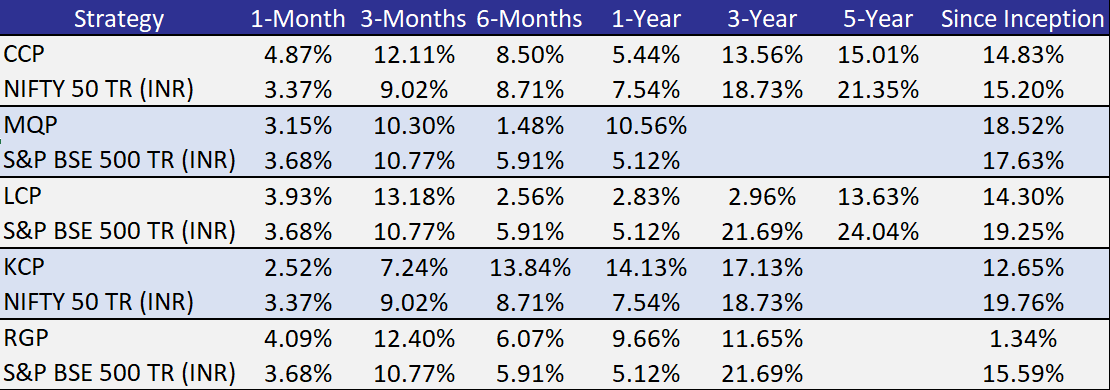

Performance Snapshot vis-à-vis Respective Benchmarks (figures in %)

As of 31st May 2025

Disclaimer:

The Benchmark for Consistent Compounders & Kings of Capital is Nifty 50 Total Return Index, and for Little Champs, MeritorQ PMS & Rising Giants is BSE 500 Total Return Index

For relative performance of particular Investment Approach to other Portfolio Managers within the selected strategy, please refer to https://www.apmiindia.org/apmi/WSIAConsolidateReport.htm?action=showReportMenu. Under PMS Provider Name please select Marcellus Investment Managers Private Limited and select your Investment Approach Name for viewing the stated disclosure. Performance data shown is net of fixed fees and expenses charged till March 31st, 2025 and is net of annual performance fees (Except for Little Champs Portfolio) charged for client accounts whose account anniversary/performance calculation date falls upto the last date of this performance period. Since, for Little Champs Portfolio, performances fees are charged on cumulative gains at the third anniversary, of the respective client account, the effect of the same has been incorporated for client accounts whose third account anniversary falls upto the last date of this performance period. Performance data is not verified either by Securities and Exchange Board of India or U.S. Securities and Exchange Commission.