OVERVIEW

POPULAR ARTICLES

Nearly four years since the launch of ChatGPT, what has AI done to middle class jobs and incomes in the West? Our literature survey (using AI) suggests: 1) Middle class white collar jobs – especially entry level jobs – have collapsed in the West; 2) Most middle class white collar jobs in the West are seeing wage stagnation or displacement but AI-complementary elite white collar workers are earning a 56% wage premium; and 3) The owners of capital are clear beneficiaries of AI because it is allowing their businesses to become more productive. It will be very surprising if AI does not have a similar effect on the white collar job market in India.

“The more intelligent technology we invent, the more your intelligence matters,” said Chris Pissarides, a Nobel Prize-winning professor of economics at the London School of Economics who has studied the effects of automation on jobs. “When the technology we invented was simpler, your IQ didn’t matter very much. But now it matters more and more with these more advanced technologies.” [1]

[1]The Financial Times, 23rd Apr 2026( https://www.ft.com/content/0873e3cb-cb02-4b47-941f-14da74149670 )

Welcome to Polarisation II

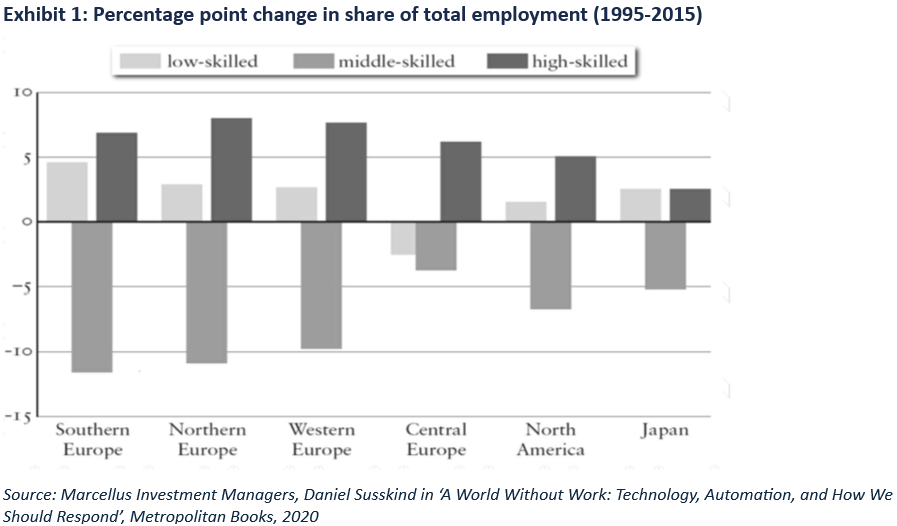

20 years before ChatGPT was launched in 2002, three American economists – Autor, Murnane & Levy – showed that middle class jobs were being lost in Western economies as automation and robotisation in factories took away the need for the machine supervisors, the mechanics and the clerks. Their bosses (the CEOs) were increasingly well-paid and less-skilled workers at the bottom of the period e.g. janitors, labourers, waiters, etc were also required but those in the middle were increasingly redundant. Autor, Murnane & Levy dubbed this phenomenon “polarisation” – see chart above. Post-2022 as AI has spread across every aspect of life & work in the developed economies. AI is leading to another round of polarisation; this time the middle class jobs are being lost in the offices rather than in the factories.

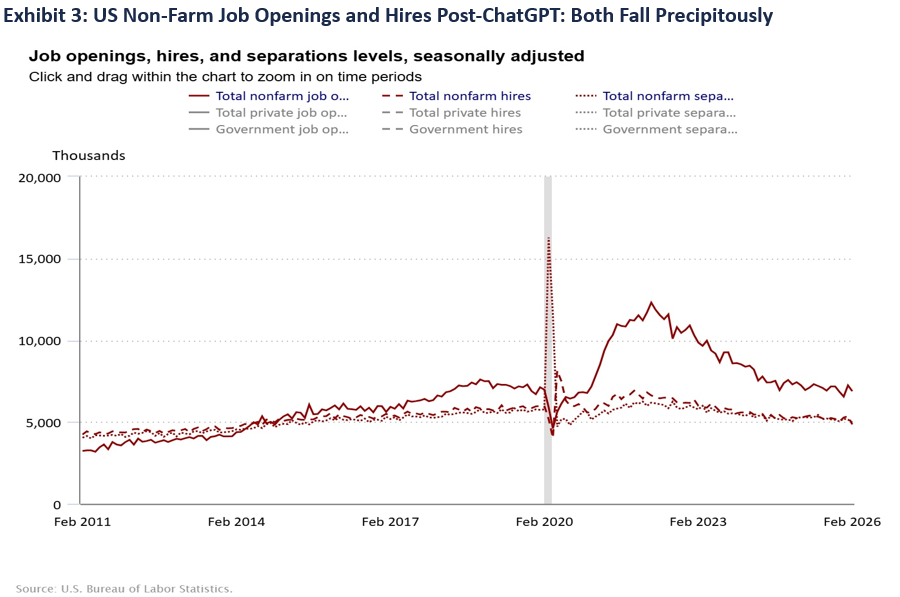

In fact, if we were to look at US Bureau of Labor Statistics data, the picture becomes quite clear: in 2023 (after ChatGPT’s launch) both the openings and hiring in non-farm jobs fell precipitously (see Exhibit 3 below).

Source: Marcellus Investment Managers, US Bureau of Labor Statistics — Job Openings and Labor Turnover Survey (JOLTS), https://www.bls.gov/jlt/

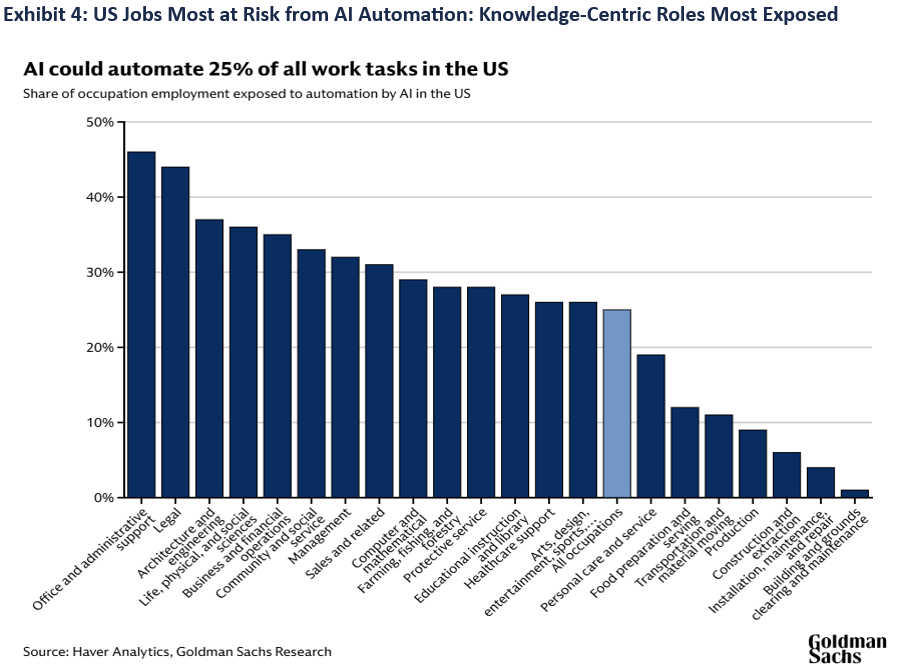

More importantly, Goldman Sachs in one of their articles detailed which sectors and jobs are at most risk due to AI rendering their skills useless — and most of these turned out to be knowledge-centric, the bastion of the middle class, whereas those at the lower end of the skill spectrum are less likely to be displaced (see Exhibit 4 below). All in all, in the US, AI has the potential to automate tasks that account for 25% of all work hours.

Source: Marcellus Investment Managers, Goldman Sachs — How Will AI Affect the US Labor Market? https://www.goldmansachs.com/insights/articles/how-will-ai-affect-the-us-labor-market

Wealth and Income Disparity Rises with AI Adoption

The discussion on wages is more nuanced than the one on jobs, because here it is not just skill of the employee in question but also their productivity and complementarity of the occupation with AI.

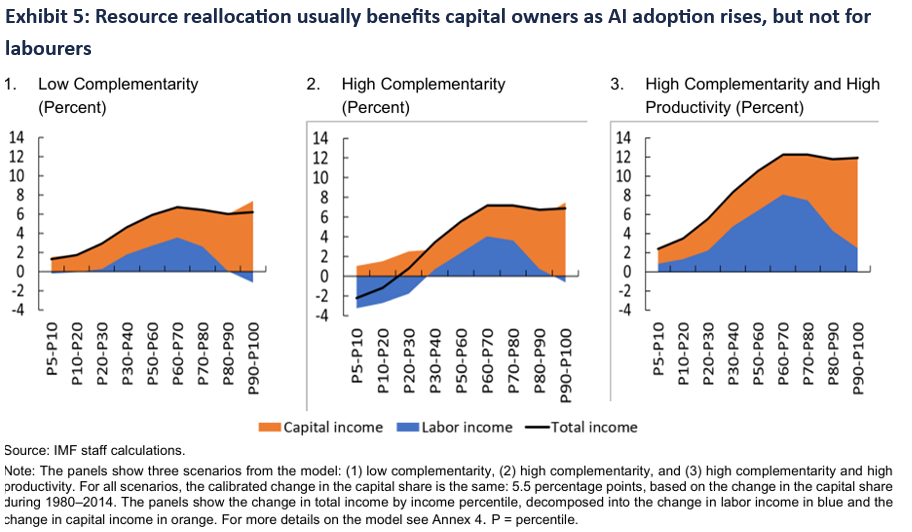

According to the IMF, when complementarity of AI with labour is lower, capital productivity improvement occurs and income inequality reduces as the displacement effect is larger than complementarity gains, affecting the labour negatively (everyone is worse off).

When there is high complementarity of labour with AI, the share of labour at the upper income spectrum getting negatively impacted reduces (as they augment their work with AI), and simultaneously because those at the lower end see their incomes getting negatively impacted because they don’t enjoy the high complementarity and get displaced due to AI. This leads to a widening of income inequality where a few at the upper end of the complementarity and income spectrum. When productivity is also considered, however, the gains from AI are enjoyed by everyone across the spectrum although those at the higher end benefit disproportionately more.

In all scenarios, rising AI adoption helps capital deepening and income generated thereof, i.e., for owners of capital AI adoption is a net positive (see exhibit below).

Whilst the authors Cazzaniga M. et al did this analysis in the context of a single country seeing these changes within, they also mentioned that this could be true between countries where resource reallocation occurs between two countries, from lesser developed regions to those more technologically advanced and AI-ready. Case in point is the redundancy of call centres in India, to be replaced by automatic bots (powered by American LLMs) answering customer phone calls.

Sources: Marcellus Investment Managers, IMF (sdnea2024001.pdf)

The relationship between AI and labour is profoundly non-linear. Capital owners are the unconditional beneficiaries regardless of the economic cycle. For labour, the outcomes bifurcate sharply. Those with skills that complement AI command a 56% wage premium over peers in the same role without AI skill. [2]

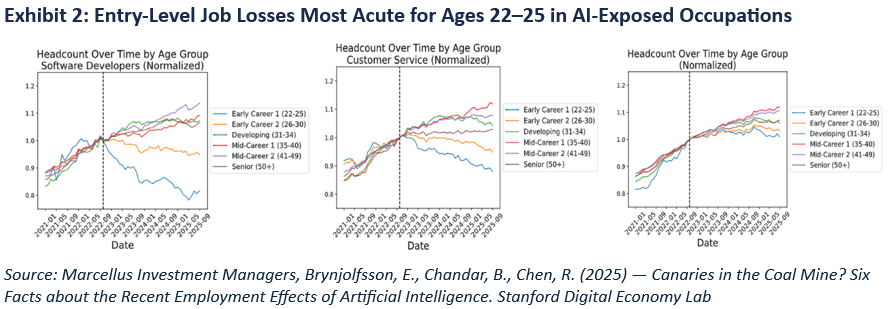

The lowest-skilled workers in physical, in-person, dexterous roles are, paradoxically, somewhat insulated: AI cannot yet care for the elderly, rewire a building, or perform surgery. It is the middle-skilled worker — the paralegal, the junior data analyst, the mid-level coder, the customer support agent — who finds their value proposition quietly and relentlessly eroded.

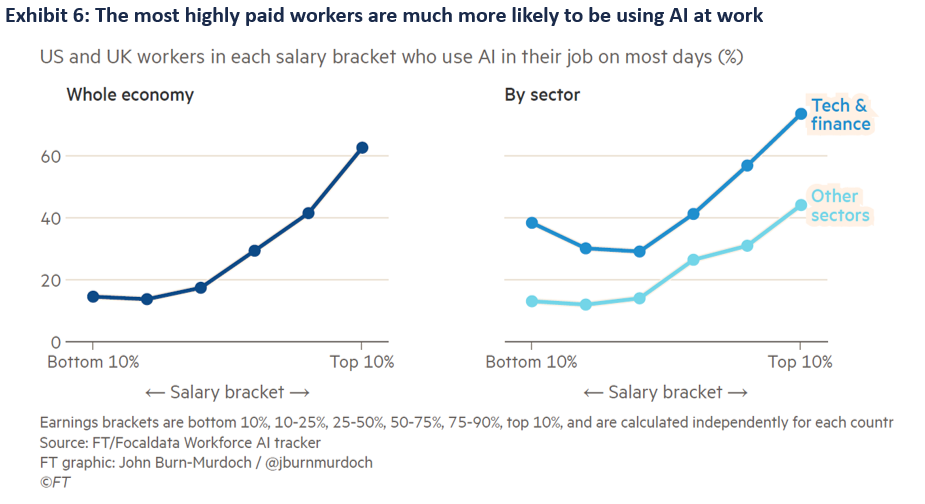

Another way to rationalise what is happening in the West is that the best paid white collar workers are using AI the most to improve their productivity and performance. “An FT poll of 4,000 workers in the US and UK shows adoption is heavily skewed towards the best paid workers: more than 60 per cent use AI daily, compared with just 16 per cent of the lower earners.” [3]

Nobel Laureate Daron Acemoglu, who teaches Economics at MIT, explains in plain English what AI is doing to the Western middle class: “The rhetoric out there is that the tools are going to be democratising. But the reality is that . . . you require a certain degree of education, abstract and quantitative skills, familiarity with computers and coding in order to be using the models…AI is going to increase inequality between labour and capital. That is almost for sure. I would say it is setting us up for a . . . shitshow.” [4]

[4] https://www.ft.com/content/0873e3cb-cb02-4b47-941f-14da74149670

Source: Marcellus Investment Managers, Financial Times (https://www.ft.com/content/0873e3cb-cb02-4b47-941f-14da74149670)

Where Does India Stand?

India’s exposure to AI-driven disruption is structurally acute. The country’s middle-class economic ascent has been built almost entirely on white-collar services employment — IT services, business process management, and financial back-office work. These are precisely the sectors generative AI is targeting first. NITI Aayog’s October 2025 roadmap frames the stakes starkly:

“In the worst-case scenario, IT services headcount could fall from 7.5–8 million in 2023 to 6 million by 2031. Similarly, the CX sector headcount could fall from 2–2.5 million to 1.8 million.”

— NITI Aayog — Roadmap for Job Creation in the AI Economy, October 2025

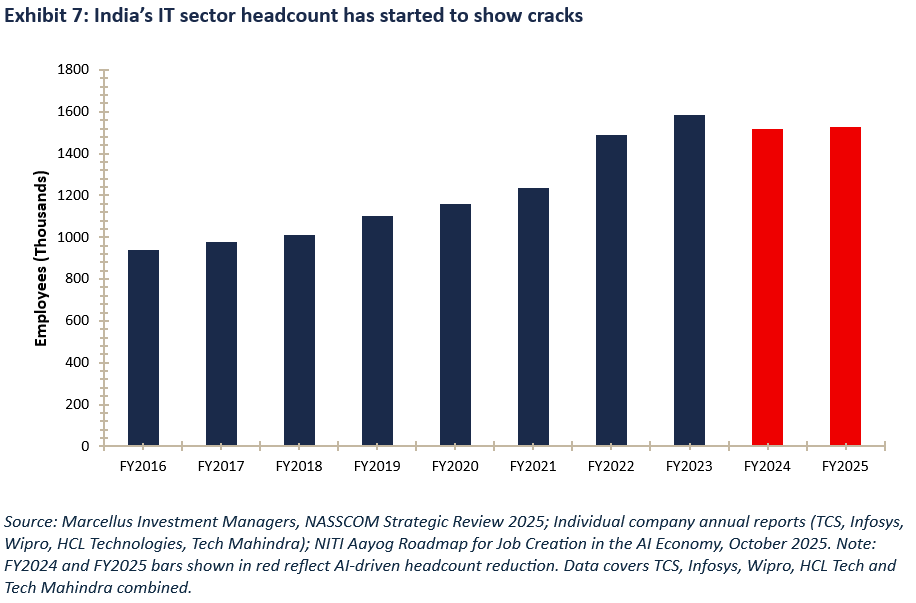

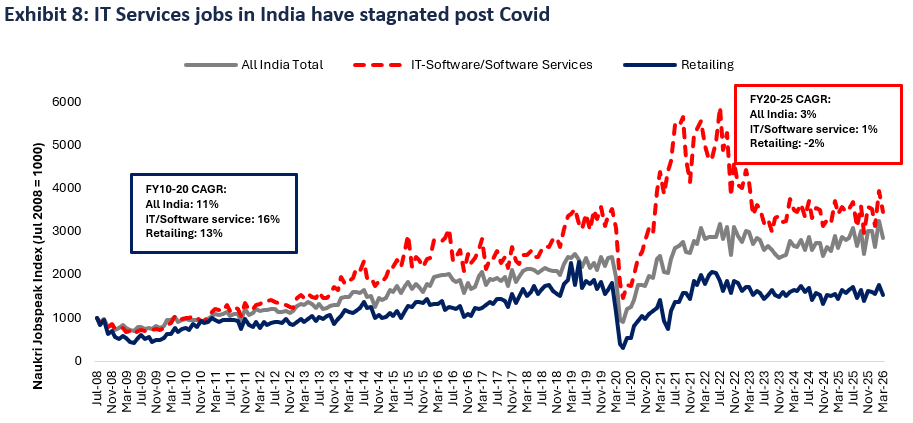

These vulnerabilities are not merely based on narratives – widespread national surveys have now started picking up these trends too. The IT sector’s hiring crisis is most visible at the entry level, where both volumes and wages have deteriorated sharply. Over 50,000 job cuts were recorded in India’s IT industry in 2024 alone, disproportionately affecting entry-level programmers and software testers – roles directly in the path of generative AI automation. Data from Naukri, India’s largest provider of employment classifieds, shows that growth in white collar jobs has been close to ZERO over the past 3 years – see chart below.

Source: Marcellus Investment Manager, Naukri Jobspeak Index (https://www.infoedge.in/InvestorRelations/NaukriJobSpeak)

Entry level salaries have barely moved from Rs. 3.5 lakhs per annum to Rs. 3.8 lakhs between 2015 to 2024 and the intent to hire freshers was 14% in 2025, down from 18.8% in 2024 (source: TeamLease/Outlook Business (2025): India’s Middle Class is the Biggest Loser in the AI Economy and India Skills Report 2025).

The disruption, however, is not uniformly negative. India has several advantages that could help it position as a key beneficiary rather than victim of the AI transition.

Thirty percent of Indian enterprises have adopted AI tools, ahead of the global average of 26%, and India ranks first globally in AI skill penetration according to NASSCOM. Approximately, 1.25 million AI professionals will be needed in India by 2027, up from 600-650K in 2022, a near doubling in 5 years. Workers who successfully navigate from traditional IT delivery roles to AI-native roles stand to benefit from both, a large domestic opportunity and India’s existing cost advantage in the global technology services delivery. [5]

[5]Deloitte-NASSCOM 2024. Advancing India’s AI Skills: Interventions needed. NASSCOM AI Enterprise Adoption Index 2.0, 2024, nasscom.in

Investment Implications

Much like in the West — where a hollowing out of middle-skill and typical middle-class, white-collar jobs began with ChatGPT’s arrival — we are staring at a similar disruption in India, perhaps at a greater scale given that India has typically been the back-office of western companies, precisely the jobs which are at risk of automation.

Having said that, with the right kind of skilling and identifying opportunities in sectors likely to benefit from AI will be key to success going forward. But most importantly, taking charge of your own work and augmenting it using AI will become a must rather than just a choice. This is the new middle class elite — ones who create work for themselves rather than working for someone else — much as we have explained in our latest bestselling book, “Breakpoint: The Crisis of the Middle Class and the Future of Work” (2026).

As India heads into a more uncertain job-market environment, our research shows that households need to pare down debts and save more to cope with the new realities. As with everything else in life, this is achievable if properly planned. Our colleagues at Marcellus offer our clients a free financial plan. To avail of this, please visit plan.marcellus.in OR scan the QR code shown below into your mobile phone.

Note: This tool provides guidance on asset allocation and does not constitute a financial plan or investment advice.

Saurabh Mukherjea and Nandita Rajhansa work for Marcellus Investment Managers (www.marcellus.in ). The views and opinions expressed in this material are those of the writers/authors and do not necessarily reflect the official policy. This material is for informational and educational purposes only and should not be considered as financial, investment, or other professional advice. The inclusion of any book does not imply endorsement or recommendation by the writers or the publisher of this material.

Disclaimer:

The above material is neither investment research, nor investment advice. HCL Tech and Info Edge form part of Marcellus’ portfolios. References to financial planning relate only to asset allocation under Marcellus’ PMS license. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. All recipients of this material must before dealing and or transacting in any of the products and services referred to in this material must make their own investigation, seek appropriate professional advice. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer, or an employee. This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.