OVERVIEW

POPULAR ARTICLES

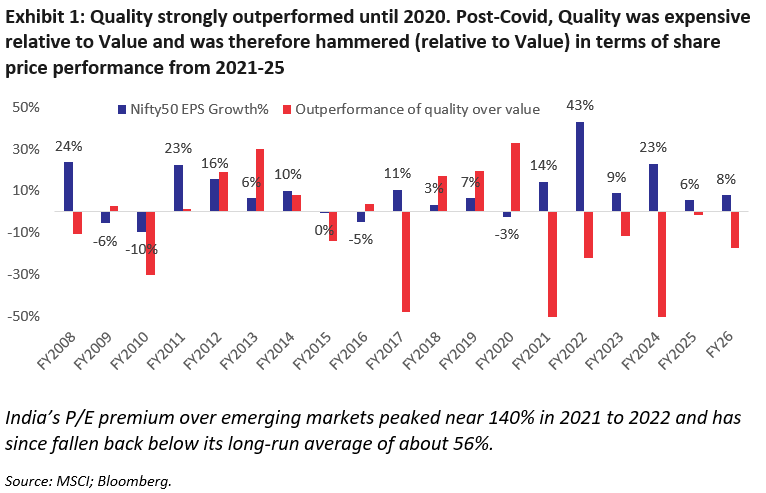

Quality investing lagged for five consecutive years (2021-25) as the twin post-Covid booms – Consumption and Govt capex – lifted all boats and investors moved away from expensive Quality names (trading at 50x earnings) to less expensive Value names (trading at 20x). FY26 was the high-water mark of that distortion: the Value factor returned 14% while Quality fell 3%. That pattern is now reversing because: (a) Quality is no longer trading at a 100% premium to the broader Indian market; and (b) The Indian consumer has run out of savings, Govt capex growth has roughly halved, and the cylical Value stocks have become expensive.

The question is “Can Quality sustain the revival it has seen in 2026?”. We believe it can due to: a) the strong ongoing recovery in earnings growth of Quality companies relative to the rest of the stock market; and b) the likely return of FIIs at some stage in FY27 as they realise that India’s Quality compounders are too attractively valued to ignore.

Why is this relevant for you? Because Marcellus’ Quality centric portfolios like CCP and KCP are staging a strong comeback on the back of the Quality rally.

1. Why Quality Went Out of Fashion?

Quality investing involves investing in high ROE companies with strong governance and clean accounts. Such companies often trade P/E multiples higher than the broader market but for Quality conscious investors like us, that premium has historically been worth paying because it helps us get access to companies which compound more sustainably over longer time periods.

The post-COVID cycle did something that we had never seen in our careers – it created a 5-year reversal against Quality investing in India. In fact, the post-Covid boom rewarded almost everything except Quality. Four forces ran together to produce that result.

Revenge spending lifted every boat

When the pandemic lifted, households unleashed the savings they had been forced to hold through Covid. The “revenge spending” wave, strongest across the Diwali seasons from 2021 to 2023, flooded everything tied to consumption.

In a surge of that intensity, category leadership stops mattering. The category leader and the third-ranked imitator both grew, so investors saw little reason to pay extra for the leaders.

The boom was financed partly out of the savings buffers created during the lockdown rather than out of rising incomes. As the RBI highlighted, by FY23 net household financial savings fell to roughly 5% of GDP, close to a fifty-year low. That distinction did not matter to share prices in the years following Covid. It would matter a great deal later.

Quality was priced for perfection post Covid

Post-Covid, Quality franchises traded at 40 to 50 times forward earnings while large parts of the rest of the market sat at 15 to 20 times. Quality’s earnings did grow faster, but a premium that wide is hard to defend when cheaper growth is everywhere. As we at Marcellus discovered, a Quality franchise can compound earnings in the mid-teens and still de-rate if the stockmarket decides a 45 times multiple should be 30 times. That de-rating kills the share price compounding of a Quality franchise.

The Twin booms in government capex and the global commodity Buildout

To fight the Covid slump, the Government of India ramped public capital spending hard, roughly quadrupling central govt capex from about Rs 2.6 trillion in FY18 to a budgeted Rs 11.2 trillion by FY26. The contractors, railway and defence suppliers and public-sector undertakings on the receiving end saw revenues and order books inflect, many growing more than 30% per annum.

Globally, the world rushed for commodities, and then for the metals, power and infrastructure needed to build out AI and electric-vehicle capacity. Thus commodity and energy producers had a stellar run.

So three large slices of the market – capex and PSUs, commodities, and broad consumption – all roared at once. After a decade of underperformance these slices were cheap, which gave them room to re-rate strongly between 2021 and 2025.

For the first time, the low-quality end of the market won over 5 years

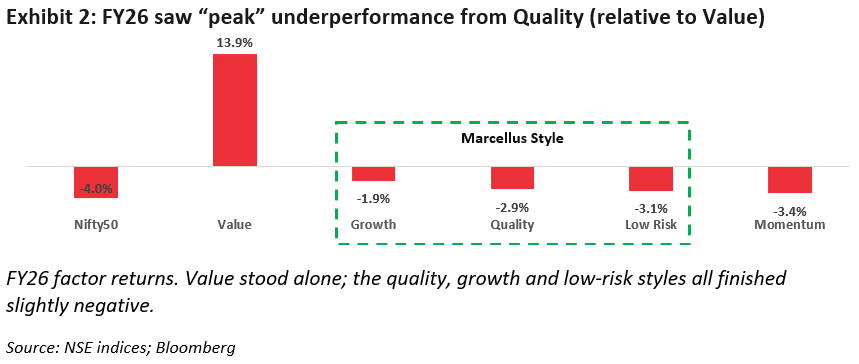

In FY26 the Value factor returned 13.9% while every style Marcellus leans on – growth, quality and low-risk – finished slightly negative, and even the Nifty 50 fell.

The sector split is stark. The FY26 leaders were almost entirely the policy-and-cycle trade, PSU banks, capital markets, metals, defence and commodities. The laggards were the consumption-and-compounding trade, FMCG, IT, private banks and broad consumption. That is the precise inverse of a Quality-led market.

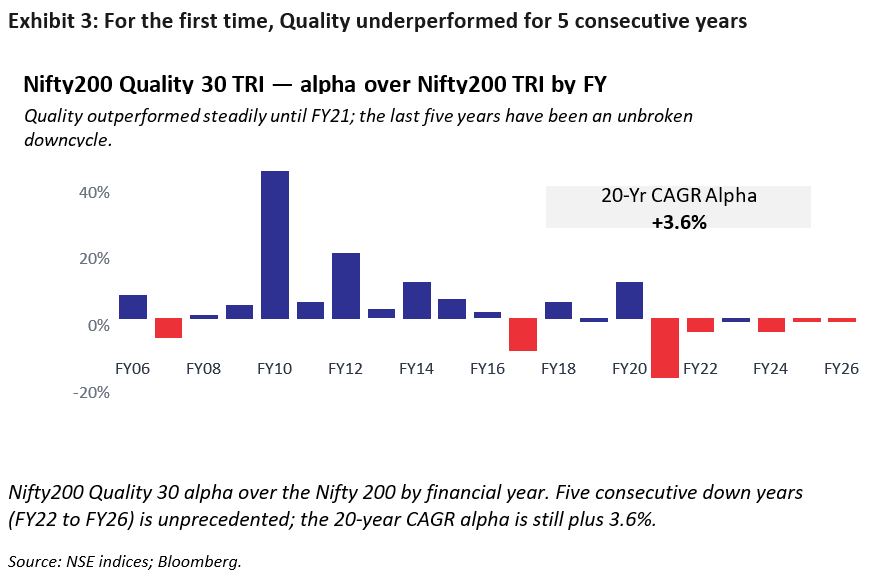

On a rolling five-year basis, the Quality factor’s outperformance over the broad market – which had been reliably positive for most of the prior two decades and compounding at about 3.6% a year over twenty years – turned negative for five straight years from FY22.

2. Why Quality Has Comeback in 2026?

The same forces that buried Quality after Covid have now reversed, and the reversal signals Quality’s comeback. As the Indian consumer’s savings ran dry, the capex tide receded and the Value names stopped being cheap, the stockmarket was left with the one thing it had ignored for five years: businesses that can grow even when the broader economy is struggling.

The consumer ran out of money

From around Diwali 2023 the engine of the boom began to sputter. The savings that had powered revenge spending were largely spent.

With financial savings near multi-decade lows, households borrowed to keep up their lifestyles rather than because incomes were rising. Average debt per borrower climbed roughly 23% in two years, with consumption loans, not home loans, doing the heavy lifting. That kind of spending or borrowed money has a ceiling.

The Government capex tide receded

As white collar jobs growth disappointed in India and as consumption cooled, government tax-revenue growth came under pressure, and with it the room to keep expanding capex.

The pace of central capex growth roughly halved, from compound rates above 20% in the boom years towards closer to 10%.

For companies whose entire case was 30% top-line growth bankrolled by an accelerating government, a slowdown to single digits is a de-rating event. Order books stalled, revenue growth at the contractors and PSUs contracted, and the multiples awarded on the assumption of permanent acceleration unwound.

Valuation reset: India is no longer expensive, and Quality is cheaper still

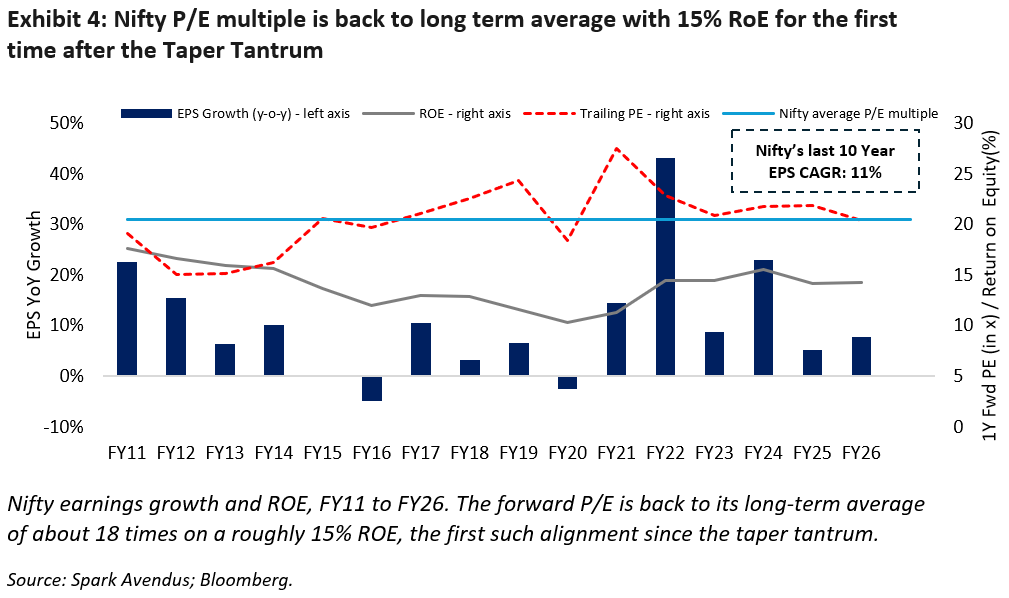

The Nifty’s one-year-forward P/E has fallen back to roughly 18 times, its long-run average, even as return on equity holds near 15%. That pairing of an average multiple for the Nifty on a healthy ROE has not been seen since the aftermath of the 2013 taper tantrum.

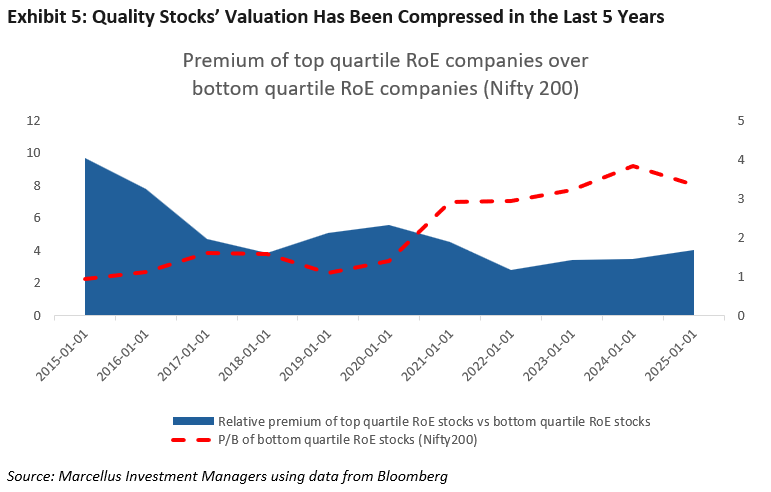

Quality is cheaper still in relative terms. After five years of underperformance, the premium that the highest-return franchises command over the rest of the market has compressed toward the bottom of its range (see exhibit 5).

The Structural Logic: Quality Outperforms When the Economy slows

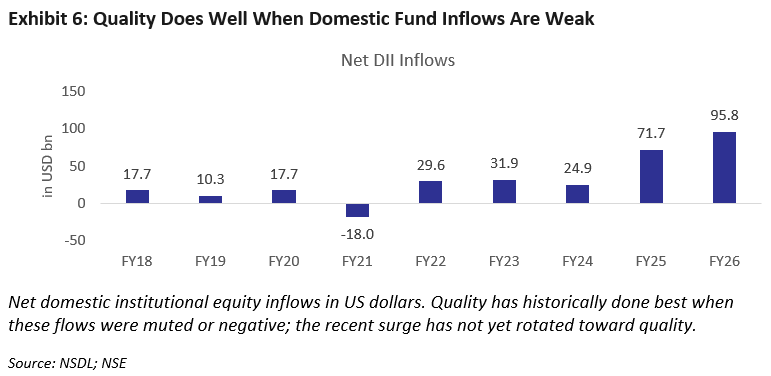

History shows that Quality tends to outperform Value during periods of weak earnings growth, which tend to coincide with weak domestic equity flows and a general sense of crisis. When money floods into the stockmarket and the macro is easy, the speculative and the cyclical stocks tend to lead the stockmarket.

Domestic flows tell the same story from the other side. Weak domestic institutional flows have marked the moments when Quality does best, for example the outflow year of FY21.

3. Can the recovery in Quality sustain?

A few quarters of relative outperformance does not count as a regime change. For the Quality comeback to last, two conditions must hold and a third must repeat. On balance they are aligning, though they do depend on the broad economy continuing to struggle.

Earnings: Quality wins when the broader economy struggles

The earnings gap that Quality needs only opens when the broader economy is having a hard time. Structural signals regarding the Indian economy point to an extended period of pain: weak job creation (as explained in our book “Breakpoint” and in our podcasts such as this: https://www.youtube.com/watch?v=73HEF3IYRcY), the uncertain effect of AI on Services and IT jobs, an already-highly levered household sector and a below-par monsoon.

Flows: India needs foreign investors back, and they tend to favour Quality

Global allocators do not, as a rule, buy crony-capitalist or governance-weak businesses. They buy a small set of transparent, high-return franchises i.e. Quality. The de-rating of quality and the exodus of foreign money from India over the past 4 years are therefore one and the same.

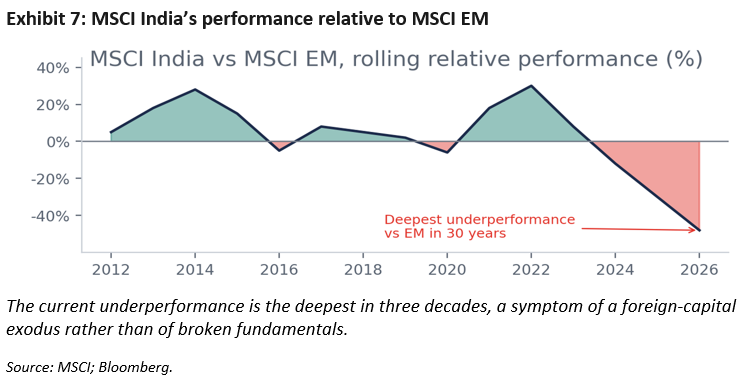

Foreign investors have been net sellers almost continuously since the September 2024 peak, with cumulative outflows on the order of 58 billion dollars. That has driven foreign ownership of Indian equities to a 15-year low, below domestic ownership for the first time, and halved India’s weight in the MSCI EM index from about 20% to under 12%.

The selling has been heavy enough that India has just registered its worst relative performance against emerging markets in thirty years. The marginal returning dollar is far likelier to land in an HDFC-type franchise than in a leveraged road or defence construction contractor. That asymmetry now runs in Quality’s favour.

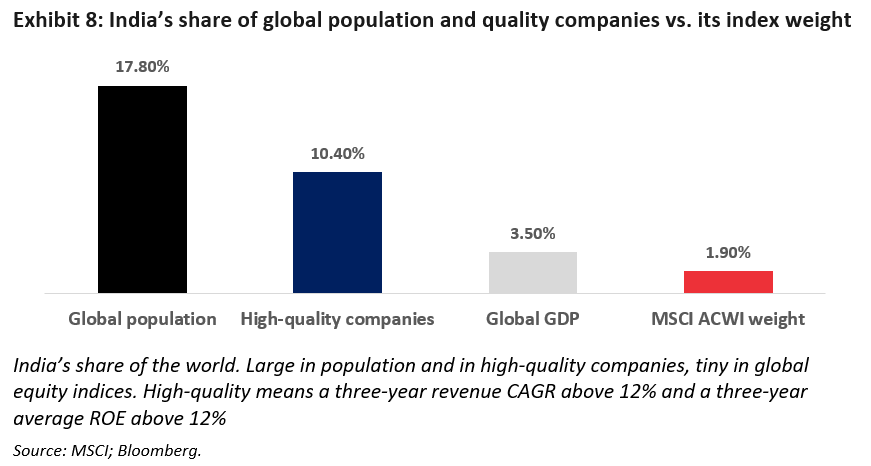

The Quality franchises are less dependent on the economic cycle. India already posts the highest return on equity in the emerging-market complex, around 15%, up from 12% in 2019, and is the only large emerging market with consistent double-digit earnings growth and low leverage. Moreover, that pool of Indian Quality compounders are badly under-represented in global portfolios. India is home to about 17.8% of the world’s people and roughly 10.4% of its high-quality companies, but only 3.5% of global GDP and a mere 1.9% of the MSCI All-Country World Index. As global capital is forced to recognise the quality on offer, the marginal flow has a long way to travel.

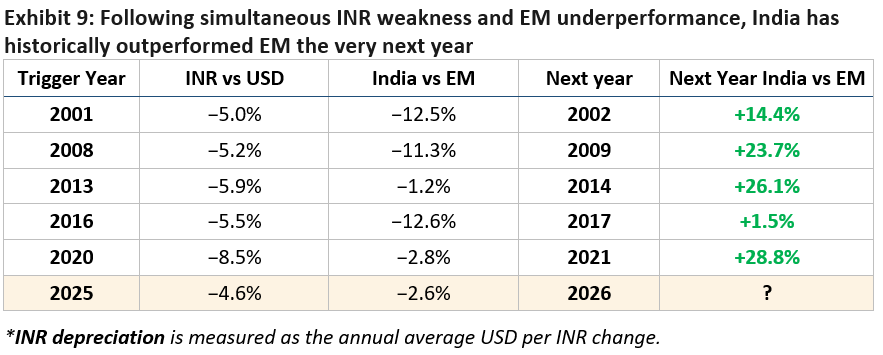

The precedent: the currency-and-EM double whammy points to an emphatic “BUY India” signal

There have been five prior occasions in the past quarter-century when the rupee weakened by more than about 5% in a year at the same time as India underperformed emerging markets. On every single one of them, five out of five, India outperformed the following year.

The average next-year outperformance was about plus 19%. The logic is intuitive: a weak rupee and relative underperformance are symptoms of foreign capital leaving; once that selling exhausts itself, valuations are reset lower, the currency is cheap, and India’s structural growth premium reasserts its pull.

Calendar 2025 reproduced the setup exactly, a weakening rupee alongside India trailing emerging markets, which on this record points to India outperforming through 2026.

India vs EM represents the MSCI India Index minus the MSCI EM Index calendar-year total returns in USD (net).

The Rebound Track Record: As highlighted by the final column, the next-year snapback has boasted a 100% success rate—delivering positive relative returns every single time and yielding a massive historical average outperformance of +19%. Calendar year 2025 has triggered this identical structural setup.

Source: MSCI; Bloomberg.

What would break Quality’s Comeback?

Conviction is worth more when the conditions that would disprove it are named in advance. Three developments would undercut our bet on Quality.

A broad, durable growth reacceleration. The biggest threat to relative quality performance is a strong, broad-based recovery. If jobs, incomes and consumption inflect upward together, the rising tide lifts the weaker boats again, the franchises’ share gains stop standing out, and value and cyclicals reclaim leadership. Quality wins on scarcity of growth, and abundant growth is its enemy.

A global liquidity flood that revives momentum. A sharp, synchronised easing in global financial conditions could re-ignite the speculative, momentum-led end of the market before fundamentals catch up, which would delay the rotation into quality.

Domestic flows sustaining the low-quality trade. Record domestic inflows have cushioned the market. If that bid keeps favouring the speculative cohort rather than rotating toward quality, the low-quality premium could persist for longer than fundamentals justify.

Currently, the odds we believe are stacked against each of these bullets.

Investment Implications

Quality did not go out of fashion because the businesses faltered. It went out of fashion because the post-Covid consumption boom and Government capex boom in India flattered lower-quality franchises which were trading at attractive valuations. Quality has come back this year because those forces have reversed. The Indian consumer has run out of money, the Government capex tide has receded, Value has become expensive for the modest earnings growth it delivers.

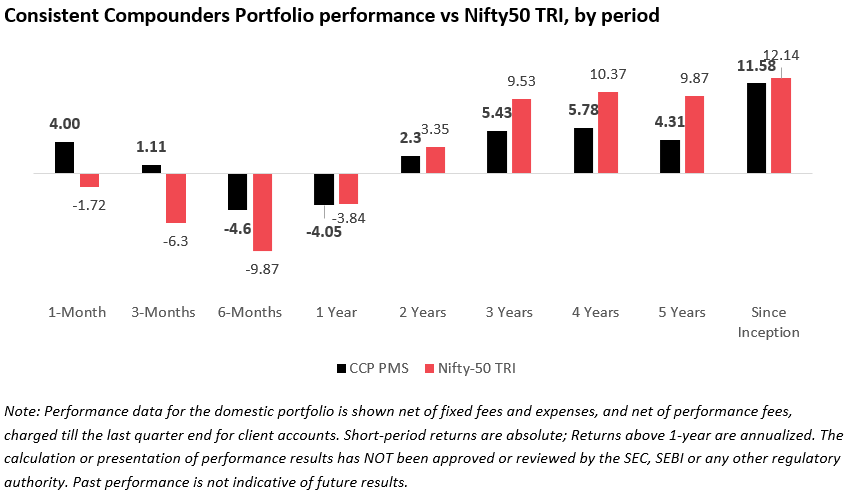

In our Consistent Compounders Portfolio (CCP), we invest in genuinely good-quality businesses with clean accounts and durable profit growth. That is the philosophy behind Marcellus’ Consistent Compounders Portfolio.

*For relative performance of particular Investment Approach to other Portfolio Managers within the selected strategy, please refer https://www.apmiindia.org/apmi/welcomeiaperformance.htm?action=PMSmenu, Under PMS Provider Name please select Marcellus Investment Managers Private Limited and select your Investment Approach Name for viewing the stated disclosure.

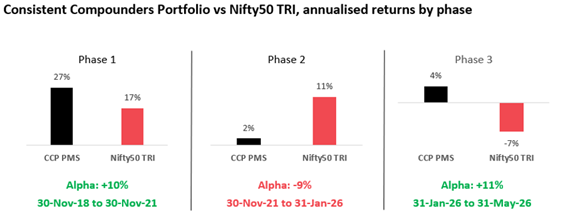

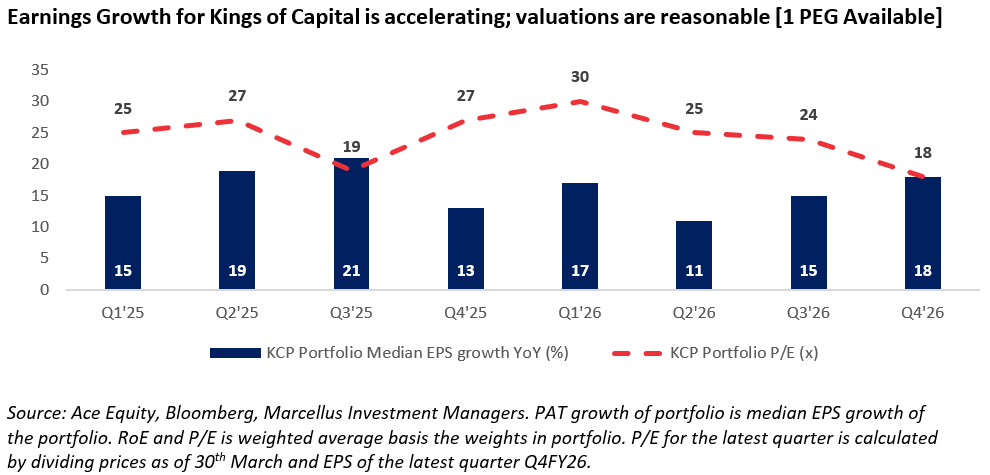

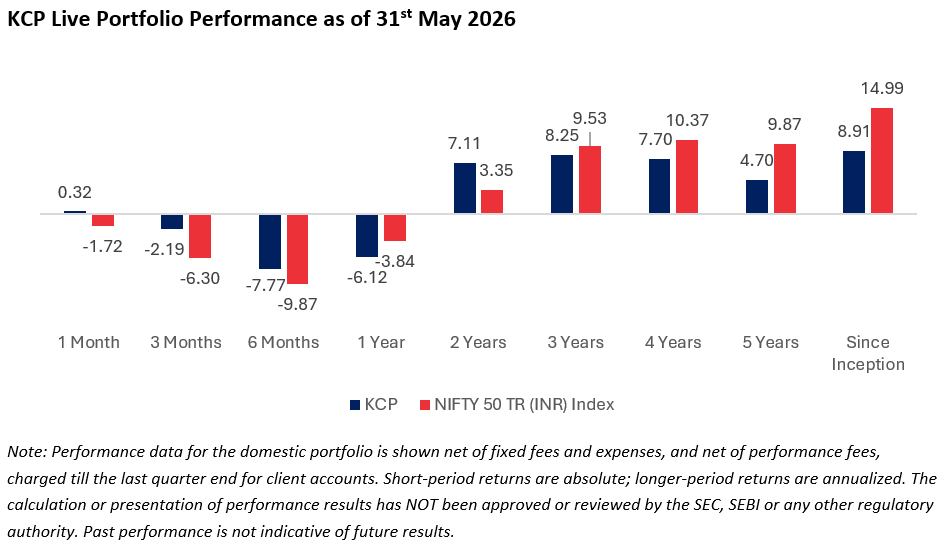

In our Kings of Capital Portfolio (KCP), we invest in a handful of well managed lenders, insurers, investment management firms and financial infrastructure providers. While earnings growth for this portfolio has been consistently better than its peers for the last five years, expensive valuations acted as a headwind. Now, however, valuations are much less of an issue. As a result, returns are compounding at a brisk pace (as can be seen below).

*For relative performance of particular Investment Approach to other Portfolio Managers within the selected strategy, please refer https://www.apmiindia.org/apmi/welcomeiaperformance.htm?action=PMSmenu, Under PMS Provider Name please select Marcellus Investment Managers Private Limited and select your Investment Approach Name for viewing the stated disclosure.

Thanks,

Saurabh Mukherjea

The views and opinions expressed in this material are those of the writers/authors and do not necessarily reflect the official policy. This material is for informational and educational purposes only and should not be considered as financial, investment, or other professional advice.

Click here for details about our regulatory registration and licensing information

Disclaimer:

The above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the International Financial Services Centres Authority (IFSCA) as a Fund Management Entity No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. All recipients of this material must before dealing and or transacting in any of the products/services referred to in this material must make their own investigation, seek appropriate professional advice. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer or an employee. This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.