OVERVIEW

POPULAR ARTICLES

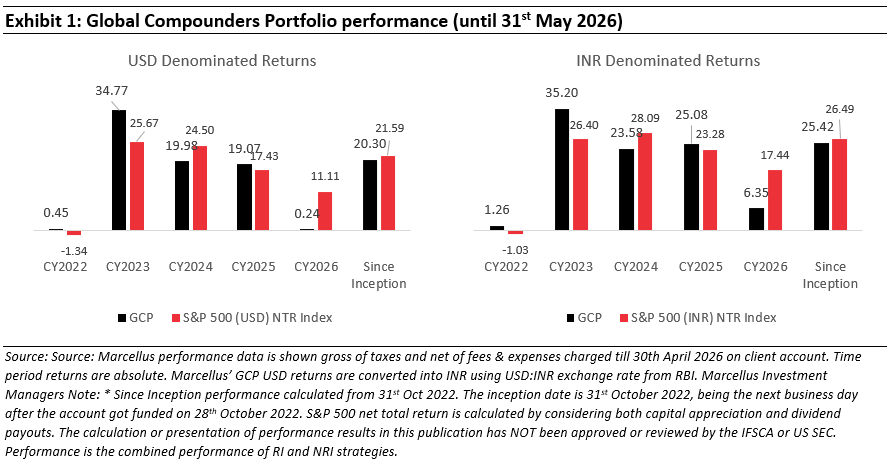

Marcellus’ Global Compounders Portfolio (GCP) strategically invests in ~40 deeply moated global companies aligned with megatrends, with an aim to provide steady earnings and shareholder wealth compounding. Over the last few years, we’ve seen the world get increasingly intoxicated with the AI narrative. While we certainly see long-term merit in this technology and what it may enable, the increasing parallels to previous periods of mania force us to remain on the sidelines. In this letter, we explore how the prevailing LLM wars have unleashed record levels of capex deployment which in turn has led to record index polarization (in favour of the LLM providers). Earnings growth expectations today surpass even the dotcom era, and valuations have unhinged completely from historical baselines. All this is happening even as claims of productivity enhancement remain debatable and initial signs of LLM commodification show up. Such periods of mania are some of the most challenging ones for active managers that focus on earnings sustainability albeit they do bring opportunities with them in ignored sectors. Our goal remains on finding such opportunities and remaining focused on businesses with durable earnings growth potential.

Unless you’ve managed to blissfully stay away from the chaos of stock markets and geopolitics, there’s a more than decent chance you’ve heard about the ‘everything is AI’ phenomenon. Loosely put, the idea says that AI is about to disrupt almost every aspect of our life – from jobs we do to the cars we drive. From the way we learn to the way we tell stories. And more. Much more.

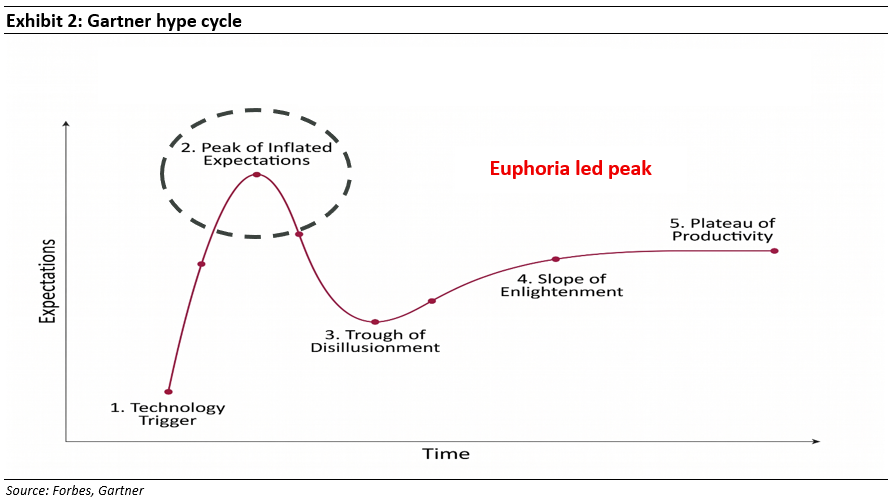

Much like any other technological change – whether it was the internet frenzy at the end of the 20th century to the more recent post Covid optimism around electrification, the initial phase of a technological change is often accompanied by much euphoria and jubilation. See the Gartner hype cycle below.

Such euphoria is based on expectations not too dissimilar to the ones we have today for AI – that it will disrupt just about every facet of life and do so very fast.

What follows inevitably is the ‘Peak of inflated expectations’.

Sir Isaac Newton famously said after losing money due to FOMO (Fear of Missing Out) during the South Sea Bubble crash of 1720: “I can calculate the motion of heavenly bodies, but not the madness of people” referring to the mad rush to buy at the very top of the bubble – something he himself succumbed to.

It’s never easy to call the exact timing in stock markets – and especially during extremes when it becomes more of a game of human behaviour and psychology and less so of business fundamentals and basic unit economics.

One can nonetheless pay heed to the signs that signal we’re at least around that zone – something we see today across equity markets.

From launch of ChatGPT to LLM wars

The launch of ChatGPT by OpenAI in November 2022 was as pivotal a moment as one can think of in the world of modern tech. The December 2022 NY Times headline captures the impact this technology had as soon as it was introduced. It was like Google search on steroids.

What followed though over the course of the next few years was something not even the inventors behind this technology perhaps would’ve foreseen.

New versions of smarter bots or Large Language Models (LLMs) as they’ve come to be known now kept rolling out, not just from OpenAI but also Google (Gemini), Meta (Llama), X (Grok) and Anthropic (Claude). Others like Microsoft and Amazon were also actively working on it.

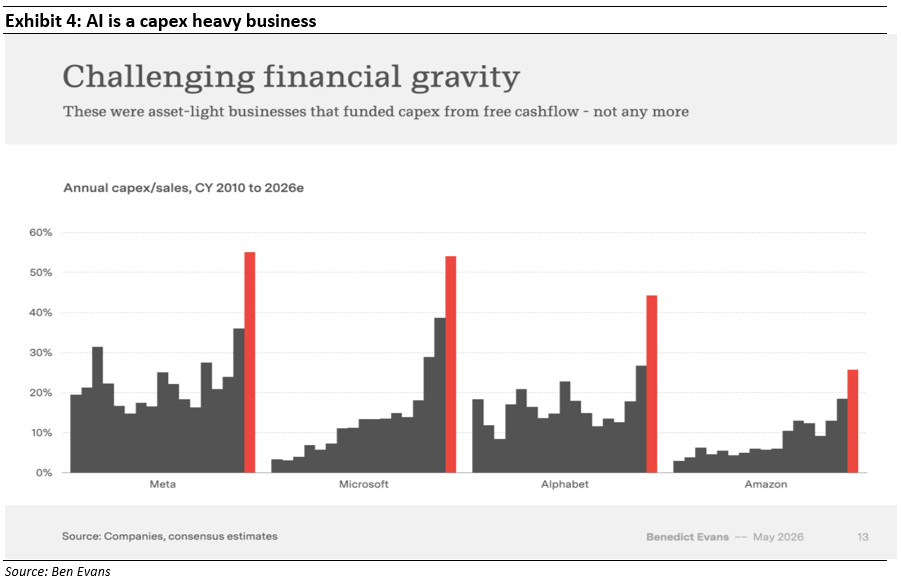

These LLMs are not just a piece of software. The ‘thinking’ or the compute that goes on behind the smartness of these models relies on huge Data Centres (DC) that deploy hundreds of thousands of Graphics Processing Units (GPUs). These GPUs are the brain and every company chases not just increasing amount of such GPUs but also the most cutting-edge versions available.

The competition for becoming the best LLM was accompanied by a surge in deployment of DCs and corresponding capex by the top technology companies.

Picks and Shovels and increasing index polarization

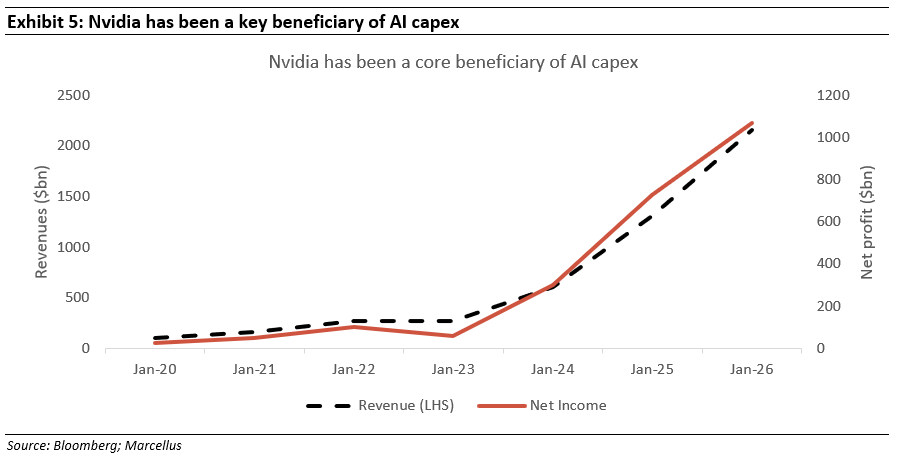

This capex has meant that the ‘picks and shovels’ or the companies supplying to satisfy this capex also surged and one company in particular was at the centre of it all – Nvidia. Its market cap grew from $570bn to $4.6tn from Jan’22 to Jan’26 as its revenues and earnings grew 8-11x over this duration. The growth in fundamentals has eventually caught up with the surge in valuation that preceded it.

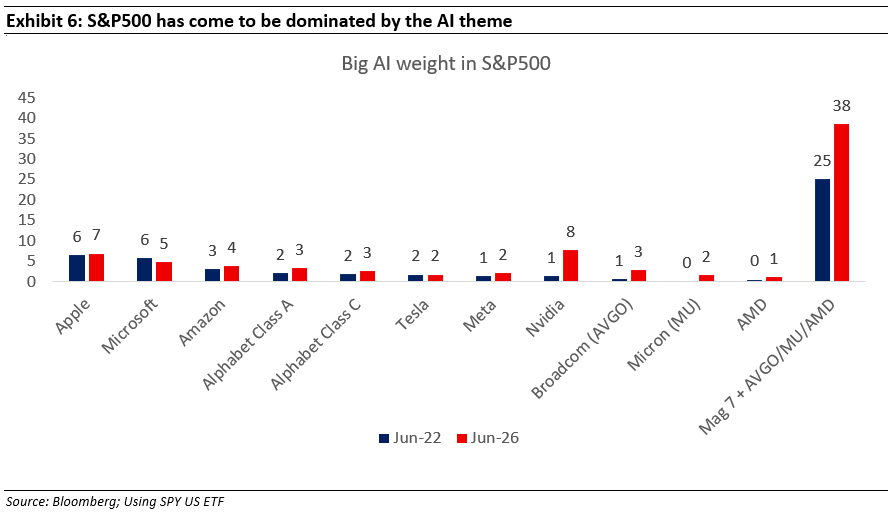

Over time, other companies in the semiconductor space such as Broadcom, AMD and Micron also saw their revenues and market cap surge. The impact is visible in the chart below that showcases how the share of Mag 7 + Broadcom/AMD/Micron surged from 25% to almost 40% over last 4 years (in S&P500).

Untethered expectations leave very little room for disappointment

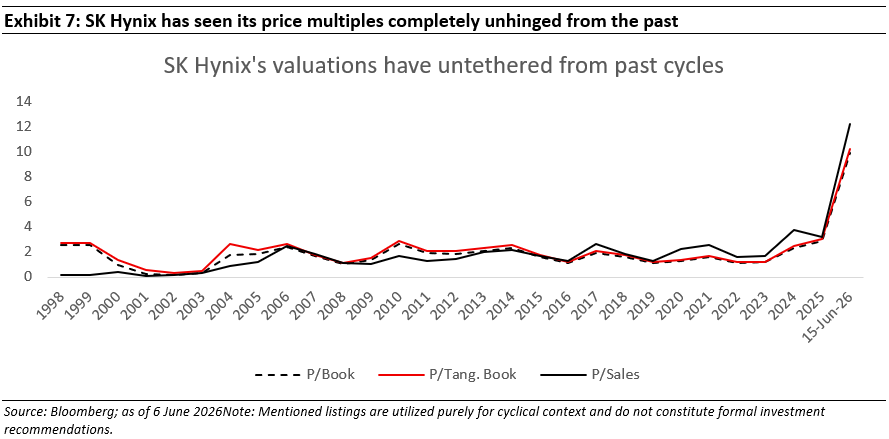

The share price run up seen in memory chip makers like Micron isn’t limited to the US either. As much of the semiconductor supply chain sits in Korea & Taiwan, stocks such as SK Hynix/Samsung have seen their share prices skyrocket too.

While some of the excitement is well founded as higher DC deployment will need higher number of memory chips, the expectations for growth today leave very little room for misjudgement. As can be seen in the chart below, the price multiples of SK Hynix have completely unhinged from the past semiconductor cycles.

Investor excitement is reflected in the 5-year earnings expectations for the Technology sector in S&P500 too which sits at higher level than was seen even during dot com era (see the blue line; as of Jun 11, 2026)

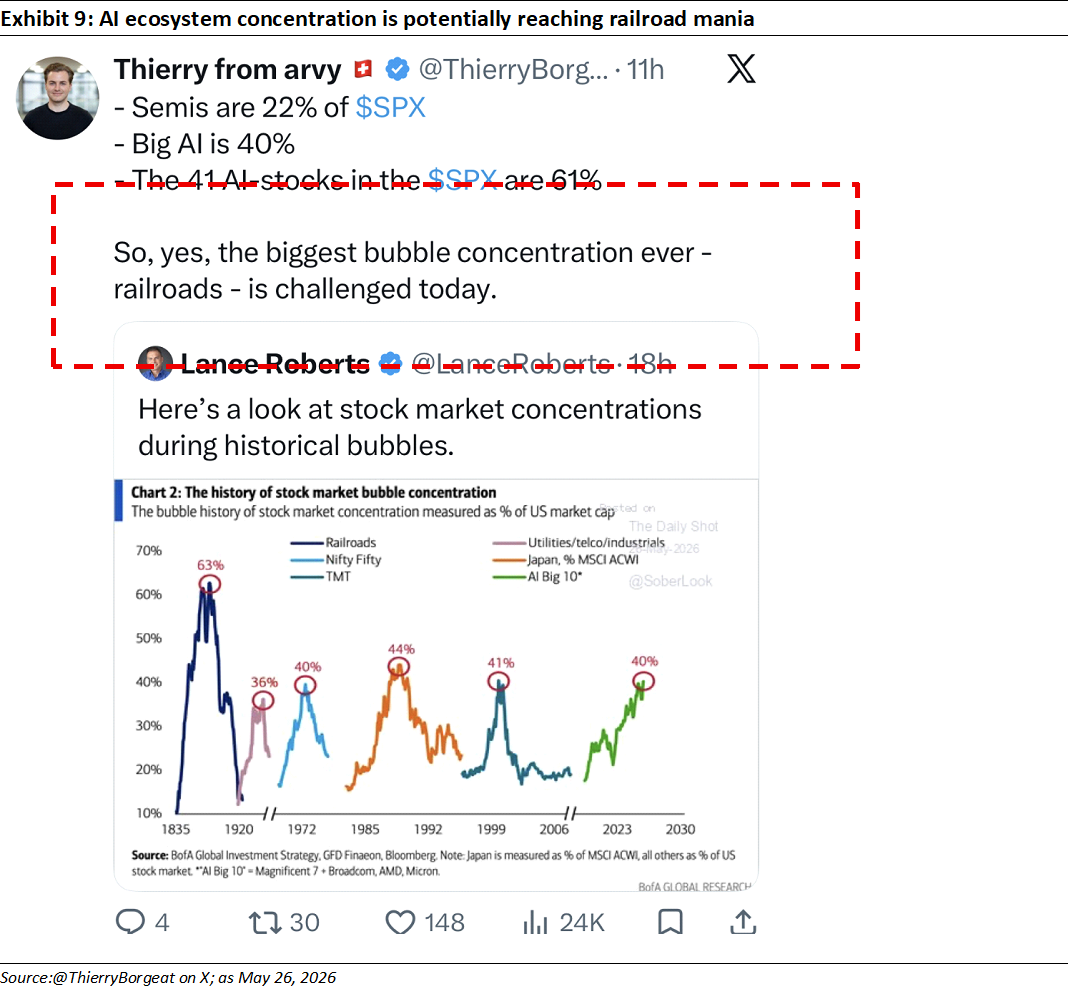

In fact, if you were to include both direct and adjacent (all semis in S&P500) AI plays in S&P500, the concentration today has potentially reached levels not seen since the railroad mania of 1870s.

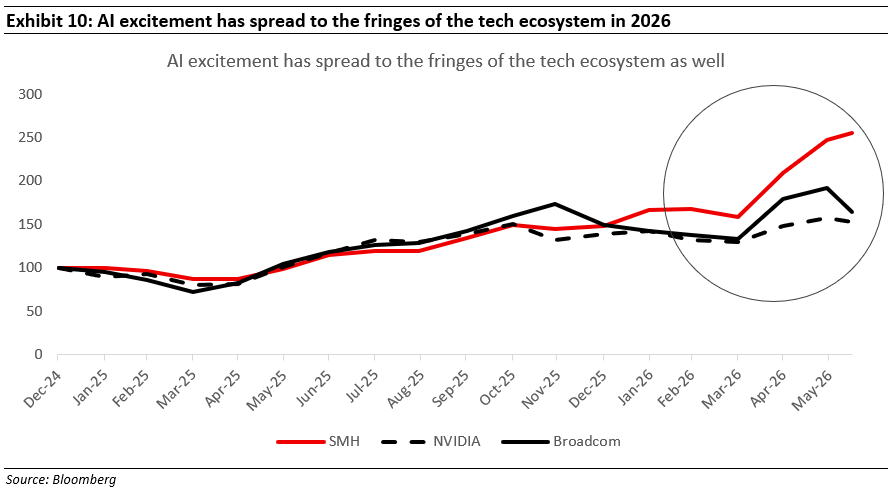

Another key sign that presents itself during peak of such euphoric mania is the breadth spreading to ‘not so great’ part of the ecosystem. This too is evident if one compares the returns of semiconductor ETF SMH to those of core AI capex plays like Nvidia and Broadcom. After staying broadly in line with each other, the excitement has spread to more average names in 2026.

In fact, Roundhill Meme ETF – perhaps created as a bit of a humour after the Gamestop share price rally in 2021 – is one of the best performing ETFs in recent months (up ~67% YTD till 18 June’26). Interestingly, the ETF was launched in Dec’21 and was shut in 2023, only to be relaunched in Oct’25!

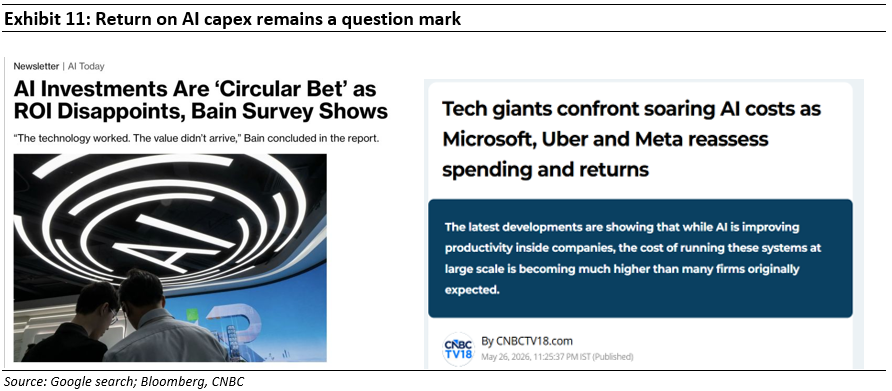

Interestingly, all this is happening even as recent news reports from Bloomberg and CNBC suggest corporates are realising limited productivity benefit vis-à-vis costs of AI spend.

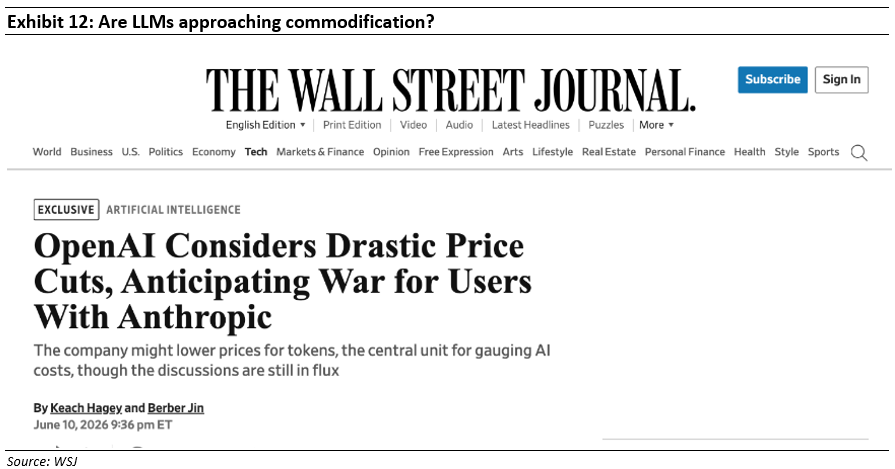

The companies supplying the LLMs meanwhile are planning price cuts even as their Return on capex remains uncertain.

It remains to be seen how the IPOs of Anthropic and OpenAI fare, or how investor interest in SpaceX (which is more AI than space according to its S-1) holds up over coming months. However, if there’s anything the past has shown us, it’s that a frenzy of new issuances during euphoric periods does not meet a happy ending.

History may not repeat but it can certainly rhyme

No one really knows when the last domino falls but history does offer some lessons on what can pan out once it happens. As investors reassess their options, it’s more than likely that money will flow back to businesses and sectors with strong economics and sustainable earnings growth.

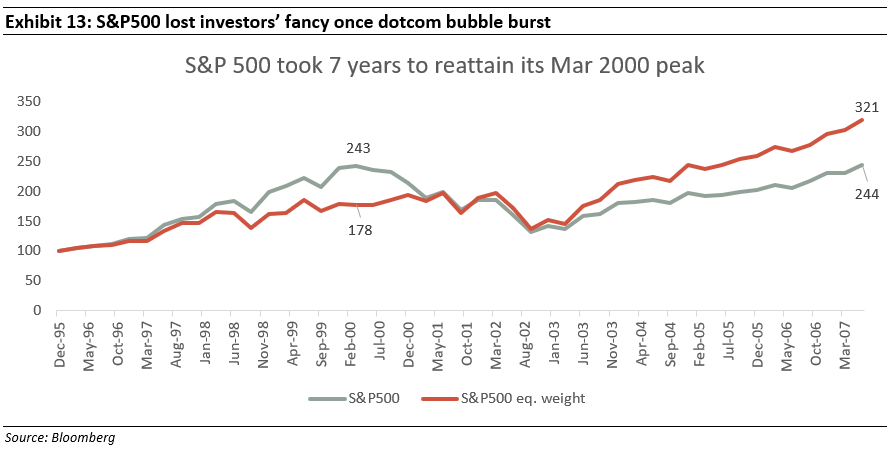

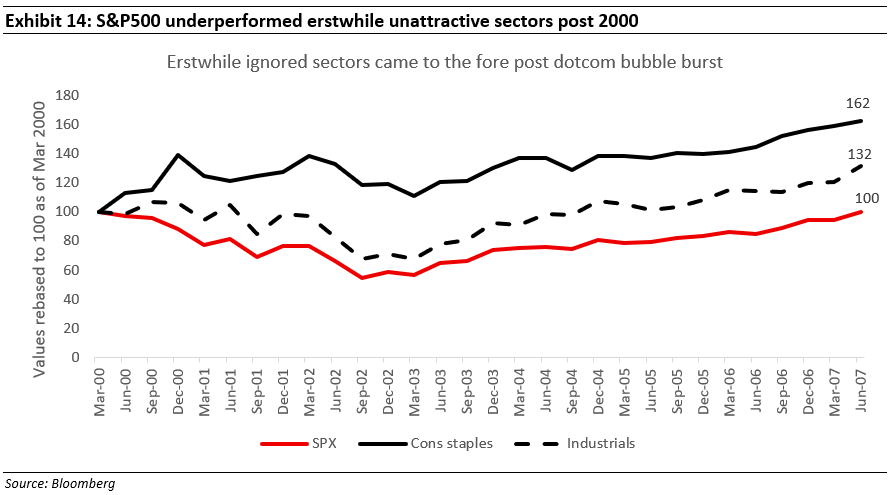

We last saw this happen post dotcom bubble burst. While we see some of the same growth expectations and signs of exuberance, the technology sector is very different today and dominated by large, profitable businesses. Post dotcom, the S&P 500 took 7 years to reclaim its Mar’2000 peak. During this period, it underperformed the S&P500 equal weight index as the erstwhile underperforming sectors like consumer staples and industrials came back to the centre stage.

Long story short, while the headline index may show lacklustre returns, opportunities exist for investors willing to look beyond the prevailing narratives. It’s not as much about ignoring a particular market or geography but rather becoming more discerning regarding what one invests in.

We believe something similar is likely to play out once this frenzy reaches its eventual climax and money finds its way to quality companies currently facing one of the longest periods of investor apathy ever.

It’s worthwhile noting that our portfolio isn’t completely absent from the AI ecosystem. Our exposure across select Mag 7, semiconductors, tech and hardware is around 30% vs. 45-50% for the S&P500. There are some very strong companies there and clear merit in what this technology may enable, keeping us engaged. However, we are actively avoiding the most crowded part of the tech ecosystem where we see the frenzy showing up most clearly.

Given the euphoria discussed across this letter, our own portfolio, which continues to compound low-to-mid teens, can still lag meaningfully when the benchmark is up 20-30%, led by a narrow set of AI and semiconductor-related stocks.

That underperformance is painful, but we take comfort from the fact that our companies are delivering earnings compounding better than expected, at a healthy rate. The gap in stock returns is mainly because the market is currently rewarding a very concentrated set of stocks where expectations and valuations have moved sharply higher.

We are consciously trying not to chase that part of the market at any price. That may hurt near-term relative performance, but it also reduces the risk of permanent capital loss if those expectations are not met. When expectations normalize, we believe the quality and valuation discipline of the portfolio should stand out.

Not only have we avoided being overexposed to the most frothy part of the US market, but we have also taken advantage of sustainably strong earnings growth across Europe and North America to load up on stocks with potentially higher compounding potential….

… but likely trading at attractive valuations.

If the concentrated AI narrative continues for the foreseeable future, we may continue to lag the headline market despite delivering healthy absolute returns. If it does not, then this portfolio’s returns should stand out meaningfully. We leave that probability assessment to our well-informed readers, while continuing to act in what we believe is the most sustainable way to compound wealth over time.

Isaac Newton might not have had the luxury of timeless stock market lessons all those years ago, but we do and at this point we plan on taking the proverbial road less travelled. We hope you join us on the journey.

Regards,

Team Marcellus

If you want to read our other published material, please visit https://marcellus.in/

Disclaimer:

The above material is neither investment research, nor investment advice. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the International Financial Service Centre Authority (Fund Management) Regulations, 2025 (“IFSCA”) as Fund Management Entity – Retail, rendering Investment Management Services. Marcellus is also registered with US Securities and Exchange Commission (“US SEC”) as an Investment Advisor. No content of this publication including the performance related information is verified by IFSCA or US SEC. If any recipient or reader of this material is based outside India or US, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Marcellus and/or its associates, employees, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material.

This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.

Data/information used in the preparation of this material is dated and may or may not be relevant any time after the issuance of this material. Marcellus takes no responsibility of updating any data/information in this material from time to time. The recipient of this material is solely responsible for any action taken based on this material. The recipient of this material is urged to read the Disclosure Document/Form ADV, Form CRS and any other documents or disclosures provided to them by Marcellus, as applicable, and is advised to consult their own legal and tax consultants/advisors before making any investment in the portfolio.

All recipients of this material must before dealing and or transacting in any of the products referred to in this material must make their own investigation, seek appropriate professional advice and carefully read the Disclosure Document, Form ADV, Form CRS and any other documents or disclosures provided to them by Marcellus, as applicable. Actual results may differ materially from those suggested in this note due to risk or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions globally, inflation, etc. There is no assurance or guarantee that the objectives of the investment strategy/approach will be achieved.

This material may include “forward looking statements”. All forward-looking statements involve risk and uncertainty. Any forward-looking statements contained in this document speak only as of the date on which they are made. Further, past performance is not indicative of future results. Marcellus and any of its directors, officers, employees and any other persons associated with this shall not be liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner whatsoever and shall not be liable for updating the document.

The mentioned stocks such as Alphabet (Google), Meta, Microsoft, Amazon, SMH ETF are part of holdings within the Marcellus Global Compounders Portfolio, a strategy offered by the IFSC branch of Marcellus. Accordingly, Marcellus, its employees, their immediate relatives, and clients may maintain interests or positions in these securities. This reference is for illustration and educational purpose only and not recommendatory.