OVERVIEW

POPULAR ARTICLES

Summary: Across the world, retirement planning is viewed as one of the most complex problems in Finance due to the multitude of unpredictable variables at play. In India, this problem is made more complex by the high and variable inflation in the cost of living. The problem is made even more challenging for the Indian middle class due to the compression in their real incomes over the past decade. If there is ONE BIG ISSUE in Finance that middle class Indians needs to understand carefully it is not stockmarket returns, not the Iran War, not the IPL; it is retirement planning. At Marcellus, we have sought to address this challenge in two ways, through a no strings attached detailed and personalised financial education, and through a low-cost goal ‑planning support service. [Note: This tool provides guidance on asset allocation and does not constitute a financial plan or investment advice or a recommendation to invest in any securities or PMS strategy.]

Nobel Laureate Bill Sharpe’s photo sourced from Barrons

“Retirement planning is the nastiest, hardest problem in Finance.” – Bill Sharpe

Regardless of where you live in the world, if you are a person of modest means then retirement planning is by far the hardest AND most important financial challenge facing you. As Nobel Laureate Bill Sharpe has helped the rest of us understand, there are 2 critical variables which are unpredictable and which could impact your retirement years very significantly-

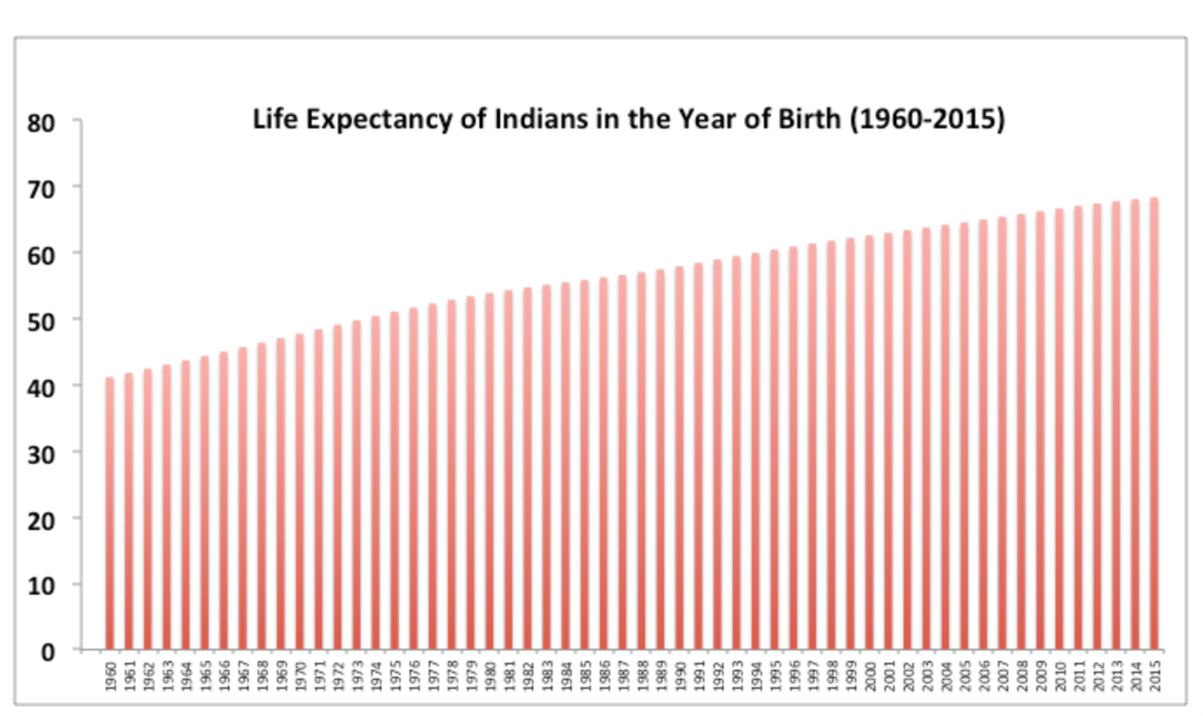

Longevity Risk: None of us know how far we will live. What we do know is that with each passing year, improvements in medical science are likely to increase our lifespan thus increasing our cost of retirement. Even if we assume that most of us will die between the ages of 70-100, there are at least 30 possible outcomes with regards to our own longevity.

Source: World Bank

However, for retirement planning purposes, we also have to factor in our spouse’s longevity – after all, after I am gone, my better half’s lifestyle still needs to be funded properly. Since, even for your spouse there are 30 possible longevity outcomes, for a couple there are at least 900 possible longevity outcomes.

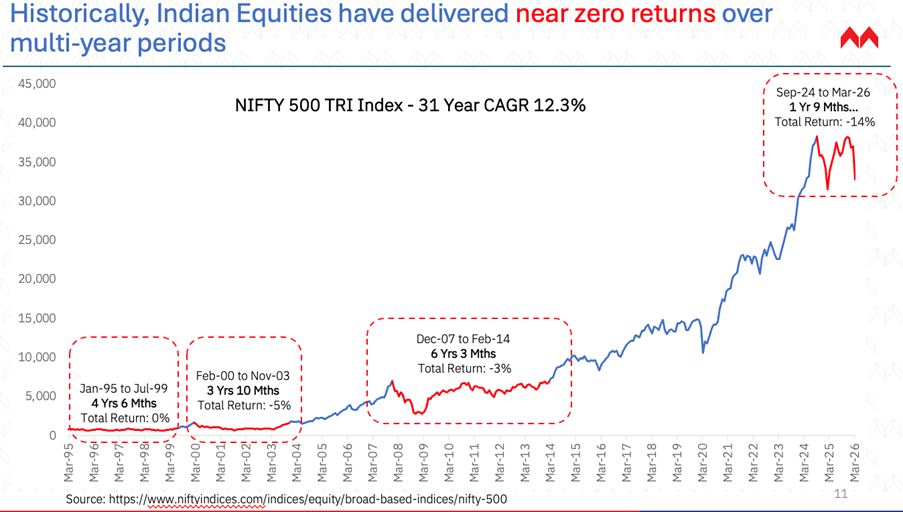

Investment Risk: Assuming that most retirement portfolios are a mixture of bonds & equities, the blended return of the portfolio through the retirement years and in the decade immediately preceding retirement could range anywhere from low-single digits to low-20s. Why? Because the world’s large stock markets have seen extended periods of ZERO returns. For example, from1967-84, the S&P500 gave zero returns. Between 1993-2003, the Sensex gave no returns. Then, again, from Jan 2007-Jan 2014, the Sensex gave close to zero returns. In fact, for half the years in the past 3 decades, the Sensex has given annual returns which are close to zero – see chart below.

Source: Marcellus Investment Managers

Assuming however, that a mixture of bonds and equities, gives a retirement portfolio long term returns anywhere between 5% and 25% and taking intervals of 0.20%, there are at least 1000 different return possibilities to consider for your retirement portfolio.

Now, given that there are 900 possible longevity outcomes (30 for you & 30 for your spouse) and there are 1000 possible returns outcomes, there are at least 90,000 possible retirement outcomes for you to consider even before we add the next important layer to this problem.

What we shared so far, is Bill Sharpe’s characterisation of the retirement planning problem. The Nobel Laureate’s mental model was built with developed economies in mind. For a developing economy like India, there are 2 other dimensions to this problem-

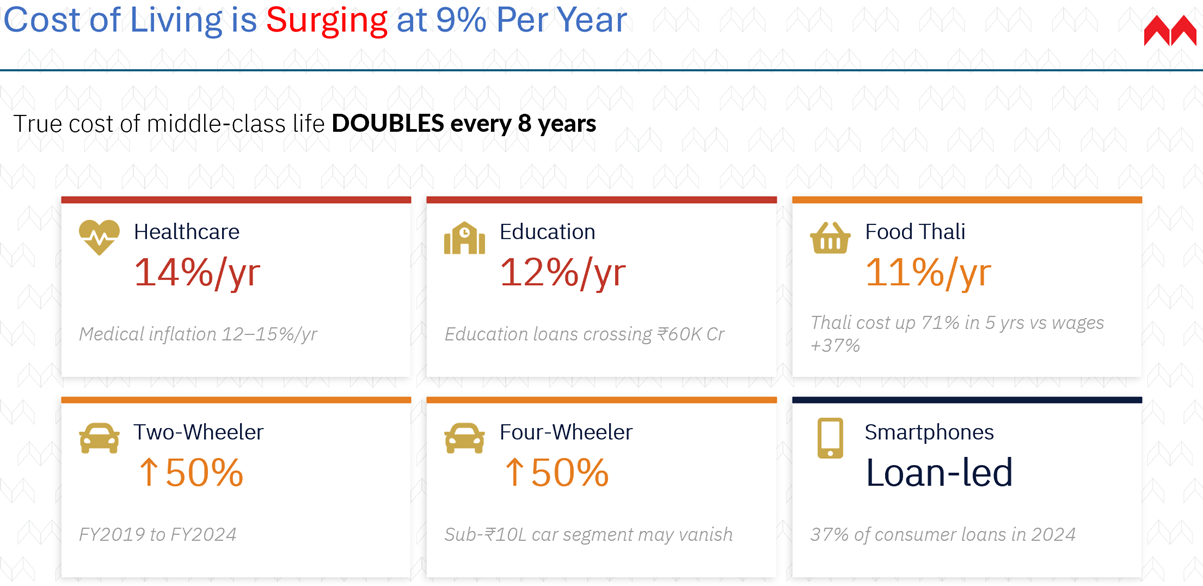

Inflation Risk: Unlike in developed markets, in developing economy like India, cost of living inflation tends to be high and variable. Over the past generation, CPI inflation in India has ranged between 0.5% at the low end to as high as 12% at the high end. Furthermore, cost of living inflation in India seems to take-off abruptly and dramatically thus reducing the practical value of strong investment returns. After all, there is no point celebrating 20% p.a. returns on your investment portfolio if your cost of living itself is rising at close to 10% as has been the case in the post-Covid era.

Source: ‘Breakpoint: The Crisis of the Middle Class & The Future of Work’ by Saurabh Mukherjea, Nandita Rajhansa & Sapana Bhavsar, Juggernaut, 2026

Within the cost of living, a specific component which is of particular interest to retirees is the cost of medical treatment. This too is ramping in India at a high rate – see article below.

Source: Business Standard

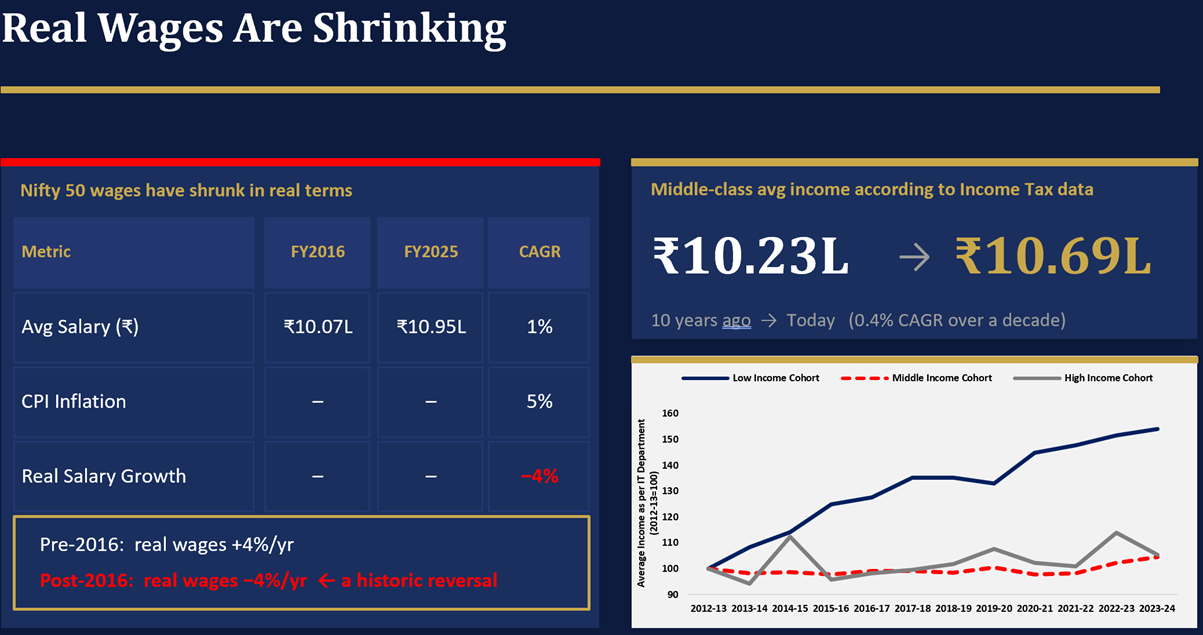

Wage compression for the Indian middle class: In most economies, retirement planning is not a problem for the rich (as they have abundant income and lots of well-paid advisors). In most countries, for the poor, the government has some sort of social security program in place. It is the middle class, who find retirement planning to be a really tricky problem to solve, both, because their means are modest and because getting good advice on this tricky subject is difficult.

The nature of this problem is made more serious by the compression we are seeing in Indian middle-class incomes. As articulated in our bestselling book, ‘Breakpoint: The Crisis of the Middle Class & The Future of Work’, over the past decade, both personal Income Tax returns and data from the Nifty50 companies show that Indian middle-class incomes have grown SLOWER than CPI inflation. As shown in the exhibit below, real incomes for the middle class seem to be dropping at the rate of 4% per annum thus reducing the means available to finance retirement.

Source: ‘Breakpoint: The Crisis of the Middle Class & The Future of Work’ by Saurabh Mukherjea, Nandita Rajhansa & Sapana Bhavsar, Juggernaut, 2026

Solving the trickiest problem in Finance

Over the last couple of years, as we wrote ‘Breakpoint’ and understood the scale & complexity of the Indian retirement challenge, we decided to solve this problem in two ways.

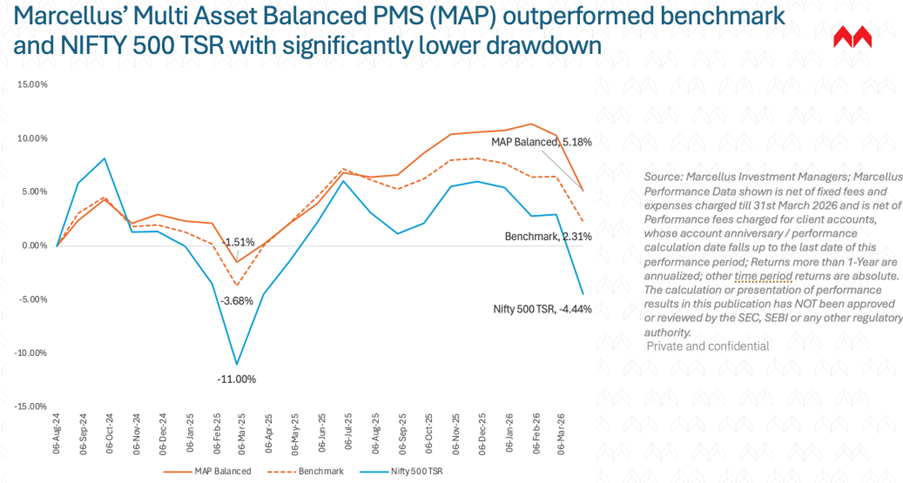

The first method was to create a Multi-Asset Product (MAP) which by diversifying across Indian Equities, Global Equities, Bonds and Precious Metals, produces smoother, more predictable returns. Our MAP PMS is available in three variants – Aggressive, Balanced and Conservative. For example, Marcellus’s ‘MAP-Balanced’ has delivered returns of 5.18% returns since inception in Aug-24 to Mar-26 while the NIFTY500 index posted a return of -4.44% over the same period – which you can see in chart below.

The second method was to create a free goal planning and asset allocation service wherein anyone (individuals who may have at least Rs 3 lakhs available for long‑term investments) could reach out to us and get a detailed 4-page financial report free of charge. If you would like to to avail of this free service (with no-strings attached and no I won’t compel you to buy my books) then either scan the QR code below OR visit plan.marcellus.in.

Thanks,

Saurabh Mukherjea

Disclaimer:

Marcellus Investment Managers; Marcellus Performance Data shown is net of fixed fees and expenses charged till 31st March 2026 and is net of Performance fees charged for client accounts, whose account anniversary / performance calculation date falls upto the last date of this performance period; Returns more than 1-Year are annualized; other time period returns are absolute. For relative performance of particular Investment Approach to other Portfolio Managers within the selected strategy, please refer to https://www.apmiindia.org/apmi/welcomeiaperformance.htm?action=PMSmenu. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the SEC, SEBI or any other regulatory authority. References to financial planning relate only to asset allocation under Marcellus’ PMS license.