OVERVIEW

POPULAR ARTICLES

Over the past 20 years, America has led the world in using economic chokepoints to hurt its rivals. First China (using rare earths) and now Iran (using Hormuz) are returning the compliment. It is all but inevitable that every significant economy will now use economic warfare to attain its goals. To protect your wealth in this new era of unceasing economic warfare, you need to – as we have done over the past few years – very consciously and very deliberately build a globally diversified multi-asset portfolio.

Source: Amazon

In 1958, the Nobel prize winning economist, Thomas Schelling defined economic warfare as “economic means by which damage is imposed on other countries or the threat of damage used to bring pressure on them.”

As Iran faces off with America and Israel in the Middle East, it has cleverly used a geopolitical form of tolling on the Straits of Hormuz to ensure that other powerful countries like China and India exert pressure on America to end the conflict.

However, for all the drama around it, Iran’s use of Hormuz is neither the most graphic demonstration of the use of chokepoints nor the most impactful in recent years. That prize belongs to China for its spectacular use of rare earths to make Donald Trump rapidly fall into a line a year or so ago (when Trump was threatening to impose punitive tariffs on China).

However, more powerful than physical chokepoints – like Hormuz or the Suez Canal or the Straits of Bosporus – and even more deeply embedded in the global supply chain than rare earths are three other sets of chokepoints which America firmly controls and which it is likely to use in the remainder of the Trump presidency:

1. Advanced chip manufacturing: The vast majority of the world’s advanced semiconductors are made by TSMC in Taiwan. In order to make these chips, TSMC and every chip manufacturer relies solely on ASML’s advanced extreme ultra-violet lithography machines which cost in excess of $200 mn (per machine). Even though ASML is notionally a Dutch company, the US government is able to exert enormous leverage on it as evidenced by the way the first Trump administration withdrew access to ASML’s equipment for Chinese semiconductor manufacturers. As Ed Fishman describes in his book “Chokepoints” (see pg 301), in 2020, the Trump administration prevented ASML from selling its machines to China’s pre-eminent chip manufacturer, SMIC: “A widely circulated report…illustrated SMIC’s ties to China’s military in considerable detail. A few weeks later, the Commerce Department warned that exports to SMIC carried an “unacceptable risk” of being diverted for military purposes….Among Washington’s biggest concerns was that SMIC would gain access to an ultra-complex chip making machine made by…ASML….No other company made anything like it, and it was essential to produce the most advanced chips. ASML had agreed to the sell the machine to SMIC…Under pressure from the Trump administration, the Dutch government dragged its feet on approving the necessary export license…”

Our job as investors is to ensure that we are invested in the critical chokepoints in the tech hardware ecosystem such that your wealth benefits, rather than suffers, from these chokepoints.

2. Ubiquitous software platforms: Microsoft’s Windows operating system for PCs and enterprises and Alphabet’s Android operating system for mobile phones dominate their respective global markets. Both of these are US-listed companies, and the Americans have shown that they are capable of yanking away such operating systems from countries and companies which they don’t like.

In 2019, the Trump administration wanted to squeeze the Chinese company, Huawei, whose cheap smartphones were in high demand around the world. Huawei’s phones ran on Android. As Ed Fishman describes in his book “Chokepoints” (see pg 275), Alphabet’s decision to abandon Huawei in 2019 meant that Huawei smartphone users across the world lost access to Google Play store and to Google products such as Gmail and YouTube. “Existing users of Huawei’s phones would eventually stop receiving software updates” from Google.

Our job as investors is to ensure that we are invested in these dominant operating systems such that your wealth benefits, rather than suffers, from this chokepoint.

3. $-based global payment system: The extent to which the global financial system is utterly dependent on the US$ and the US government is a subject of much misunderstanding in India (ironically, courtesy the nonsense which is spread on this subject using social media platforms owned by American companies). To understand the extent of American dominance of the global financial system consider a simple transaction that takes place almost daily in India (and is replicated in many other countries).

Consider an Indian oil marketing company (OMC) which has to buy crude from Saudi Arabia’s Aramco. To pay for the oil, the Indian OMC has to wire $ to Aramco’s bank account because Aramco will not accept any other currency as payment. Now, since the OMC’s bank – say State Bank of India – is unlikely to have an account with Aramco’s bank, this $ payment will have to go through one of the big banks in New York City, say JP Morgan, which would debit the payment from the OMC’s SBI account and credit it to Aramco’s bank.

For this JP Morgan facilitated payment to be successful, it will have to go through one of America’s two main payment system – CHIPS or Fedwire. And if the US government decided that either the Indian OMC or SBI or Aramco or Aramco’s bank was an entity that it has a problem with, the payment would be blocked! This chokepoint allows the US government to control 85% of the cross-border transactions conducted on this planet. Our job as investors is to ensure that we are invested in the piping of the US financial system so that your wealth benefits, rather than suffers, from this chokepoint.

Investment implications for you

Having seen what Trump did in his first term and having seen Joe Biden eject Russia from the global payment system (SWIFT), four years ago we decided to consciously build a global portfolio which benefits from chokepoints.

While our global portfolio does not guard us against every single chokepoint (e.g. we are exposed if China decides not to export rare earths to the rest of the world), our Global Compounders Portfolio – which focuses on 35-40 high quality companies chosen from stock markets in Taiwan, Germany, Sweden, Holland, France, Canada and America – is far better placed to deal with the new era of economic warfare than a single country portfolio.

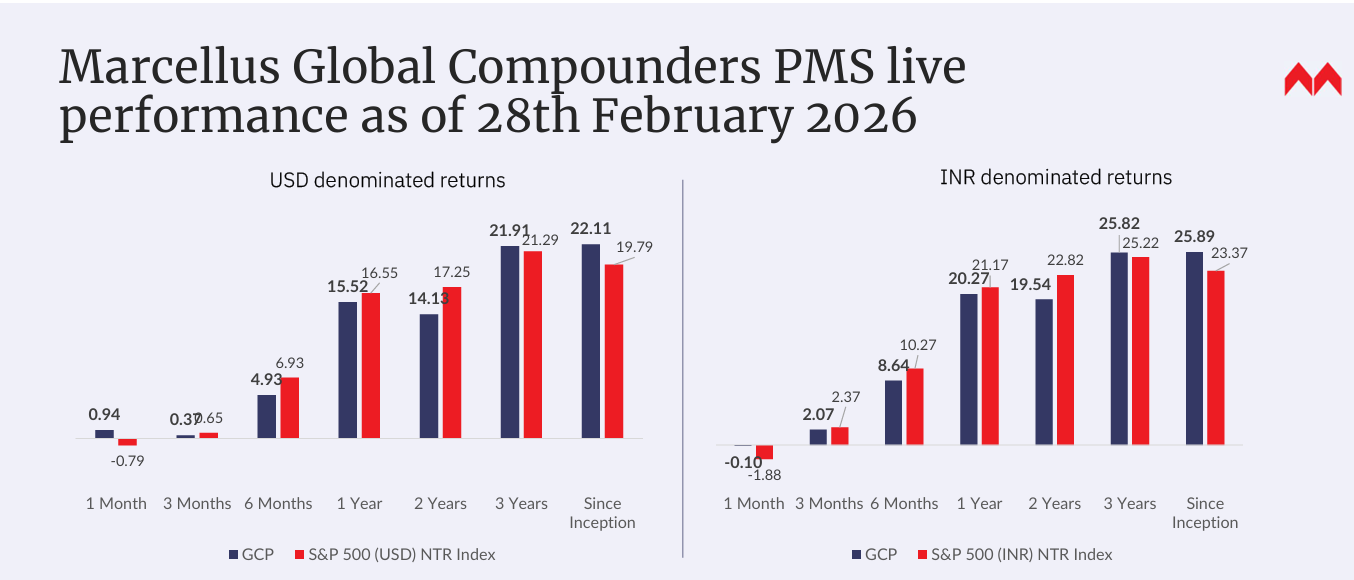

Thanks to the regulatory reforms expedited by the Indian authorities over the past couple of years (see my 7th Jan blog: https://marcellus.in/blogs/four-mega-reforms-which-opened-up-global-investing-for-indians/), you now able to diversify globally in a cost-efficient and tax-efficient manner thereby benefitting from this new age of rage. Our track record in compounding across the world is shown below. Since inception in Oct 2022, the strategy has delivered at ~26% CAGR (net of all fees & expenses in INR).

If you would like more information about our global strategy, please reach out to us.

Note: Marcellus performance data is shown gross of taxes and net of fees & expenses charged till end of last month on client account. Performance fees are charged annually in December. Returns more than 1-year are annualized. Marcellus’ GCP USD returns are converted into INR using USD: INR exchange rate from RBI – Link for the reference

Note: * Since Inception performance calculated from 31st Oct 2022. The inception date is 31st Oct 2022, being the next business day after the account got funded on 28th October 2022. S&P 500 net total return is calculated by considering both capital appreciation and dividend payouts. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the IFSCA or US SEC. Performance is the combined performance of RI and NRI strategies.

Marcellus GCP PMS is offered by Marcellus Investment Managers GIFT Branch in a segregated managed accounts format

The final word on how the age of economic warfare came to pass belongs to bestselling author Ed Fishman and Columbia University professor:

“Historically speaking, ‘chokepoints’ are geographic features like the Strait of Hormuz, which has been in the news in recent months because 20% of global oil flows go through a narrow strait. And throughout history, controlling these geographic chokepoints has given countries and empires really immense power…What happened in the wake of hyper globalization, when countries like China, Russia…entered the global economy, into the dollar-based financial system, into global supply chains, we saw the creation of what I call ‘invisible chokepoints,’ like the dollar-based financial system, which are parts of the global economy where one country has a dominant position and there are few, if any, substitutes. And so when you think about something like the dollar or advanced semiconductor technology, where the U.S. government really can control other countries’ access to it, we actually have similar economic power that empires of old had by controlling geographic chokepoints, just by controlling these key elements of the globalized economy. And it’s what’s given the U.S. government, in particular, really significant power to impose really devastating economic harm on foreign countries. What I would note, though, is that other countries do control some chokepoints. China, as we’ ve seen in recent months with rare earth minerals, also has this power. But really, in recent years, it has been the U.S. that has really pioneered this new style of economic warfare.” – Edward Fishman .

Thanks

Saurabh Mukherjea

The stocks TSMC, ASML, Microsoft, Alphabet and JP MORGAN CHASE & CO are part of the Global Compounders Strategy managed from GIFT City by Marcellus and regulated by IFSCA. Marcellus, its employees, their relatives, and clients have an interest in these stocks.

This material is for informational purposes only and does not constitute investment research or advice. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the IFSCA as a Fund Management Entity – Retail and is also registered with the U.S. SEC as an Investment Adviser. The contents, including any performance information, are not verified by IFSCA or the U.S. SEC. Past performance is not indicative of future results. Investments involve risk, including loss of principal. Recipients should seek independent legal, tax, and investment advice.