| As discussed in our Mar, 2021 newsletter on ICICI Lombard (click here to read), the unique business model of raising cash upfront (at possibly no cost) and earning income on it for extended periods of time makes a well-run general insurer an attractive business to own. In this newsletter we discuss Progressive Corp., an American auto insurer established in 1937 to understand how a leading Indian general insurer like ICICI Lombard (ILOM) may evolve over the next few years. Progressive has grown its PAT at 15% CAGR over the past twenty years (2001-2020) and has seen its RoE improve from 13% in 2001 to 37% in 2020. Progressive’s growth has come through consistent market share gains as it has been gaining market share in the American general insurance industry every year since 2008. We further highlight the similarities and differences between ICICI Lombard and Progressive in this newsletter.

“I have always thought for a very long time that Progressive has been very well run. Sometimes they copy us. Sometimes we copy them. And I think that will be true five years from now, 10 years for now. And I think they will, for a long time, be the two companies that the rest of the auto insurance industry has trouble not losing share to. The success of the auto companies getting into the insurance business is about as likely as the success of insurance companies getting into the auto business. It’s not an easy business at all. And I would bet against any company in the auto business being any kind of an unusual success. I worry much more about Progressive than all of the auto company possibilities getting into the insurance business.” – Warren Buffett during Berkshire Hathaway’s Annual Meeting in May 2019

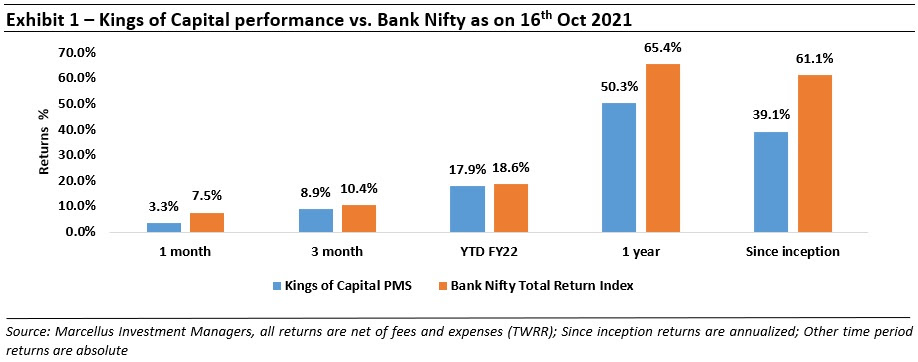

Performance update of the live fund

The key objective of our “Kings of Capital” strategy is to own a portfolio of 10 to 14 high quality financial companies (banks, NBFCs, life insurers, general insurers, asset managers, brokers) that have good corporate governance, prudent capital allocation skills and high barriers to entry. By owning these high-quality financial companies, we intend to benefit from the consolidation in the lending sector and the financialization of household savings over the next decade. The latest performance of our PMS is shown in the chart below.

American auto insurance industry

The American automobile industry was at a nascent stage in the 1890s and one of the first unforeseen realities of owning a car was automobile owners’ operating errors i.e. car accidents. This prompted Travelers Insurance Company to issue the first automobile insurance cover in 1898. According to the Company, this policy was a $5,000 liability coverage for a premium of $12.25. In 1925, Massachusetts became the first state to make auto insurance compulsory. This legislation was followed up by other American states over time and it was during this period that the four largest American auto insurers were incorporated – Allstate (1930), GEICO (1936), Progressive (1937) and State Farm (1942).

Progressive’ history

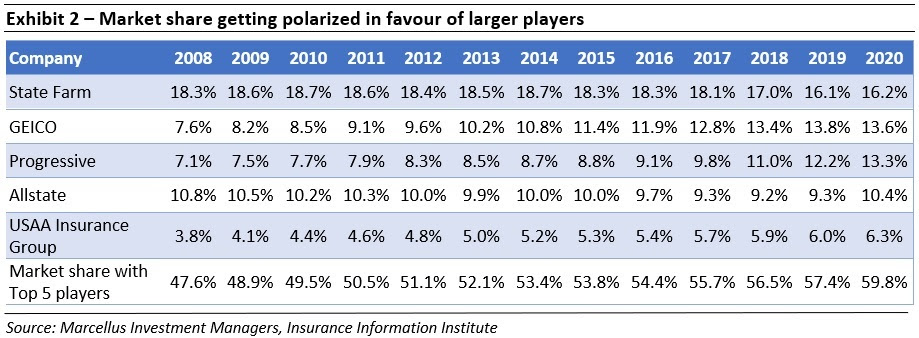

In early 1937, Joseph Lewis and Jack Green founded the Progressive Mutual Insurance Company in Cleveland, Ohio. Their stated desire was to approach auto insurance in an innovative way – like no other company had, hence the name Progressive. Following the death of Joseph Lewis in 1955, Jack Green became Progressive’s CEO and Joseph’s son Peter Lewis joined the company as an underwriter and went on to become the CEO ten years later in 1965. Peter Lewis who remained CEO for 35 years (1965-2000) had a simple financial dictum: prioritize underwriting profitability over volume growth. Under Peter Lewis, Progressive took several steps which were radically different from how the industry was operating – (i) focus on high-risk drivers which were rejected by other auto insurers; (ii) it became the first company to publish loss reserves in 1977; and (iii) when the internet was just gaining popularity, Progressive stepped ahead of the competition and became the first major auto insurer in the world to launch a website. Since Lewis stepped down as CEO in 2000, the Company has had only two other CEOs – Glenn Renwick (2000-2016) and the current CEO Tricia Griffith. Exhibit 2 below shows the significant and consistent market share growth of the three direct auto-insurers (Progressive, GEICO and USAA).

Progressive’s competitive advantage

A. High quality underwriting– Warren Buffett has noted Progressive’s “very sophisticated way of pricing business.” Given Progressive had the first mover advantage of insuring higher-risk drivers, the company has amassed a large amount of data on various driver profiles that sits at the core of its policy pricing formulae. Some of the initiatives taken by Progressive to improve its policy pricing algorithms and related pricing skill sets are:

- In 2004, the Company introduced TripSense, a usage-based insurance program to research the driving habits of consumers.

- In 2008, the data from TripSense was used to introduce MyRate, an innovative way to price car insurance which allowed dynamic pricing of insurance based on how customers actually drive.

- MyRate was rebranded in 2011 as Snapshot. Snapshot collects driving information during the first policy term and the customer will see a new personalized rate when the policy renews. Driver information includes the time of day a person drives, sudden changes in speed (hard braking and rapid accelerations), the amount driven, and, for customers using the mobile app in some states, how the drivers use the mobile phone while driving. As a result, customers with safe driving behaviour were rewarded with lower rates while high risk drivers were penalized.

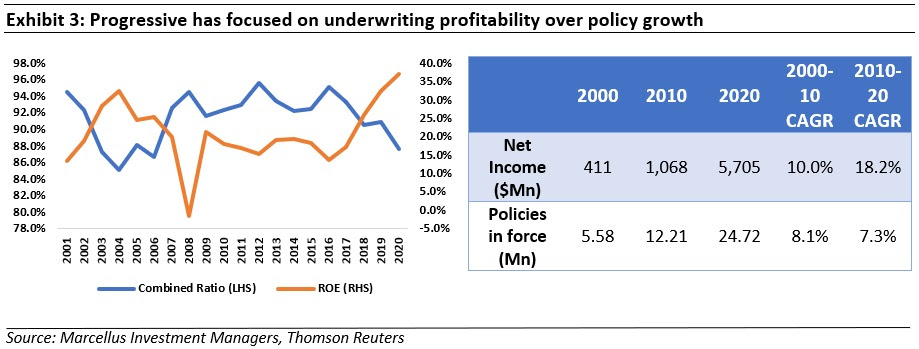

Such initiatives helped the company to drive premiums, which doubled during 2015 to 2020 with steady decline in combined ratio.

B. DNA of choosing profitability and ROE over growth in premium income– Peter Lewis’ simple financial dictum still serves the Company today: underwriting profitability over policy growth. For instance, during 2002, the Company decided to wind-down lender’s collateral protection program as they lost some key accounts for the lender’s collateral protection products and determined that this business was unable to meet its profitability target. Progressive’s underwriting margins have been the best in the industry since a long period of time and as seen in Exhibit 3, its earnings growth has remained higher than the number of policies issued over the past two decades. While the past few years have been exceptional for Progressive with returns on equity ranging from 25% to 32% which is remarkable for an American financial services company given that 10-year treasury bills trade at 1.5%.

C. Focus on the customer– Progressive’s product as well as marketing initiatives have been customer centric, and it has not shied away from disrupting its own business model – one such initiative was to launch an auto insurance rate comparison service as early as 1994 which enabled consumers to receive a Progressive quote and comparison rates for up to three competitors. Other such initiatives include:

- It was the first auto insurer to allow customers to pay their premiums in installments which was an attractive option for those who couldn’t afford annual payments.

- Being the first in the industry (1994) to launch a specially marked and outfitted vehicle that brought trained claims professionals to wherever customers needed them— even to the scene of an accident.

- Launch of an online scrolling rate ticker in 1995 which displayed actual Progressive Direct auto insurance rates side-by-side with those of other top auto insurers.

- GEICO and Progressive popularized creative marketing for auto insurance. One can hardly watch any network or cable-based television programming (particularly live sporting events) without being flooded by comedic car insurance ads. Progressive’s Flo made its debut in 2008. (Flo is a fictional salesperson character appearing in more than 100 advertisements for Progressive Insurance since 2008). The impetus behind all the major auto insurance companies getting on board with massive advertising campaigns was to directly market to consumers rather than through commission-based insurance agents. GEICO and Progressive were able to figure out that the returns on such upfront marketing spend can be 30% if you can retain such customers for a long period of time.

- Progressive has also been successful in bundling its policies across their product set, particularly after the company acquired part of American Strategic Insurance in 2015, thereby allowing independent agents the ability to offer a competitive auto and home insurance bundled offering.

Progressive’s Competitive advantages and smart capital allocation resulted in value creation for Progressive shareholders

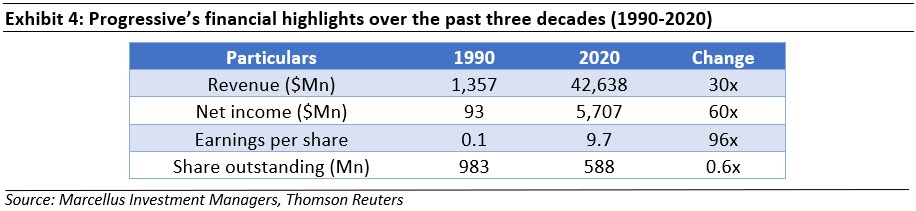

Unlike most financial services businesses which need frequent infusions of capital to grow earnings, during the past 30 years, Progressive has not raised any capital; instead it has paid dividends and regularly repurchased shares. Between long periods of inactivity, it made the occasional large acquisition (in 2014 they acquired stake in ARX Holding Corp., the parent company of American Strategic Insurance for $875Mn). Progressive’s earnings per share (EPS) grew by 96 times over the last three decades and the number of shares outstanding have reduced by 40% due to share buybacks, resulting in significant value creation for shareholders. Since 1971, Progressive has spent $9.1 billion repurchasing their shares, at an average cost of $7.5 per share (its current market price is $91).

Similarities and dissimilarities between the well run Indian and American general insurers:

(i) Focus on profitable growth has been the bedrock for Progressive and ILOM: Progressive has not shied away from winding down segments if they were unable to meet the profitability targets (refer point (ii) under competitive advantages). Likewise, ILOM has made a conscious choice of staying away from segments which are likely to see high loss ratios and aggressively growing in segments where loss ratios are likely to be lower. For example, in the past two years it has aggressively grown in the fire insurance segment while it has completely exited the crop insurance business even though it used to form 17% of the product portfolio in FY19. Progressive in America and ILOM in India differentiate themselves from other Insurers on their ability to raise low cost of liabilities by sound underwriting practices. Because they are able to raise float at low cost, they can consistently earn a post-tax return on equity of 20%.

(ii) ILOM has a better ability to change business mix: A significant difference between the two high quality insurers is the business segments that they operate in. Progressive has largely focused on auto insurance (makes up ~80% of Progressive’s business) whereas ILOM has been able to setup deep distribution networks across all major segments of general insurance. ILOM has consistently been the leading player across all major segments (Fire, Health, Motor) which enables it to change its business mix depending on regulations, competitive intensity and expected loss ratios. ILOM therefore has a larger market to operate in and options to diversify away from products which might not be RoE accretive.

(iii) Presence of state-owned players in India is unlike the US: Unlike the US, government owned general insurers still have 36% market share in India – the four public sector general insurers have an average solvency ratio of 144% vs. the regulatory minimum of 150%. Additionally, the combined ratio of these public players has been above 100% since a long period of time. Unless the Government of India consistently keeps pumping significant amounts of capital in these public sector players, private general insurers are likely to see market share gains for a long period of time.

(iv) ILOM has not yet aggressively explored the route of selling directly to consumers: While Progressive and GEICO have greatly benefitted from selling auto insurance to customers directly, ILOM has not yet aggressively built a direct sales engine. The advantages of building a direct sales channel include personalized customer data, better policy pricing, improved profitability margins and an improved ability to cross sell other products. However, Indian auto insurance regulations and customer behaviour will determine when the shift to direct selling of insurance will gain scale.

|

|

|