OVERVIEW

POPULAR ARTICLES

Summary: More than investments in Indian stocks, it is $ investment in the world’s best companies through GIFT City is emerging as an option for NRIs. A GIFT City PMS in global stocks may help in addressing FOUR big challenges for NRIs because: a) it does NOT create PFIC issues; b) it does NOT expose the NRI to INR depreciation; c) it does NOT create high Capital Gains Tax burden for NRIs; and d) it does NOT require creating a PIS account. An added bonus is that $ assets parked in a GIFT City PMS may not be directly subject to certain POTUS’ remittance tax. Marcellus has been offering US$ PMS investing in global stocks via GIFT City since 2022.

Not clear to us as to why NRIs should be big investors in Indian stocks

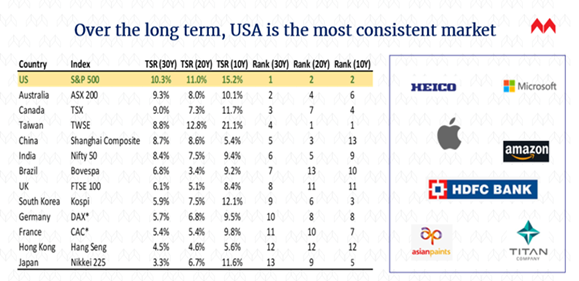

While NRIs’ $ denominated deposits in Indian banks make sound financial sense (what’s there to complain about receiving 6% interest income in $) and while their investments in Indian real estate make emotional sense (especially for those who intend to live in India after retirement), it may be worth evaluating the rationale for significant investment in Indian stocks given the weak $ returns of the Nifty50 over the past decade (just 9.4% p.a. $ returns vs 15.2% for the S&P500).

As is evident from the table below, because the S&P500 has been the one of the stronger performing markets historically for several decades, most NRIs who diversified away from the S&P500 may have experienced relatively lower returns in certain periods.

Source: Marcellus Investment Managers; Bloomberg LP; 30-Year, 20-Year and 10-Year TSR calculated period ending Nov 2025; *Taken from 1st January 1999 when Euro was adopted; all returns expressed in USD terms. For information/education only. Not investment advice or a recommendation.

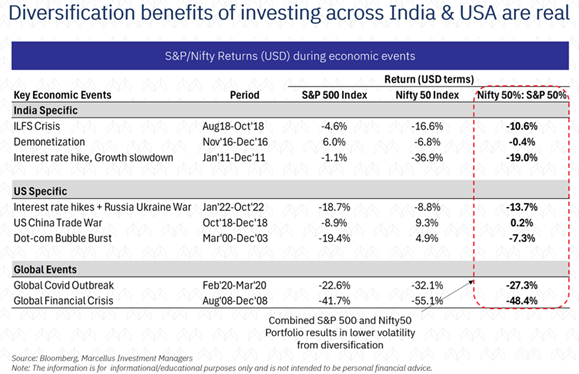

However, because the correlation between the Indian and American stock markets is low (and falling), a case can be made for NRIs to have a small allocation to Indian stocks on the grounds that Indian stocks offer diversification. In simple English, India “zigs” when America “zags” (see table below).

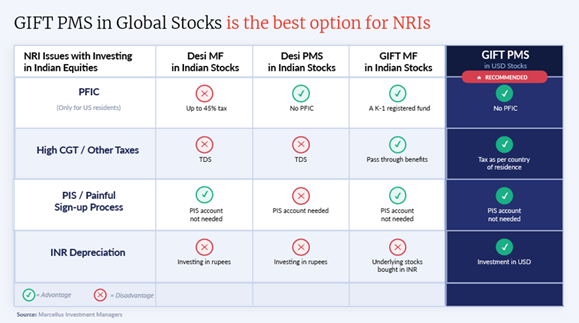

While a sub-10% allocation to Indian stocks makes sense for NRIs (from the point of view of diversification), doing so through Indian mutual funds in mainland India i.e. desi MFs does NOT make sense because of the Capital Gains Taxes (CGT) that have to be paid in India in addition to the PFIC related taxes that have to be paid in USA (for US residents – see below). An alternative approach could be for NRIs to invest in Indian MFs is through GIFT City (which are exempt from paying CGT in India and are not treated as PFIC in USA).

However, for the core of the NRIs’ portfolio, a GIFT City based PMS investing in $ assets around the world (ex-India) trumps everything else. To understand why this is the case, let’s go through the four major pain points that NRI investors have to contend with.

Pain point #1: PFIC and high taxes in USA – A Passive Foreign Investment Company (PFIC) is taxed by US authorities at a penal rate of 37% ordinary income + interest surcharge. Our maths suggests that this effectively works out to a CGT of 45% on an investment held for 3-4 years. In addition, NRIs resident in USA have to file Form 8621 per fund per year. Remember, US CPAs charge $100-300 per PFIC annually.

A foreign corporation is considered by the US authorities to be a PFIC if it meets any one of the following criteria:

· Income Test: 75% or more of the company’s gross income is passive (e.g., dividends, interest, capital gains, or royalties).

· Asset Test: 50% or more of the company’s assets produce—or are held to produce—passive income.

The bad news is that Indian mutual funds are deemed by the US authorities to be PFICs. Non-filing of PFIC investments with the US tax authorities mean indefinite IRS audit exposure. Most US NRIs avoid desi MFs entirely.

Investing in $ assets in GIFT City (either as PMS or in fund format) avoids anything to do with PFICs. The NRI may be required to pay CGT in his country of residence as per the normal CGT rules of that country.

Pain point #2: High CGT and other taxes in India – If an NRI invests in stocks in mainland India, he/she has to pay 20% Tax Deductible at Source on her realised short term capital gains plus a cess and a surcharge. The same would apply if the NRI invested in desi MFs. In addition, he/she will also have to pay STT every time he/she transacts in Indian stocks.

In contrast, an NRI investing in $ assets globally through a GIFT City PMS may not be subject to certain taxes in India, subject to applicable regulations i.e. there is NO CGT or STT to pay in India. The NRI simply pays CGT on realised gains in his country of residence.

Pain point #3: Opening a PIS account is painful –To invest in mainland India (but not GIFT City), NRIs have to open a Portfolio Investment Scheme (PIS) account. This account is operated under a specialized framework established by the Reserve Bank of India (RBI) under the Foreign Exchange Management Act (FEMA). It allows Non-Resident Indians (NRIs) and Persons of Indian Origin (PIOs) to invest in shares of listed Indian companies. Unfortunately, opening such an account is a lengthy process involving physical identity verification. The NRI either has to go to the Indian embassy in the country of his residence OR visit India to open a PIS account. As if the initial pain to open a PIS is not enough, every 2-3 years the NRI is required to go through a re-KYC process for which she has furnish a long list of documents to prove identity & address (again).

Thankfully, operating a PMS account (or a fund) in GIFT City does NOT require a PIS account.

Pain point #4: Sustained INR depreciation – Since 1991, the INR has historically averaged around 4% of its value to the $ each year implying that the BSE500’s 20-year return CAGR of around 12.81% in INR is only 8.74% in $. If you knock-off forex charges, the returns drop to sub-8% which is hard for NRIs to swallow given that the US stock market has delivered returns in excess of 10% p.a. over 10, 20 and 30 years and done so with lower volatility than the Indian market. Investing in $ assets – including American and European stocks – via a GIFT City PMS account makes INR depreciation a non-issue.

Not only does GIFT City address the 4 pain points highlighted above, but there is also a further bonus. If an America-based NRI keeps his $ assets in a GIFT based PMS, then even if the US President decided to slap higher taxes on NRIs’ remittances to India, the $ investments held in GIFT City would be outside the reach of POTUS.

Solution from Marcellus: $ investing in Global stocks

Marcellus offers THREE ways in which investors (resident and non-resident) can gain access to the same underlying $ assets in the form of Europe, America and East Asia’s best managed companies:

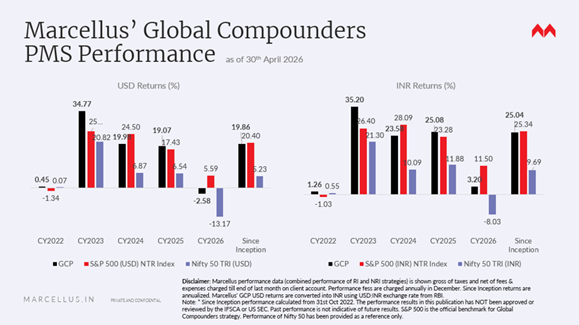

1. A US$ PMS in global stocks in GIFT City. This is our Global Compounders Portfolio, and it has delivered ~20% p.a. US$ returns (net of all fees & expenses) since inception in Oct ’22 – see chart below. Minimum ticket size is $75K. This $ PMS construct is suitable for NRIs based on individual risk profiles.

2. A US$ AIF in global stocks in GIFT City. This is the Alternative Investment Fund version of our Global Compounders Portfolio. Minimum ticket size is $150K. This fund is suitable for RESIDENT Indians.

3. A Cayman Islands domiciled version of our Global Compounders Portfolio. This fund is intended for eligible non-resident investors, subject to applicable laws and regulations and may provide K-1 to US taxpayers. Minimum ticket size is $100K.

Please note, for more details, please refer to the disclosure and offer documents. This is for awareness only, not an offer or solicitation.

Note: Marcellus performance data is shown gross of taxes and net of fees & expenses charged till end of last month on client account. Performance fees are charged annually in December. Returns more than 1-year are annualized. Marcellus’ GCP USD returns are converted into INR using USD: INR exchange rate from RBI – Link for the reference. Since Inception performance calculated from 31st Oct 2022. The inception date is 31st Oct 2022, being the next business day after the account got funded on 28th October 2022. S&P 500 net total return is calculated by considering both capital appreciation and dividend payouts. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the IFSCA or US SEC. Performance is the combined performance of RI and NRI strategies. S&P 500 NTR is the benchmark for the strategy. Nifty 50 is provided for reference to illustrate the relative performance of the US and Indian markets.

Marcellus GCP PMS is offered by Marcellus Investment Managers GIFT Branch in a segregated managed accounts format.

Thanks

Saurabh Mukherjea

Click Here for details about our regulatory registration and licensing information.

Disclaimer:

This material is for informational purposes only and does not constitute investment advice or research. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the International Financial Services Centres Authority (IFSCA) as a Fund Management Entity (Retail) and registered with the U.S. Securities and Exchange Commission (SEC) as an Investment Advisor. The mentioned Cayman Fund is registered with the Cayman Islands Monetary Authority (CIMA) and it is managed by Marcellus International Investment Managers LLC (USA). GIFT based fund is a Category III Restricted Scheme under the IFSCA (Fund Management) Regulations, 2025. The Cayman Fund is sub-advised by Marcellus Investment Managers Private Limited – IFSC Branch. The contents herein including performance numbers, if any, have not been reviewed or verified by IFSCA, CIMA or US SEC.

This communication is not a solicitation in jurisdictions where Marcellus is not regulated. It is confidential and intended solely for the addressed recipient; unauthorized use or distribution is prohibited. carefully read the Disclosure Document, Form ADV, Form CRS and any other documents or disclosures provided to them by Marcellus, as applicable. Actual results may differ materially from those suggested in this note due to risk or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions globally, inflation, etc.

Information provided is based on data available at the time of preparation and may change without notice. Marcellus makes no representation regarding accuracy or completeness and assumes no obligation to update. Recipients should rely on their own judgment and consult independent legal, tax, and financial advisors before making any investment decisions.

Investments are subject to market risks and uncertainties. This material may include “forward looking statements”. All forward-looking statements involve risk and uncertainty. Any forward-looking statements contained in this document speak only as of the date on which they are made. Past performance is not indicative of future results, and there is no assurance that investment objectives will be achieved. Marcellus, its affiliates, employees, and authors may have financial interests in securities discussed.