OVERVIEW

POPULAR ARTICLES

Across the world, technology is steadily reducing the relevance of ‘The Office’ for white collar workers. As demand for office space in big cities reduces and as work shifts in two directions: a) to ‘Work From Home’; and b) to white collar gig work, demand for residential and commercial space in Tier 2 cities will grow. This will have big implications for the real estate investments of Marcellus’ clients. Secondly, the altered nature of work will compel white collar workers to save more and inject more structure & planning into their financial savings. That is where Marcellus’ free financial planning service comes into play.

“The office is dead. It’s not dying or on life support, it’s just dead….When teams became spread across the country, the purpose of the office died and it accelerated a shift that was bound to happen anyways.” — Jeffrey Smith, a tech professional (1)

The office is only 300 years old

Modern humans have existed for approximately 300,000 years. The office, in its current form, is only around 300 years old i.e. for 99.9% of human history, we have not had to ‘go to office’ to earn a living. In fact, the first purpose-built office building in the world was inaugurated in London in 1726. Named the Old Admiralty (now the Ripley Building – see exhibit below), it was built for the Royal Navy and was the world’s first dedicated office.

Now, however, a confluence of factors are resulting in the demand for office space reducing globally. Globally, office attendance has stabilized at ~30% below pre-pandemic levels, leading companies to downsize their footprints. (3)

As demand for offices reduces further in the years to come due to the factors discussed below, it will have a significant impact on the economy and on your investments.

Challenge #1 for the office: Tech advancements take away a part of the ‘use case’

Part of the reason people go to office is that expensive equipment, which only the employer can afford to purchase, is kept there. For example, in the late 1960s, buying a photocopier was a massive capital investment (so much so that the cost of a simple copy was $0.25).

While exact “inflation-adjusted” figures are difficult, a basic, entry-level, personal-use copier today costs roughly 5%–10% of what a high-end, dedicated photocopier cost in the 1970s in real terms, and provides far superior functionality. (4)

As the cost of office equipment has crashed, many employees can now afford to have similar (if not exactly the same) equipment at home thus removing the need to go to the office to access the photocopier or the computer or fax machine.

Furthermore, instead of 2D video calls, virtual reality VR allows employees to meet in 3D virtual offices (5) . VR is reducing the need to go to the office by enabling more immersive remote work, enhanced virtual collaboration, and efficient training, with 70% of IT companies in some regions like Bengaluru projected to adopt virtual office solutions by 2026. By 2026, VR has evolved from a novelty into a practical tool, with over 53% of companies worldwide using it for employee training and 77% planning to increase investment. (6)

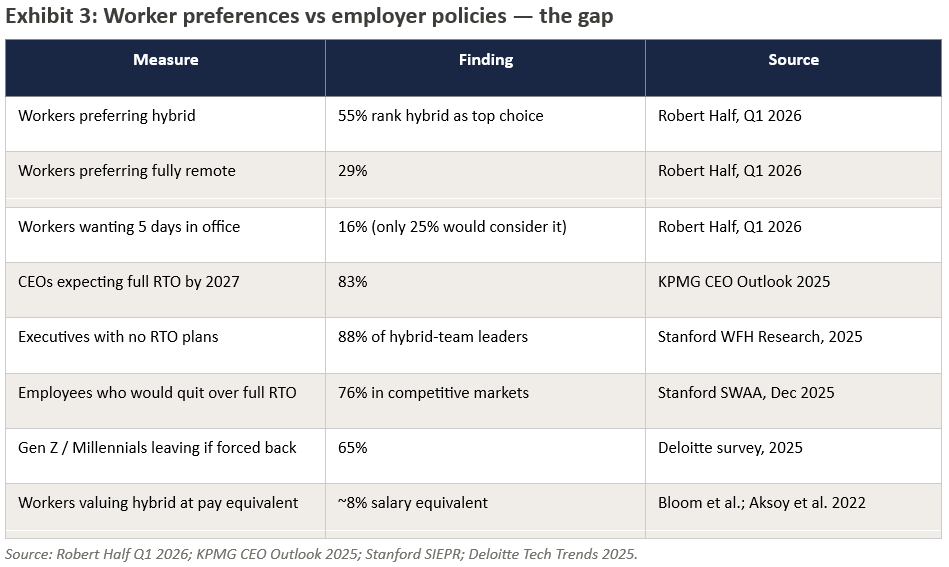

Challenge #2 for the office: Flexible work hours is working well for knowledge workers

Remote work did not begin with COVID-19 — but the pandemic forced a global experiment that no corporation would have voluntarily designed. The results are now well-documented across multiple independent research programmes. To be specific the average college educated office worker works from home 1.3 days / week and evidence strongly suggests 2–3 office days per week as the productivity and retention optimum. (7)

Hybrid work models are decreasing the total amount of space companies require, with a forecasted 8.7% decline in office demand in major global office markets (G5) by 2030. (8)

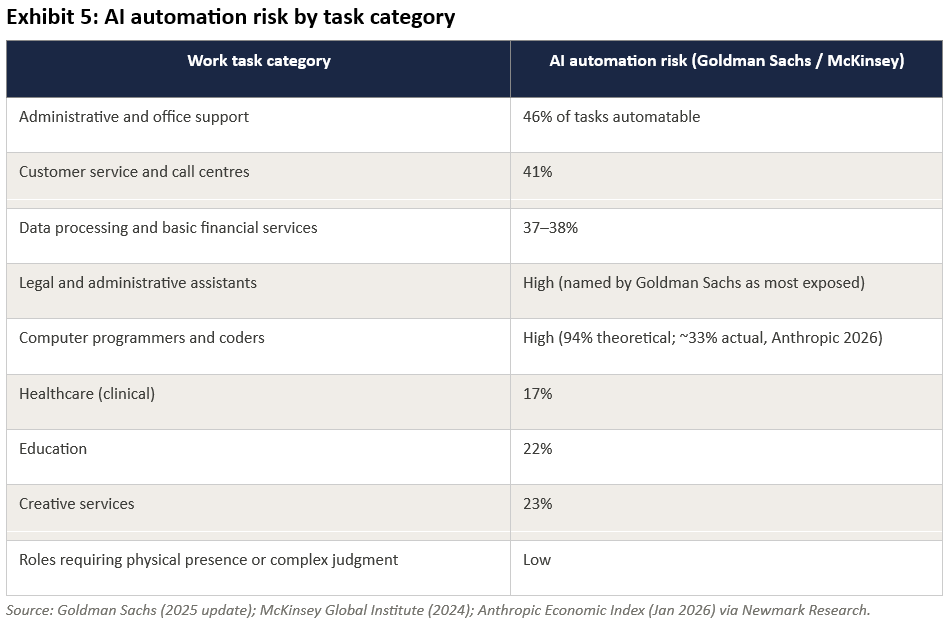

Challenge #3 for the office: Routine, cognitive office jobs are being AI-ed out

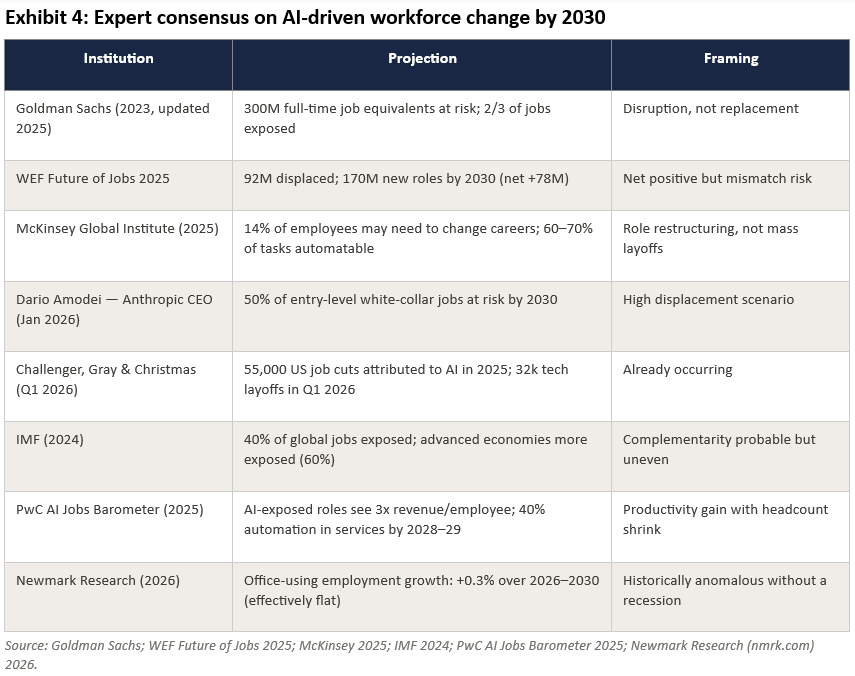

In our bestselling book, “Breakpoint: The Crisis of the Middle Class & The Future of Work”, we have discussed in detail how hiring of white-collar workers has reached a standstill in India over the past 3 years as AI begins to automate a range of tasks.

Every previous technological shift that threatened the office ultimately reinforced it, because the tools changed while the underlying logic did not. AI is structurally different: it targets the core cognitive activities of office work itself — drafting, analysing, summarising, coding, processing — rather than physical or peripheral tasks.

A 2025 study cited in the PricewaterhouseCoopers (PwC) report shows entry-level employment in AI-exposed occupations has fallen 13 per cent, while experienced roles are stable. That matters because entry-level hiring is what fills office seats. One quote from the PwC study stands out: “AI is a solid replacement for a junior analyst.” That is where the office impact begins. (9)

Increased AI automation, particularly in the IT sector, is limiting hiring and lowering the need for large, traditional offices. “Fresh graduates and junior analysts are the biggest users of office desks. When those roles shrink, the need for large, dense office floors reduces.” (10)

Investment implications

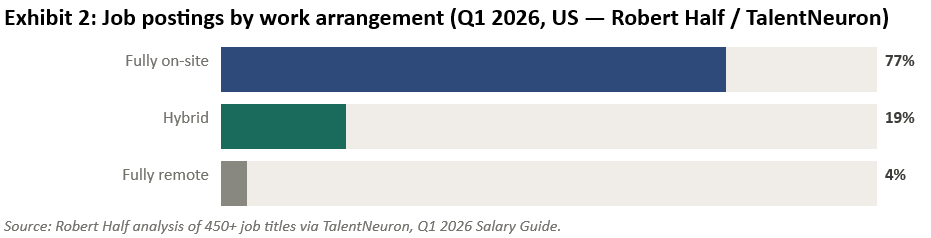

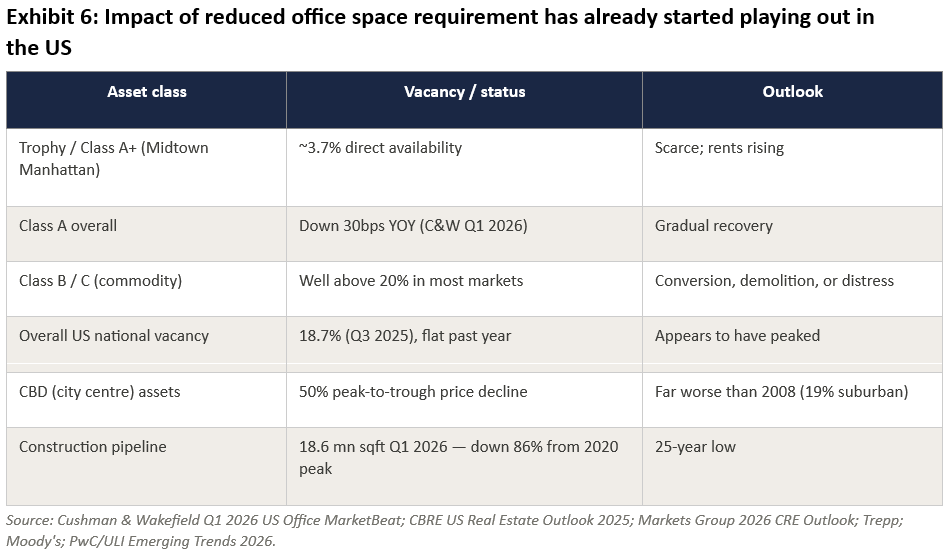

Substantial reduction in office use by 2040: Britain’s Industrial Revolution (c.1760–1840) created clerical work as a mass profession. Factories needed workers to track orders, manage payroll, write contracts and handle insurance. The office became the administrative shadow of the factory floor. That is how 300 years ago the office was born. Now, however, as AI increasingly takes over routine cognitive tasks, time tracking orders, managing payroll, writing contracts, etc it makes logical sense to believe that demand for office space will gradually reduce. You can see the impact of reduced office space requirements in the AI capital of the world – the USA (see exhibit below).

Real estate price appreciation in smaller towns and suburbs: “AI-Led distributed teams are also changing where offices are taken. Vijay Raundal, Managing Director at Teerth Realties, says companies are looking at cities where rentals and operating costs are 30-50 per cent lower than Tier-1 hubs.” Cities like Indore, Coimbatore, Jaipur and Lucknow are emerging as serious office markets. Digital infrastructure and remote collaboration tools make this possible. (11)

As people move out of overcrowded, expensive megacities and move into Tier 2 cities, you would expect residential real estate prices to also be impacted by this shift. So, if jobs are reducing in Hyderabad and increasing in Coimbatore – which is what we are seeing in our travels – that is likely to impact these residential real estate markets.

Significant reduction in demand for cars and for fuel: Nearly half of the world’s oil is used by road vehicles for transportation. (12)

If you assume that half of this oil is used for commuting to & from the office, then nearly a quarter of the world’s oil is being consumed for commuting to the office. The steady shift to working from home for part of the week could therefore reduce the world’s oil consumption by 10%.

While in countries in like America, most people have no choice but to drive to work (as public transport networks are patchy in America outside the 5 largest cities), in Europe and Asia, a shift to working from home for a part of the week is bound to reduce the need for workers to own cars (especially given how easy-to-use and how dense ride-share networks are across Europe and Asia).

More time & demand for sports, fitness, holidaying & entertainment: In many countries, but especially so in India, the commute to work eats up at least 10 hours per week of office workers’ time. A shift to working from home for a part of the week, will allow workers to use that time for sports, fitness, leisure and entertainment. Expect demand for gyms, for stadiums and restaurants especially in suburban and Tier 2 locations to rise.

Millions of AI related gig jobs in India: “According to Infosys, generative AI might displace 92 million jobs such as front-end developers and testers, but it will create some 170 million new jobs for data annotators, AI engineers and AI leads.” (13)

As repetitive cognitive office tasks are AI-ed out, a large part – perhaps as much as 50% of the workforce – will move to AI-related gig jobs. These freelancers will almost certainly work-from-home (or from a WeWork-type set-up near their residence).

Intermediating between these freelancers on the one hand and enterprise users of AI on the other will be network providers who will basically provide a Uber-type of service for the AI-world. So, a small restaurant chain in Tanzania will be able to get its CRM-bot trained by an AI-worker sitting in her living room in Coimbatore.

Greater need to save more and to plan financial goals: However, this type of work will also create the need for workers to:

- Save more money to buffer themselves from lean periods (which are all but inevitable in most forms of freelance work)

- Pay for their own medical insurance and life insurance (benefits that are currently offered by many employers in India)

- Inject structure & planning into their financial lives (a service that employers effectively provide to white collar workers by giving them structured career development).

This is why Marcellus has created over the past couple of years, a free goal planning and asset allocation service wherein anyone can reach out to us and get a detailed 4-page allocation report free of charge.

If you would like to to avail of this free service (with no-strings attached) then either scan the QR code below OR visit plan.marcellus.in

Note: This tool provides guidance on asset allocation and does not constitute a financial plan or investment advice.

Sources:

[1] https://medium.com/@jefferysmith/the-office-is-dead-long-live-the-office-6eb370209b39

[2] https://c8.alamy.com/comp/3DW34XB/the-ripley-building-old-admiralty-building-1726-by-architect-thomas-ripley-with-entrance-screen-added-by-robert-adam-in-1788-whitehall-london-uk-3DW34XB.jpg

[3] https://www.forbes.com/sites/jenamcgregor/2023/07/12/demand-for-office-space-could-fall-13-by-2030-and-thats-not-the-severe-forecast/

[4] https://en.wikipedia.org/wiki/Photocopier

[5] https://www.red-thread.com/blog/5-ways-virtual-reality-will-change-the-workplace/

[6] https://www.linkedin.com/pulse/70-bangalore-companies-use-virtual-offices-2026-market-kulkeet-singh-1ja0c

[7] Stanford WFH Research Group / Survey of Working Arrangements and Attitudes (SWAA), December 2025. Stanford SIEPR policy briefs (siepr.stanford.edu)

[8] https://www.mckinsey.com/mgi/our-research/empty-spaces-and-hybrid-places

[9] https://www.ndtv.com/business-news/ai-impact-on-real-estate-automation-hybrid-work-cutting-demand-for-office-spaces-11434993

[10] https://www.ndtv.com/business-news/ai-impact-on-real-estate-automation-hybrid-work-cutting-demand-for-office-spaces-11434993

[11] https://www.ndtv.com/business-news/ai-impact-on-real-estate-automation-hybrid-work-cutting-demand-for-office-spaces-11434993

[12] https://www.ebsco.com/research-starters/power-and-energy/energy-use-transportation

[13] https://www.bbc.com/news/articles/c5yrq1090p8o

Disclaimer:

Disclaimer:

The above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. All recipients of this material must before dealing and or transacting in any of the products and services referred to in this material must make their own investigation, seek appropriate professional advice. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer, or an employee. This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.