis not only compared to all the banks within Bank Nifty (including SBI and ICICI Bank) but also compared to the other 8 KCP stocks.

Will we therefore invest in turnaround stories?: As discussed in our July, 2020 newsletter (click here to read) we use our capital allocation filters to zero in on Financial Services companies which have historically demonstrated the ability to deploy capital prudently. Given our focus on a long track record of healthy fundamentals, we will miss out on some turnarounds in the Financial Services sector, but we will also have a much lower probability of losing money. Investing in turnaround stories also requires us to time the entry and exit into such stocks perfectly which we believe is extremely difficult to execute on a consistent basis. We will therefore continue to be disciplined in our approach of investing in only those companies which have historically demonstrated consistent earnings growth and have the ability to deliver sustainable, profitable growth for long periods of time.

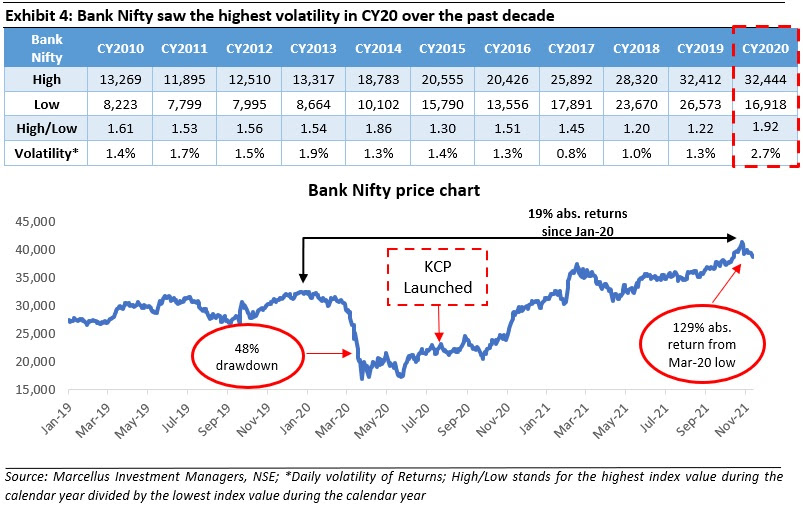

Extreme volatility during CY20 resulting in large divergence in performance based on entry point

Exhibit 4 illustrates the volatility of the Bank Nifty in 2020 – a year which saw unprecedented volatility in that index (about twice that of the volatility over the past decade). Given the excessive volatility over the past year, the short-term share price performance numbers can look distorted.

Take for instance the case of Bajaj Finance – absolute share price performance of Bajaj Finance since fund inception on 28th July, 2020 has been 134% but had the fund inception been a couple of months earlier, the share price performance would have been 289%. Similarly, for AU Small Finance Bank the absolute share price performance since inception has been 55% but had the fund inception been a month earlier, absolute share price returns of AU would have been 124%.

Investment strategy going forward

We will continue following the same strategy (as followed over the past year) to manage KCP. To be more specific we will:

- Invest in Financial Services franchises with clean accounts, a proven track record of rational capital allocation and very tangible competitive advantages.

- Allocate around 40-50% of the portfolio to non-lending stocks i.e. plays on savings since these not only provide stability to the portfolio but also allow us to tap into the financialisation of India’s savings by investing in high quality insurers, asset managers and wealth managers.

- Avoid turnaround stories in the Financial Services sector since these tend not to be sustainable generators of shareholder value.

The underlying earnings of the KCP companies have compounded by 22% over the past 5 years. We expect to see this earnings compounding sustain over the coming years. This, we believe, should provide a sound underpinning to the prospective returns of the Kings of Capital Portfolio.

|

|

|

|

|

|

Disclaimer: Copyright © 2026 Marcellus Investment Managers Pvt Ltd, All rights reserved

Note: the above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer or an employee.

This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.

Regards, Team Marcellus

If you want to read our other published material, please visit https://marcellus.in/pms-investment-blog/

Copyright © 2026 Marcellus Investment Managers Pvt Ltd, All rights reserved