This month we delve deeper into Godrej Agrovet Limited (GAVL) which we added to the Little Champs portfolio earlier this year. GAVL is a diversified agri-focussed company present across animal feed, palm oil, crop protection, dairy and poultry businesses. The Company witnessed muted earnings growth over FY18-23 due to volatility in commodity prices (inputs as well as finished products). However, we expect much better earnings growth henceforth driven by the GAVL’s focus on building out value added portfolios across business segments and favourable government policies for farmers such as the ‘National Mission on Edibile Oils – Oil Palms’. Succession around the current Managing Director and near-term Government actions to manage commodity price volatilities are the key risks to our earnings estimates.

Performance update for the Little Champs Portfolio

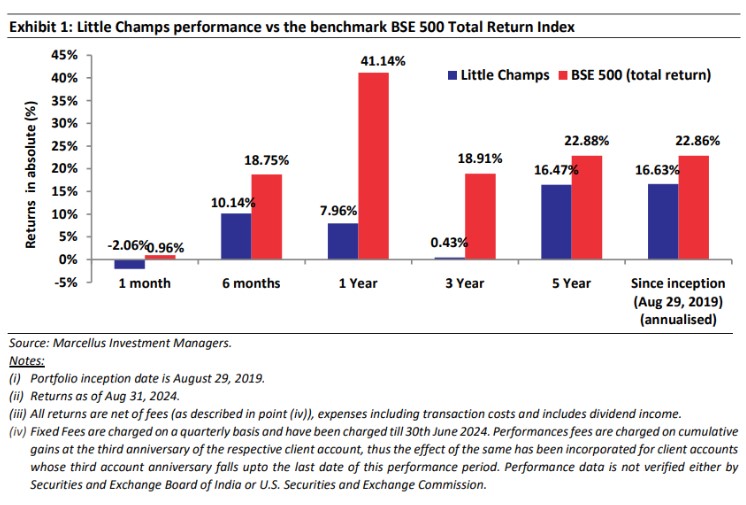

The Little Champs Portfolio went live on August 29, 2019. The performance so far is shown in the below table.

*For relative performance of particular Investment Approach to other Portfolio Managers within the selected strategy, please refer the following link https://www.apmiindia.org/apmi/welcomeiaperformance.htm?action=PMSmenu . Under PMS Provider please select Marcellus Investment Managers Private Limited & select your Investment Approach Name for viewing the stated disclosure.

Significant new additions to the Little Champs portfolio in the last twelve months

Since October 2023, we have added 18 new stocks to the Little Champs portfolio (until August 31, 2024). The brief rationales for all the additions/deletions have been shared with you in the monthly portfolio updates. In this LCP newsletter, we delve deeper into our reasons for adding Godrej Agrovet Limited in the portfolio.

Why we invested in Godrej Agrovet?

Background: A diversified agri-focussed company

Godrej Agrovet Limited (GAVL), with a focus on building agricultural business, was incorporated in 1991. The business kickstarted with the acquisition of the animal feed and crop protection businesses (agrovet division) from Godrej Soaps Limited (later demerged into Godrej Industries Limited and Godrej Consumer Products Limited). Over the years, the Company forayed into many new businesses – prominent amongst them being:

- Palm oil (acquired again from Godrej Soaps Limited in 1997);

- Poultry (forayed in 1994 through the Real Good chicken brand and subsequent JV with Tyson in 2008);

- Dairy through the acquisition of a 26% stake in Creamline Dairy in 2005 (increased to 51.9% since 2015); and

- Acquisition of a 52.3% stake in Astec Lifesciences in 2015 (increased to 64.8% now).

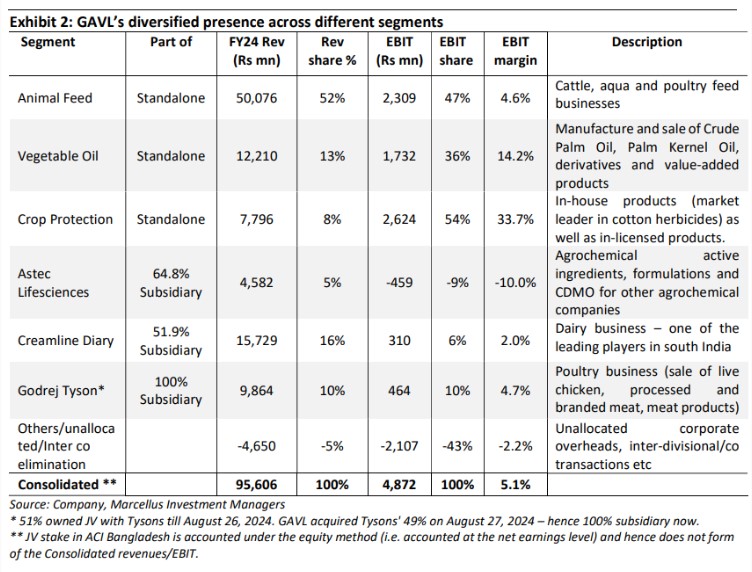

As of today, GAVL’s corporate structure with key segmental contribution stood as below:

What ailed the business over FY18-23?

By 2017, all of the above business segments were in place and the Consolidated EPS had compounded at a healthy 16% CAGR over the preceding five years (FY12-17). In October 2017, the Company went public combining a primary raise of Rs. 2,915 mn, alongside secondary sale of shares by promoters.

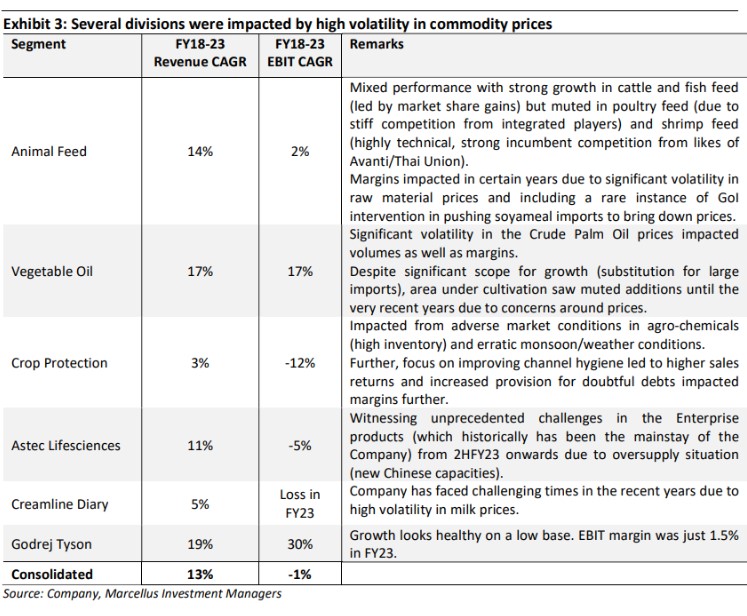

However, unlike the pre-listing era, the Company’s net earnings stagnated over FY18-23. Several of firm’s businesses witnessed cyclical issues (volatility in input/finished prices and the impact on demand/margins thereof) – explained in the below exhibit.

A. Healthy RoCEs, cash generation and balance sheet:

i. While Company deals in many agri-commodities which by definition have a low margin, many of the divisions enjoy asset light models – on both working capital and fixed assets fronts – which means strong RoCE generation. The Company’s pre-tax RoCE averaged 19% over FY19-23.

ii. Cumulative positive FCF generation of close to Rs 500 crores over FY19-23.

iii. Net debt-equity as at FY23-end stood at a comfortable 0.3x.

Despite being at the negative end of the business cycle through most of these 5 years, healthy RoCE, positive FCF generation and declining net debt levels prompted us to look deeper into the Company.

B. Greenshoots of revival in earnings:

i. After having a weak FY23, we started seeing signs of an earnings pick from June 2023 quarter onwards. For the first three quarters of FY24, EBIT was up 27% – this was indicative of things turning around for the Company.

It also helped that stock price was trading at an undemanding 29x trailing twelve months net earnings.

Our reasons for looking at the Company despite weak historical fundamentals?

Similarly, driven by weak fundamentals, the Company’s share price had stagnated around Rs550 by December 2023; returning less than 3% CAGR relative to the IPO issue price (Rs. 460) about six years ago. Against this backdrop, we started researching GAVL during the early part of this calendar year. What aroused our interest in this company were:

A. Healthy RoCEs, cash generation and balance sheet:

i. While Company deals in many agri-commodities which by definition have a low margin, many of the divisions enjoy asset light models – on both working capital and fixed assets fronts – which means strong RoCE generation. The Company’s pre-tax RoCE averaged 19% over FY19-23.

ii. Cumulative positive FCF generation of close to Rs 500 crores over FY19-23.

iii. Net debt-equity as at FY23-end stood at a comfortable 0.3x.

Despite being at the negative end of the business cycle through most of these 5 years, healthy RoCE, positive FCF generation and declining net debt levels prompted us to look deeper into the Company.

B. Greenshoots of revival in earnings:

i. After having a weak FY23, we started seeing signs of an earnings pick from June 2023 quarter onwards. For the first three quarters of FY24, EBIT was up 27% – this was indicative of things turning around for the Company.

It also helped that stock price was trading at an undemanding 29x trailing twelve months net earnings.

Focus on value added products, favourable government policies to aid next 3/5 years earnings growth

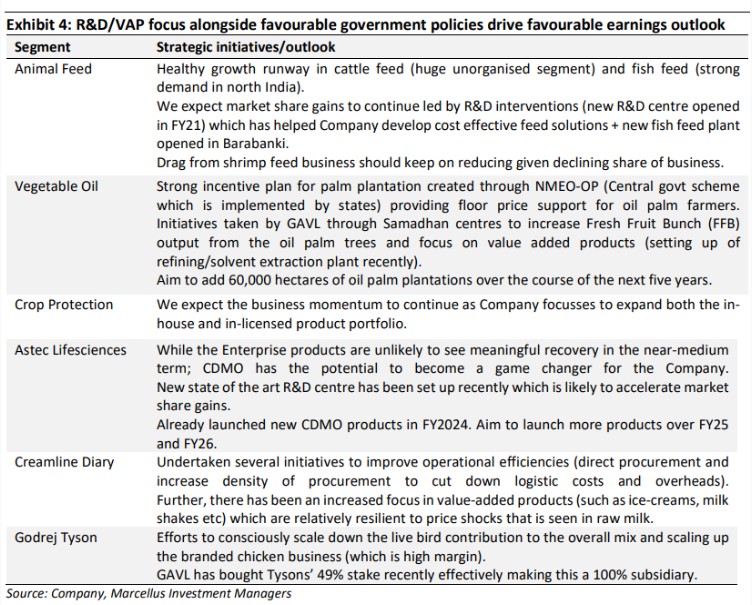

Our research team travelled to GAVL’s various divisions/manufacturing/R&D facilities across the length and breadth of the country, interacted with the channel and primary data sources and came back convinced about the outlook for many of the key divisions for the next 3-5 years.

While Division-wise details are captured in the below table, we see this Company benefiting from the following broad trends:

A. Focus on building out the VAP portfolio across various divisions particularly vegetable oils, dairy and poultry businesses. This is likely to not only help improve the margin profile but also better protect margin during periods of commodity inflation (due to higher pricing power in the VAP portfolio) – a structural improvement compared to the highly commoditized nature of the business historically. This change has been brought upon by conscious R&D efforts made by the Company eg. setting up of R&D centres for the Animal Feed business and for Astec (the CDMO subsidiary) over the last 5 years.

B. Government policies favourably impacting divisions such as vegetable oils and fish feed. We also see macro-tailwinds with increasing Government focus on food, farmers and sustainability.

Key Risks:

A. Government actions/regulations can create significant volatility in near term earnings

While longer term government policies seem to be in favour of the Company, near term Government actions driven particularly by volatility in the commodity prices can create volatility in GAVL’s earnings. Some of the instances of this happening are:

- In August 2021, Government of India (GoI) relaxed rules to allow imports of upto 1.2 mn tonnes of genetically modified soyameal which led to significant inventory loss/margin impact in the animal feed division.

- In response to the volatility in the global crude oil palm prices, the GoI periodically alters the level of import duty (increase in case of weak global CPO prices; reduce in case of high prices) – this significantly impacts the domestic CPO prices and thus the fortunes of GAVL’s vegetable oil division.

B. Succession risks

Mr Balram Singh Yadav has been the Managing Director of the Company since 2007. His current term ends on April 30, 2025. It is not clear to us whether he will continue to be the Managing Director of the Company post the end of this term. While there are CEO/heads in place for all the key divisions, Mr Yadav has been associated with the Company since long (1990) playing a key role in the evolution of the Company and liasoning with the Government. Hence his continuation/succession is a key thing to watch out for.

Regards,

Team Marcellus

Disclaimer: Note: the above material is neither investment research, nor investment advice. Marcellus does not seek payment for or business from this material/email in any shape or form. Marcellus Investment Managers Private Limited (“Marcellus”) is regulated by the Securities and Exchange Board of India (“SEBI”) as a provider of Portfolio Management Services. Marcellus is also a US Securities & Exchange Commission (“US SEC”) registered Investment Advisor. No content of this publication including the performance related information is verified by SEBI or US SEC. If any recipient or reader of this material is based outside India and USA, please note that Marcellus may not be regulated in such jurisdiction and this material is not a solicitation to use Marcellus’s services. All recipients of this material must before dealing and or transacting in any of the products/services referred to in this material must make their own investigation, seek appropriate professional advice. This communication is confidential and privileged and is directed to and for the use of the addressee only. The recipient, if not the addressee, should not use this material if erroneously received, and access and use of this material in any manner by anyone other than the addressee is unauthorized. If you are not the intended recipient, please notify the sender by return email and immediately destroy all copies of this message and any attachments and delete it from your computer system, permanently. No liability whatsoever is assumed by Marcellus as a result of the recipient or any other person relying upon the opinion unless otherwise agreed in writing. The recipient acknowledges that Marcellus may be unable to exercise control or ensure or guarantee the integrity of the text of the material/email message and the text is not warranted as to its completeness and accuracy. The material, names and branding of the investment style do not provide any impression or a claim that these products/strategies achieve the respective objectives. Further, past performance is not indicative of future results. Marcellus and/or its associates, the authors of this material (including their relatives) may have financial interest by way of investments in the companies covered in this material. Marcellus does not receive compensation from the companies for their coverage in this material. Marcellus does not provide any market making service to any company covered in this material. In the past 12 months, Marcellus and its associates have never i) managed or co-managed any public offering of securities; ii) have not offered investment banking or merchant banking or brokerage services; or iii) have received any compensation or other benefits from the company or third party in connection with this coverage. Authors of this material have never served the companies in a capacity of a director, officer or an employee.

This material may contain confidential or proprietary information and user shall take prior written consent from Marcellus before any reproduction in any form.

Regards, Team Marcellus

If you want to read our other published material, please visit https://marcellus.in/pms-investment-blog/

Copyright © 2026 Marcellus Investment Managers Pvt Ltd, All rights reserved