OVERVIEW

POPULAR ARTICLES

On the back of the re-industrialization of the West, the global market for small industrial machines and components is growing at 5-7% per annum in $ terms. Over the past 3 years, as demand for Defence, Aerospace and Power has accelerated in Developed economies, our Global team has made several investments in European and American companies who supply industrial components and small machines.

In our 12th Feb ’26 blog Profiting from Defence & Aerospace in this Age of Rage we highlighted how the multi-trillion-dollar boom in Aerospace & Defence was leading the 10-year backlogs in the order books of European and American manufacturing giants such as GE Aerospace and Airbus.

Then in our 24th Feb ‘26 blog Profiting from the Global Upsurge in Electricity Demand we explained how surging demand for power (electricity demand growth has jumped from 2.7% p.a. before Chat GPT was launched in 2022 to 4% p.a. since then) is leading to $600 billion per annum of capex on power generation.

Industrial capex on this scale has NOT taken place in the Western world in the past half a century. In fact, in the history of mankind, China is the only country to have seen industrial capex on the colossal scale which we are currently seeing in the West. Among the multiple beneficial side-effects of this capex is a boom in demand for small industrial components (e.g. fasteners, bearings, sensors, compressors, tools, safety supplies, etc) and machines (e.g. motors, generators, hydraulics, pneumatics, drilling machines, small robots, CNC machines, etc).

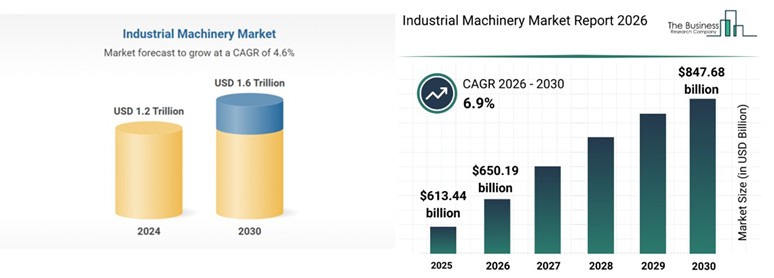

The global industrial machinery market today is sized between $0.6 – 1 trillion of sales per annum (depending on what definition of machinery one uses). More importantly, regardless of how one defines this space, this industry is growing at 5-7% per annum in $ terms (see charts above) with the fastest growth coming, interestingly, from Western Europe(iii).

5-7% p.a. industry growth suggests that well-managed manufacturers of industrial components & machinery who are seeing market share gains and efficiency improvements may have potential to sustainably grow EPS in the double digits in $ terms. With improvements in working capital cycles facilitated by AI and the Internet of Things, operating cash flow per share may also benefit even faster than EPS.

Leaving aside the boom in the end-industries (i.e. aerospace, defence, power generation) referenced above, there are three other reasons why we are seeing such robust demand growth for industrial components & small industrial machinery:

- Europe and America are suffering from acute labour shortages especially of workers who are willing and able to work in factories. As a result, across these two continents and in East Asia, we are observing a rapid move towards what is called Industry 4.0 i.e. the digitization of manufacturing and industrial processes, integrating technologies like IoT, AI, big data, and robotics. This would entail, for example, that in a power plant rather than a human being checking the pressure gauges on boilers, a sensor would do the job and feed the information it into a plant management system which using AI (rather than human operators) would recalibrate the boiler if need be.(iv)

- The move towards energy efficiency in Europe and the rise of EVs across the world is triggering greater demand for smart factory technology and demand for, small, robust, components in, electrical and electronic, systems (v). The automotive sector remains the largest consumer, particularly for, precision tools, while aerospace and, consumer goods are also fueling growth.

- With the USA and China in the early stages of what promises to be an extended period of superpower rivalry, every country now fears being held hostage to fortune by other of these two muscular nations. Thus, every large economic block – including America and Europe – is rushing to rebuild its domestic industry and manufacturing ecosystem (an ecosystem which had been ceded to China over the past 40 years). Legislation like the CHIPS Act and Inflation Reduction Act (IRA) in USA and similar initiatives by the EU is providing hundreds of billions in subsidies and tax credits , specifically boosting the production of semiconductors, EV batteries, fighter jets, drones, and clean energy components (vi).

Over the past four years, as the story of re-industrialization of the West has kicked into higher gear, Marcellus’ Global team has made several investments in companies listed in Europe and America who supply industrial components and small machines to the industrial giants of the West. Two such companies are Parker Hannifin and Addtech.

Founded in 1917 and listed on the New York Stock Exchange, Parker Hannifin is one of the largest companies in the world in motion control technologies. Uniquely the firm offers a portfolio that spans nine core motion technologies, including hydraulics, pneumatics, filtration, and aerospace. The firm dominates the $145 bn motion & control market through comprehensive, integrated solutions and high customer retention (vii). The company has had contracts to contribute parts and maintenance for machinery produced by giants like Airbus, Rolls-Royce and Commercial Aircraft Corporation of China (viii). Parker Hannifin’s primary competitive advantages lie in its unmatched global distribution network of over 17,000 partners, and superior operational execution. More than 50% of sales are derived from the higher-margin aftermarket. Over the past decade, Parker Hannifin’s share price has risen 15.5x in INR terms (Source: Bloomberg).

Listed in Sweden and heavily focused on the Nordic markets, Addtech AB traces its roots back to 1906. Addtech is a group of companies active within niche markets for high-tech products and solutions. The firm’s operations are organized in five business areas: Automation, Electrification, Energy, Industrial Solutions and Process Technology (ix). The firm’s 150 independent subsidiaries maintain their own brands and their entrepreneurial cultures. This allows for faster decision-making and deep local market proximity that larger, centralized competitors often lack. The company avoids commoditised markets, focusing instead on high-knowledge industrial niches in sectors like Automation, Electrification, and Energy. This specialization creates high barriers to entry and allows for premium, value-based pricing (x). Over the past decade, Addtech’s share price has risen 15.6x in INR terms (Source: Bloomberg).

Investment implications for you

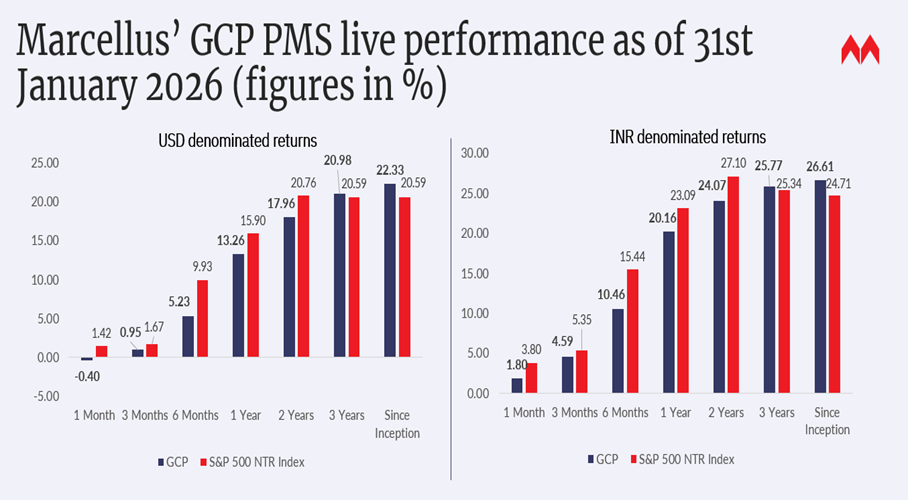

Our Global team has undertaken investments in this segment as part of its stated strategy over the past year to help our clients achieve global diversification through allocation to companies which are benefitting from this new era of high-tech industrialisation. Thanks to the regulatory reforms expedited by the Indian authorities over the past couple of years (see our 7th January ‘26 blog: Four Mega Reforms Which Opened up Global Investing for Indians ), we Indians are now able to diversify globally in a cost-efficient and tax-efficient manner and benefit from this new age of rage. Our track record in compounding across the world is shown below. Since inception in Oct 2022, the strategy has delivered at ~27% CAGR (net of all fees & expenses in INR).

If you would like more information about our global strategy, please reach out to us.

Source: Marcellus performance data is shown gross of taxes and net of fees & expenses charged till end of last month on client account. Performance fees are charged annually in December. Returns more than 1-year are annualized. Marcellus’ GCP USD returns are converted into INR using USD: INR exchange rate from RBI – Link for the reference

Note: * Since Inception performance calculated from 31st Oct 2022. The inception date is 31st Oct 2022, being the next business day after the account got funded on 28th October 2022. S&P 500 net total return is calculated by considering both capital appreciation and dividend payouts. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the IFSCA or US SEC. Performance is the combined performance of RI and NRI strategies.

Marcellus GCP PMS is offered by Marcellus Investment Managers GIFT Branch in a segregated managed accounts format.

Thanks,

Saurabh Mukherjea

Sources:

i. https://www.researchandmarkets.com/report/industrial-machinery?srsltid= AfmBOopeGwjkupbU8RnKLrMV-1mTNr2ko4cX1Sf28WI-kGq4Y0zUUoiZ

ii. https://www.thebusinessresearchcompany.com/report/industrial-machinery-global-market-report

iii. https://www.thebusinessresearchcompany.com/report/industrial-machinery-global-market-report

iv. https://www.sap.com/sea/products/scm/industry-4-0/what-is-industry-4-0.html

v. https://www.marketsandmarkets.com/Market-Reports/europe-smart-factory-market-254889723.html#:~:text=OVERVIEW&text=The%20Europe%20smart%20factory%20market,continues%20to%20drive%20market%20expansion

vi. https://www.powermation.com/blog/2026-macro-outlook-for-u-s-manufacturing-in-industrial-automation/#:~:text=Demand%20hotspots%20(2026%E2%80%932030),Energy%20&%20electrification%20equipment

vii. https://www.swotanalysis.com/parkerhannifin#:~:text=The%20Parker%20Hannifin%20SWOT%20analysis,Strengths & https://www.gurufocus.com/news/8569377/decoding-parker-hannifin-corp-ph-a-strategic-swot-insight?mobile=true#:~:text=Hannifin’s%20strategic%20position.-,Strengths,growth%20through%20complementary%20product%20offerings

viii. https://en.wikipedia.org/wiki/Parker_Hannifin

ix. https://en.wikipedia.org/wiki/Addtech

x. https://matrixbcg.com/blogs/competitors/addtech#:~:text=Addtech’s%20competitive%20edge%20is%20built,as%20a%20specialized%20technology%20partner. & https://portersfiveforce.com/blogs/competitors/addtech#:~:text=Addtech’s%20competitive%20advantages%20are%20built,in%20the%20Addtech%20market%20analysis

The stocks Parker Hannifin and Addtech AB are part of the Global Compounders Strategy managed from GIFT City by Marcellus and regulated by IFSCA. Marcellus, its employees, their relatives, and clients have an interest in these stocks.

This material is for informational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any securities. Past performance is not indicative of future results. All company references are for illustrative purposes only and do not represent recommendations. Projections are based on third‑party sources and may change. Investors should consult their financial advisor before making investment decisions.