OVERVIEW

POPULAR ARTICLES

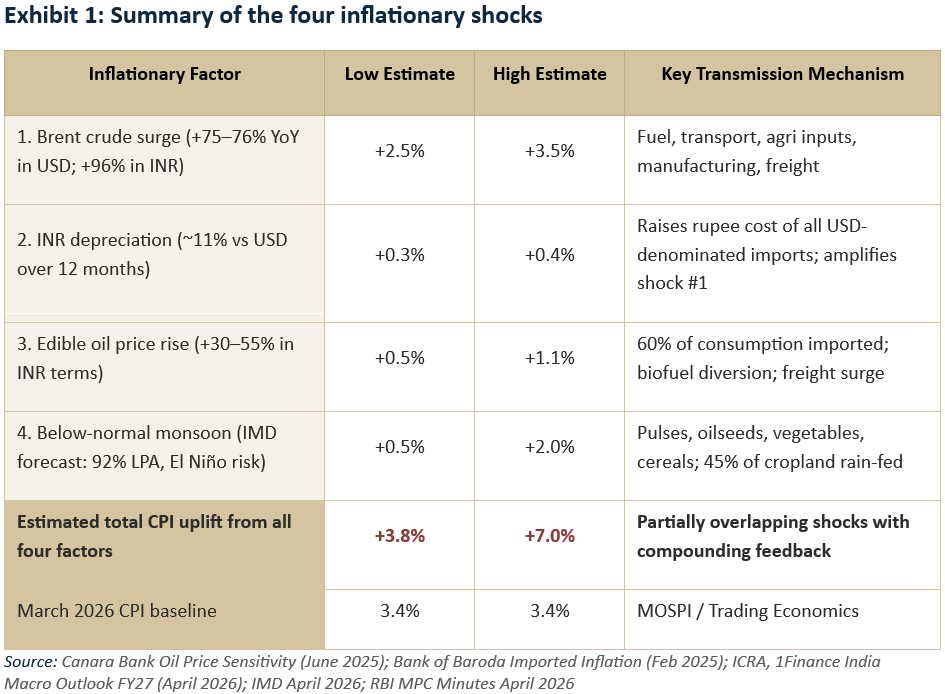

While the rising price of Brent crude features prominently in media reports, there are 3 other less reported inflationary shocks moving towards the Indian economy – the rising cost of imports, the soaring cost of edible oils and the likelihood of a poor monsoon – which are capable of delivering a punch as powerful as crude oil. Cumulatively, these 4 inflationary shocks are capable of pushing up India’s CPI inflation by around 4% points (even assuming very benign second round impacts). That in turn would trigger rate hikes from the RBI of at least 1.5-2% with serious consequences for the Indian middle class due to its status as one of the indebted groups of people in the world.

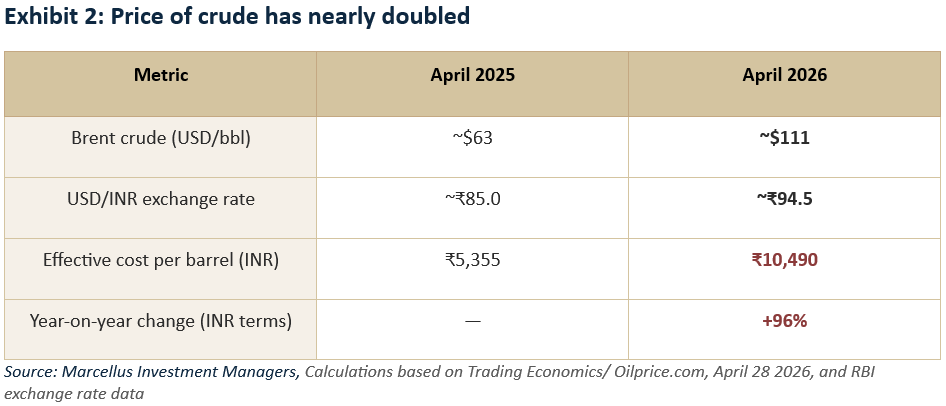

Inflationary Shock #1: Brent crude has doubled in price in INR terms

Most investors seem to believe that the price of crude oil has risen by around 50% from $70 before the Iran War to around $110 after the onset of the war. This rudimentary calculation significantly underestimates the jump in crude oil price shock that India is experiencing due to the Iran War. As shown in the table below, the price of crude has nearly doubled YOY when measured in INR terms.

The impact of crude oil on India’s CPI operates through two distinct channels:

Direct channel: Petrol, diesel, LPG and kerosene prices. The fuel & light basket carries a weight of around 7% in India’s CPI. With a pass-through rate of approximately 30–40% (reflecting partial government price management), a 40–75% crude rise directly contributes 1.2–1.5% to a jump in CPI inflation.

Indirect channel: Diesel powers agricultural irrigation pumps, tractors, and freight transport. When diesel prices rise, the cost of moving food from farm to market rises, feeding into the 46% food component of the CPI basket.

Inflationary Shock #2: The rupee’s 11% slide against the US$

The Indian Rupee has depreciated approximately 11% against the US Dollar over the past 12 months, falling from ~ ₹85/$ to ~₹94.5/$ as of April 28, 2026. This represents the steepest annual fall since FY12.

India’s CPI pass-through from currency depreciation is structurally lower than many comparable emerging markets because the CPI basket is heavily skewed toward domestically produced food (approximately 46% of total weight). However, the impact is concentrated and meaningful in specific sub-categories.

Bank of Baroda’s quantitative analysis (December 2025) estimates that a 10% INR depreciation raises CPI by 30–35 basis points (0.30–0.35%). For the ~11% depreciation observed, the direct CPI impact is therefore approximately 0.33–0.38%.[i]

Inflationary Shock #3: The 40% jump in the price of edible oil

India is the world’s largest importer of edible oils, relying on imports for approximately 60% of its domestic consumption requirements. Domestic production of roughly 9.6 million tonnes in 2025–26 falls well short of estimated consumption, necessitating imports of approximately 16.5 million tonnes. The import basket is dominated by palm oil (~45–55%), soybean oil (~20–23%), and sunflower oil (~8–22%), sourced primarily from Malaysia, Indonesia, Ukraine, Russia, and Argentina. [ii]

Over the past 6 months, global edible oil prices have risen by 40-50% in INR terms.[iii] Oils and fats carry a weight of around 3% in urban CPI. A 40–55% rise in the price edible oil therefore translates into 1-1.5% jump in CPI inflation.

Inflationary Shock #4: El Nino and the risk of a poor monsoon

The India Meteorological Department (IMD) has forecast the 2026 southwest monsoon at 92% of the Long Period Average (LPA), classifying it as ‘below normal’ — the first such forecast in three years. The forecast carries a model error margin of ±5 percentage points. Critically, there is a 35% probability of a fully ‘deficient’ monsoon (below 90% of LPA). El Niño conditions are expected to develop between June and September 2026, historically weakening Indian monsoons in 7 out of every 10 occurrences. [iv]

The economic significance of the monsoon extends far beyond agriculture because 45% of India’s net sown area is rain-fed with no irrigation cover and food items account for around half of the CPI basket.[v]

In 2014–15 and 2015–16, when the monsoon fell below 90% of normal, kharif crop production declined materially. Food inflation in those years contributed significantly to CPI breaching the RBI’s 6% upper tolerance band.

ICRA has projected that CPI inflation for FY2027 could exceed 4.5% on the monsoon shock alone. In a deficient scenario (below 90% of LPA), the contribution to headline CPI is estimated at 1.0–2.0% given the food basket’s weight.

A mitigating factor is that reservoir storage levels entering the 2026 kharif season are at 127% of normal — an above-average buffer that can support irrigation and partially offset rainfall shortfalls in key agricultural states.[vi]

Investment Implications

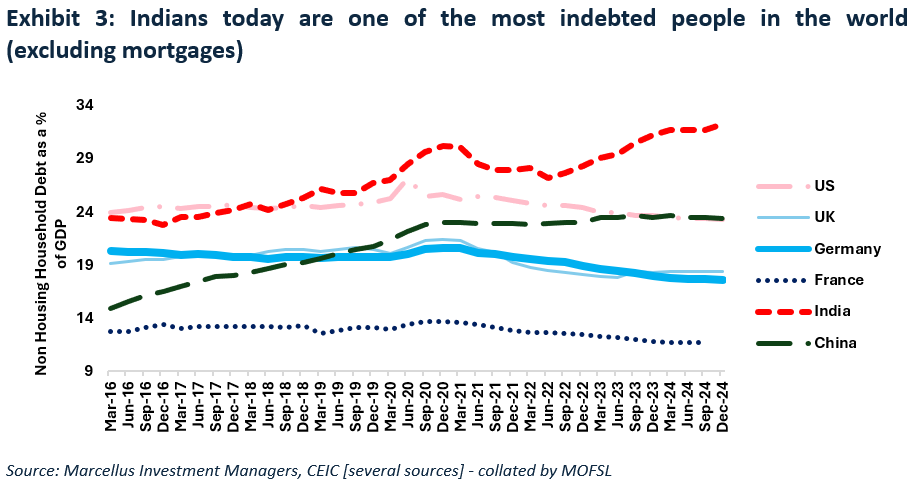

We have highlighted in our bestselling book, “Breakpoint: The Crisis of the Middle Class” that the Indian middle class is: a) more indebted today than it has ever been; and b) among the most indebted groups of people anywhere in the world – see chart below

As India heads into a more uncertain job-market environment (see our blogs dated 9th March 2026 and 27th April 2026 ) amid rising CPI inflation, our research shows that households need to pare down debts and save more to cope with the new realities. As with everything else in life, this is achievable if properly planned. Our colleagues at Marcellus offer our clients a free asset allocation plan. To avail of this, please visit plan.marcellus.in OR scan the QR code shown below into your mobile phone.

Note: This tool provides guidance on asset allocation and does not constitute a financial plan or investment advice.

[i] Source: Bank of Baroda: ‘Imported Inflation: Myth or Reality?’, February 2025; ANI/Bank of Baroda report, December 2025

[ii] Source: IVPA (Indian Vegetable Oil Producers’ Association), Black Sea Grain Conference, Kyiv, April 2026; Global Agriculture, April 2026

[iii] Source: IVPA / Asianet Newsable, April 2026; Whalesbook Energy Costs & Edible Oil Report, March 2026; FAO Vegetable Oil Price Index, January 2026.

[iv] Source: IMD Southwest Monsoon Forecast, April 13 2026; Outlook Business, April 2026; BusinessToday, April 21 2026

[v] Source: Policy Circle — Below-Normal Monsoon India 2026, April 2026; BusinessToday, April 21 2026

[vi] Source: RBI MPC Minutes, April 2026; ICRA as cited in BusinessToday; Ministry of Agriculture reservoir data

Saurabh Mukherjea and Nandita Rajhansa work for Marcellus Investment Managers (www.marcellus.in ). The views and opinions expressed in this material are those of the writers/authors and do not necessarily reflect the official policy. This material is for informational and educational purposes only and should not be considered as financial, investment, or other professional advice. The inclusion of any book does not imply endorsement or recommendation by the writers or the publisher of this material.

Disclaimer:

The above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. All recipients of this material must before dealing and or transacting in any of the products and services referred to in this material must make their own investigation, seek appropriate professional advice. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer, or an employee. This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.