OVERVIEW

POPULAR ARTICLES

Summary: The quantum of ESOPs held by Indians in foreign companies is orders of magnitude larger than ESOPs held in desi companies. And yet, this is a mixed blessing because foreign ESOPs are illiquid, tax-inefficient and tricky to manage. Marcellus recommends 3 simple steps which can help Indians make the most of these stock options: (1) Move portfolio concentration from one stock to a diversified US$ global portfolio; (2) Map out your life goals and use a range of global & local funds to achieve these goals; and (3) Review & rebalance your global investments annually in a tax-efficient & cost-effective manner.

Introduction

India now hosts over 2000 Global Capability Centers (GCCs). These GCCs employ over 2 million people, many of whom are employed in roles involving cutting edge Technology & Finance. Almost all foreign-listed parents (Microsoft, Google, Amazon, JPMorgan, Goldman, Walmart) grant RSUs (Restricted Stock Units) and ESOPs (Employee Stock Options) to their Indian employees on globally uniform terms. Such equity compensation is typically 30-60% of total compensation for senior executives working in these GCCs run by multinational companies. As a result, the total value of these ESOPs held by Indians working in GCCs runs into several tens of billions of dollars, far exceeding the value of ESOPs held by Indians in Indian listed companies.

Microsoft, Amazon, Alphabet Inc. (Google) JP Morgan Chase are constituent holdings within the Marcellus Global Compounders Portfolio, a strategy offered by the IFSC branch of Marcellus Investment Managers Private Limited and regulated by the IFSCA. Accordingly, Marcellus, its employees, their immediate relatives, and clients may maintain interests or positions in these securities. Any reference to these companies is intended strictly for informational and educational purposes within the context of this discussion and should not be construed as investment advice.

Value of ESOPs held by Indians in foreign companies: What we can figure out from public disclosures

|

Input |

Value |

Source |

|

Total GCC employees in India (2024-25) |

1.9 million |

Nasscom-Zinnov GCC Annual Report 2024 / Feb 2025 |

|

GCC salary premium vs IT services (TeamLease) |

12-20% higher than IT services |

TeamLease Digital ‘Digital Skills & Salary Primer 2024-25’ |

|

GCC software developer salary range |

₹9.7 lakh – ₹43 lakh per year |

TeamLease Digital (Aug 2024) |

|

Variable + LTI as % of fixed salary in GCCs (2025) |

Variable 16.1% of fixed; LTI 45-50% at senior leadership |

CXO Digital Pulse / NHRDN GCC Report (2026) |

|

Google L5 software engineer in India: median total comp |

₹1.8-2.2 crore/year (~35-45% RSU) |

Levels.fyi (verified data, May 2026) |

|

Nvidia software engineer in India: median total comp |

₹68 lakh/year (significant RSU weight) |

Levels.fyi (verified data, April 2026) |

|

JPMorgan India headcount (largest US-bank GCC) |

55,000+ (~1/5 of global JPM workforce) |

Inductus / Tradebrains (2025) |

|

Wells Fargo India headcount |

~37,000 |

Sansovi GCC Top Performers 2025 |

|

Citi India headcount |

~32,000 |

Sansovi GCC Top Performers 2025 |

|

Bank of America India headcount |

~28,000 |

Sansovi GCC Top Performers 2025 |

|

Microsoft India Development Centre headcount |

18,000+ across 10 cities |

Inductus (May 2025) |

Source: Nasscom-Zinnov India GCC Landscape Report (5-Year Journey, 2025); TeamLease Digital Skills & Salary Primer 2024-25 (via Business Standard, Aug 2024); CXO Digital Pulse: ‘The Salary Race in India’s GCCs Is Over’ (April 2026); Levels.fyi (verified compensation data, 2026); Inductus ‘Top US Companies via GCCs’ (May 2025); Tradebrains ‘Top GCCs in India by Revenue 2025’.

The problem: Undue concentration in tax-inefficient ESOPs

What we are observing in the portfolio reviews that we do for our clients is that while the older generation is over-indexed on real estate, the newer generation is over-indexing on ESOPs and RSUs which they receive as part of their compensation. In other words, while one generation is locked into physical assets, the next is getting locked into financial assets in the form of equity from their own employers.

Global wealth managers like Fidelity and JPMorgan Private Bank flag any single stock above 5-10% of net worth as a problem requiring active management. We’re increasingly seeing investment portfolios, especially of senior professionals in tech, fintech, and quick commerce companies, where 30–70% of their net worth is tied to one company’s stock in the form ESOPs or restricted stocks RSUs.

Stock as percentage of total compensation

|

Cohort |

Stock as % of total comp |

Source |

|

Foreign GCC — junior engineer (e.g. Google L3 in India) |

15-25% |

Levels.fyi (May 2026) |

|

Foreign GCC — senior engineer (Google L5, Microsoft 64+, Amazon SDE3) |

35-50% |

Levels.fyi (May 2026) |

|

Foreign GCC — Director / Principal |

50-65% |

Levels.fyi (May 2026); CXO Digital Pulse Apr 2026 |

It could be the company they are currently work for, or one they left a few years ago, but the ESOP holding just kept growing in value during the bull market. And because the stock did well, the employee never felt the need to sell or divest out of it. So, they’re sitting on huge paper gains, feeling secure — but it’s actually a house built on one pillar.

Furthermore, more often than not this single pillar is largely built around ESOPs in companies which are listed abroad implying significant challenges around Estate Duty, Capital Gains Tax and foreign brokerage accounts as and when the stock options are exercised.

Challenge #1 with ESOPs in foreign companies: Emotional biases

We are emotional beings, and as we keep seeing again and again – emotions come in the way of rational decision making. In investing this comes in the form of behavioural biases.

Any rational investor would know that having 30% or more of your wealth ties to a single stock is not smart investing. But the familiarity bias says – “I know my company really well, so it must be safe”. The recency bias says, “it’s done well, so it will continue to do well”. The status quo bias says – “Oh to sell or not is a big decision – so let’s just leave it as is for now”.

And the concentration is not just of value of the ESOP. The employee’s human capital i.e. salary, bonus, career is already fully concentrated in that company. So, it’s mega concentration of both the employee’s existing and future wealth in a single company.

Challenge #2 with ESOPs in foreign companies: Tax aversion

There is an element of tax incidence when the employee exercises or sells her stock options. Because this tax impact results in a cash outflow right now, most of us remain averse to it. In fact, this tax impact has multiple layers to it in the case ESOPs in companies listed abroad.

Firstly, Capital Gains Tax (CGT) on foreign stocks is at an employee’s maximum marginal rate if these investments are sold in less than 2 years. For senior employees, the maximum marginal rate can be as high 42% – a rate high enough to make most investors procrastinate.

Secondly, unlike India, many developed economies have Estate Duties or Inheritance Taxes which have to be paid by the inheritors when the owner of the assets dies. For example, the heirs of Indian residents holding direct US shares above $60,000 in value can face up to 40% US estate tax on death. We have seen first-hand how difficult and time-consuming this process can be for Indians living in India trying to pay Estate Duties in America on shares in American companies.

Challenge #3 with ESOPs in foreign companies: Not wanting to abandon US$ linked compounding

Over the past decade, the S&P 500 has compounded at 15% p.a in US$ terms whereas the Nifty 50 has compounded at a mere 6.5% p.a. Indian employees of the global tech giants having seen decadal compounding in excess of 20% p.a. in $ terms are naturally reluctant to move their assets into India for fear of missing out on further compounding in US$ assets. This aversion to sell US$ assets is even greater for those Indians who expect to see their children to go to college in America. In their mind, their US$ denominated ESOPs are effectively their children’s college fund.

Solution #1 from Marcellus: GIFT City based Marcellus’ Global Funds (USD)

Four years ago, we began investing our clients’ monies globally from GIFT City in Gujarat. We now have multiple tax-efficient and cost-effective US$ based Global funds based out of GIFT City. These funds address all of the challenges highlighted above facing ESOP holders in foreign companies. Specifically, these funds:

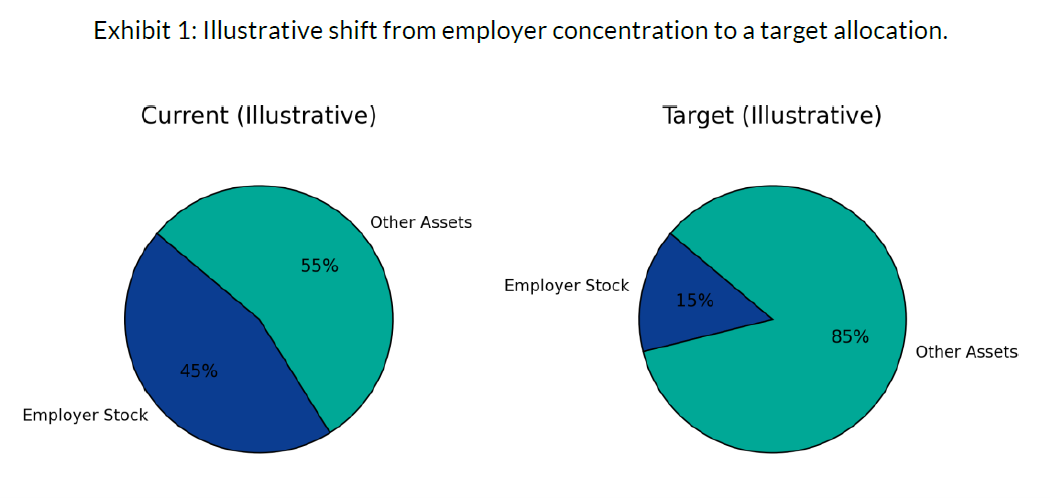

· Move portfolio concentration from one stock to a diversified portfolio: Move from employer concentration to a curated basket of quality globally dominant companies which sit inside a professionally managed and diversified portfolio.

· Breaks career + capital coupling: Your human capital remains tied to your employer; your financial capital now becomes a function of the global dominant companies sitting inside your portfolio.

· Cut through behavioural biases: A structured format enforces diversification and discipline—removing emotional anchors.

· Allow employees to stay invested in US$ & avoid forced INR conversion: Invest directly in USD currency—avoid USD→INR conversion anxiety and costs associated with it.

· Create global spending capacity beyond LRS caps: Global investments via GIFT City can facilitate larger, timely diversification without relying solely on the USD 250k/year LRS window (subject to prevailing IFSC regulations and your onboarding route).

· Give Indian investors an estate‑planning advantage: By holding fund units in a $-denominated fund instead of U.S. securities directly, our funds help investor avoid potential U.S. estate‑tax exposure associated with direct holdings. This significantly simplifies wealth transfer for heirs.

Contact us on invest@marcellus.in to invest globally with us in a tax-efficient & cost-effective manner.

Solution #2 from Marcellus: Goal-based asset allocation

Marcellus has a free goal planning and asset allocation service wherein anyone can reach out to us and get a detailed 4-page financial report free of charge.

We work with a three-step approach to help our clients diversify globally:

1. Map your life goals to financial goals. How much do you need for near, medium, and long-term goals?

2. Allocate your investments across multiple uncorrelated asset classes. Avoid over concentration, illiquidity and disproportionate risk-reward. Get the allocation right based on your needs and your risk tolerance.

3. Remain disciplined. Continue to save and channel savings to investments. Review and rebalance regularly.

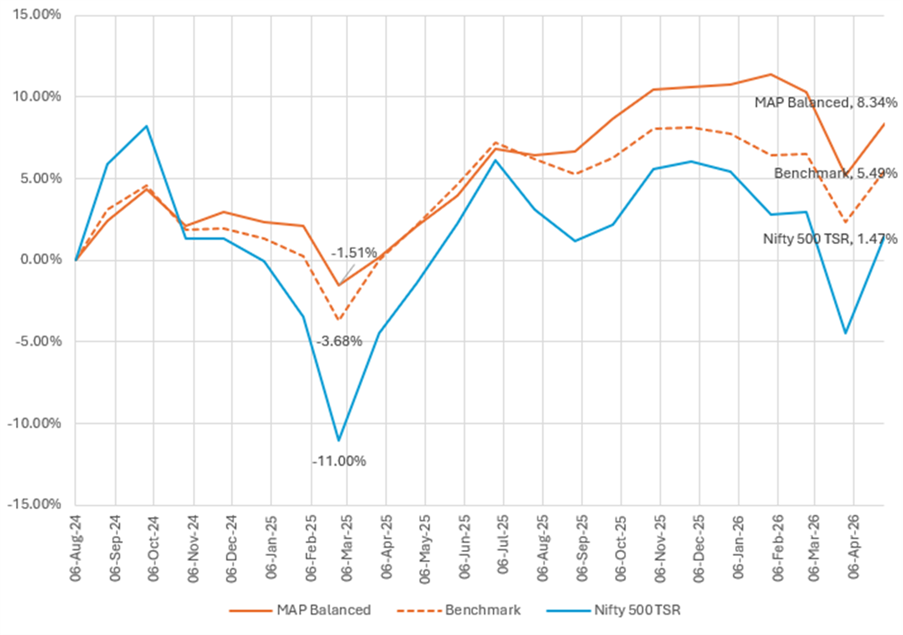

Marcellus’s ‘MAP-Balanced’ which has delivered 8.34% returns since inception in Aug-24 to April-26 net of all fees and costs against 1.47% of Nifty 500 TSR (see the chart below).

Source: Marcellus Investment Managers; Marcellus Performance Data shown is net of fixed fees and expenses charged till 31st March 2026 and is net of Performance fees charged for client accounts, whose account anniversary / performance calculation date falls upto the last date of this performance period; Returns more than 1-Year are annualized; other time period returns are absolute. For relative performance of particular Investment Approach to other Portfolio Managers within the selected strategy, please refer to https://www.apmiindia.org/apmi/welcomeiaperformance.htm?action=PMSmenu. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the SEC, SEBI or any other regulatory authority.

If you would like to to avail of this free service (with no-strings attached) then either scan the QR code below OR visit plan.marcellus.in.

Please note that this is neither a financial plan, nor an investment advise.