OVERVIEW

POPULAR ARTICLES

Industrial policy refers to government officials channelling resources to particular industries that the market would not. What India’s leaders understood many decades ago was acknowledged a fortnight ago by the World Bank – that every country should now have an industrial policy. Companies in our Global Compounders Portfolio are well positioned to potentially benefit from this thanks to their critical positions in tech, AI, power, defence and biotech supply chains.

Source: World Bank

In 1993 the World Bank published a famous report which said that developing economies should focus on getting the basic things required for a functioning free market economy in place e.g. healthcare, law & order, education, etc and then step out of the way. Specifically, the World Bank instructed developing economies to not do anything which jeopardised macroeconomic stability (such as running big budget deficits on the back of heavy subsidies). “The state’s role, where acknowledged at all, was cast as facilitative rather than directive — getting the basics right and then stepping back.”

33 years on from that highly influential report, the World Bank changed its position by 180 degrees. On 17th March 2026, the World Bank published a 276-page report which acknowledged what the Indians and the Chinese have known for decades i.e. “…. governments around the world are increasingly turning to a once controversial policy. Industrial policy—the range of policy tools governments use to shape what an economy produces, rather than leaving it to markets alone—is back with a vengeance.

Contrary to recent headlines, advanced economies are not the heaviest users of industrial policy. As this report documents, developing economies use it more intensively. New data show that total business subsidies among upper-middle-income economies now average 4.2 percent of GDP—the highest on record. Middle-income economies have higher average import tariffs and more dispersion of tariffs across individual products compared to high-income economies—evidence of stronger targeted protection of certain industries. A review of the latest national development plans across 183 economies finds that low-income economies target growth in 13 industries on average, more than twice the number in high-income economies.”

With the World Bank now blessing the use of industrial parks, production subsidies, demand subsidies, tax incentives, tariffs, exchange rate devaluation, etc to boost industrial production, across the world we may see increased adoption of approaches similar to those used in India:

- Mobile phones i.e. give firms like Apple a Production Linked Incentive equivalent to 5% of its incremental sales of goods manufactured in India.

- Chip manufacturing i.e. give firms like Micron subsidies equivalent to 70% of its production costs.

- Datacentres in Andhra built by hyperscale’s like Alphabet and Microsoft i.e. heavily subsidised land, power at a subsidised rate of Rs 1/unit, 25% subsidy on water, 100% reimbursement of Net SGST and a 25 year long holiday from paying corporate tax.

The investee companies in our Global Compounders Portfolio appear well positioned to potentially benefit from the worldwide return on industrial policy. “The evidence for industrial policy was always there. What has changed is the geopolitical context. Western nations now actively need industrial policy to compete, especially with China. Semiconductor supply chains, electric vehicle manufacturing, critical minerals processing — these are the battlegrounds of great power competition.” In our July 2025 newsletter ( Global Compounders: Greatness and Value Capture – Marcellus) we had explored how Apple had captured significant value from its China centric supply chain. Variants of this playbook is what large global franchises can benefit from.

As almost every large economy now seeks to scale up its defence industry, its EV manufacturing, its semiconductor manufacturing and its pharma/biotech manufacturing industry in this age of rage (see here for our March 6, 2026 blog on this) and economic warfare (see here for our March 9, 2026 blog on this), they may increasingly engage with companies like Apple, Alphabet, ASML, TSMC, Airbus, GE Aerospace, Safran and Danaher for potential investments (just as India has done over the past five years).

Investment implications for you

Nearly four years ago, we decided to consciously to build a global portfolio which benefits from critical chokepoints in the global economy around tech hardware & software, around pharmaceuticals/biotech and around defense & aerospace. As the rest of the world now realises that these powerful companies own essential technologies central to the functioning of modern economies, the people running these countries will continue to roll out industrial policies to welcome our investee companies. You may consider participating by joining us in our global compounding journey.

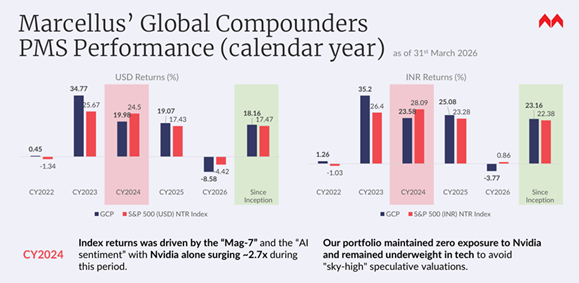

Thanks to the regulatory reforms expedited by the Indian authorities over the past couple of years (see my January 7, 2026 blog: Four Mega Reforms Which Opened up Global Investing for Indians), you now able to diversify globally in a cost-efficient and tax-efficient manner thereby benefitting from this new age of rage. Our track record in compounding across the world is shown below. Since inception in Oct 2022, the strategy has delivered at ~23% CAGR (net of all fees & expenses in INR).

If you would like more information about our global strategy, please reach out to us by replying to this email.

Note: Marcellus performance data is shown gross of taxes and net of fees & expenses charged till end of last month on client account. Performance fees are charged annually in December. Returns more than 1-year are annualized. Marcellus’ GCP USD returns are converted into INR using USD: INR exchange rate from RBI – Link for the reference

Note: * Since Inception performance calculated from 31st Oct 2022. The inception date is 31st Oct 2022, being the next business day after the account got funded on 28th October 2022. S&P 500 net total return is calculated by considering both capital appreciation and dividend payouts. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the IFSCA or US SEC. Performance is the combined performance of RI and NRI strategies.

Marcellus GCP PMS is offered by Marcellus Investment Managers GIFT Branch in a segregated managed accounts format.

Thanks

Saurabh Mukherjea

The stocks Apple, Alphabet, Microsoft, ASML, TSMC, Airbus, GE Aerospace, Safran and Danaher are part of the Global Compounders Strategy managed from GIFT City by Marcellus and regulated by IFSCA. Marcellus, its employees, their relatives, and clients have an interest in these stocks.

This material is for informational purposes only and does not constitute investment research or advice. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the IFSCA as a Fund Management Entity – Retail and is also registered with the U.S. SEC as an Investment Adviser. The contents, including any performance information, are not verified by IFSCA or the U.S. SEC. Past performance is not indicative of future results. Investments involve risk, including loss of principal. Recipients should seek independent legal, tax, and investment advice.