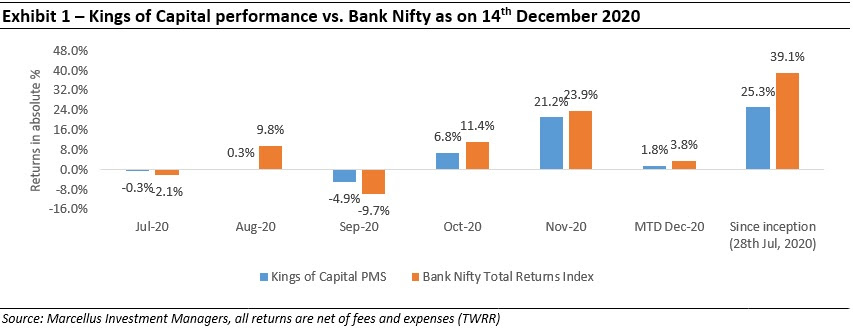

Under the TWRR method of calculating portfolio performance the initial performance looks optically lower in an upward trending market because of large inflows on a relatively small AUM. As on 14th Dec, the first customer of the Kings of Capital PMS had generated returns of 29.7% vs 39.1% for the Bank Nifty since inception.

Marcellus has launched its SIP (Systematic Investment Plan) and STP (Systematic Transfer Plan) offering. Investors now have the option to save and invest regularly in Marcellus Funds. For more details please read our FAQs on STP here and SIP here.

Because the Kings of Capital portfolio is focused on Indian Financial Services stocks, we have received questions around “Won’t the banks and NBFCs in the Kings of Capital portfolio suffer in the coming months as the Covid NPAs will hit the banking industry?” or “Will we not see a further deterioration of the profitability and balance sheet strength of the KCP lenders in the next few quarters?”. We try and answer both of these questions in this newsletter.

For more insights on why bad debts are not rising in the Indian banking system, please watch Marcellus’ 28th October, 2020 webinar on the said subject with RBI’s former Deputy Governor R Gandhi here.

Understanding NPAs, GNPA% and provision coverage ratio and how they impact profitability of lenders

NPAs:

For banks, a non-performing asset is any loan for which interest or principal payment is overdue for a period of 90 days or more. Banks then estimate the amount that can be recovered from a non-performing asset and the balance amount is provided for as an expense on the P&L.

Illustration:

For eg. if a bank has a loan book of Rs. 10,000 and interest or principal repayment is overdue for a period of more than 90 days on a loan of Rs. 100 then the bank’s gross NPA ratio will be 1% (Rs. 100 divided by Rs. 10,000). Further, if the bank believes that Rs. 30 can be recovered then the bank will provide for Rs. 70 i.e. there will be an expense of Rs. 70 on the bank’s P&L for that period. The provision coverage ratio for the bank will be 70% (provision of Rs. 70 divided by GNPAs of Rs. 100). In other words, for the P&L of a bank to get impacted, a loan is usually first classified as a NPA and the bank then provides for the amount it will not be able to recover as an expense on the P&L statement.

Impact of the moratorium, standstill asset classification and Supreme Court verdict

Impact of the moratorium:

As per the moratorium granted by the RBI, all borrowers had the option to not pay their EMIs from 1st March, 2020 to 31st Aug, 2020 and all loans on which EMIs were not paid during this period were not to be classified as NPAs. For eg. if an installment was due on 1st April and was unpaid till 30th June i.e. for a 90-day period, it still won’t be classified as an NPA because it was during the moratorium period.

Impact of standstill asset classification:

In addition to NPAs not being recognized during the six-month moratorium, even those loans which were already overdue before the moratorium period began get the benefit of standstill asset classification. For eg. if a loan was overdue for 1 day on 29th Feb, 2020 and remains unpaid till 31st Aug, 2020, it will still be considered only 1 day overdue on 1st Sep, 2020 and therefore won’t be classified as an NPA. It will be classified as an NPA only if it remains unpaid for 89 days post 31st Aug i.e. till 28th Nov, 2020.

Supreme Court interim order:

After the completion of the moratorium and standstill period post 31st August 2020, banks would have had to start recognizing and providing for NPAs. However, the Supreme Court has passed an interim order banning declaration of NPAs until it reaches a final verdict on the various petitions filed with it. As a result, most NPAs will be recognized only in the December or March quarter as and when permitted by the Supreme Court.

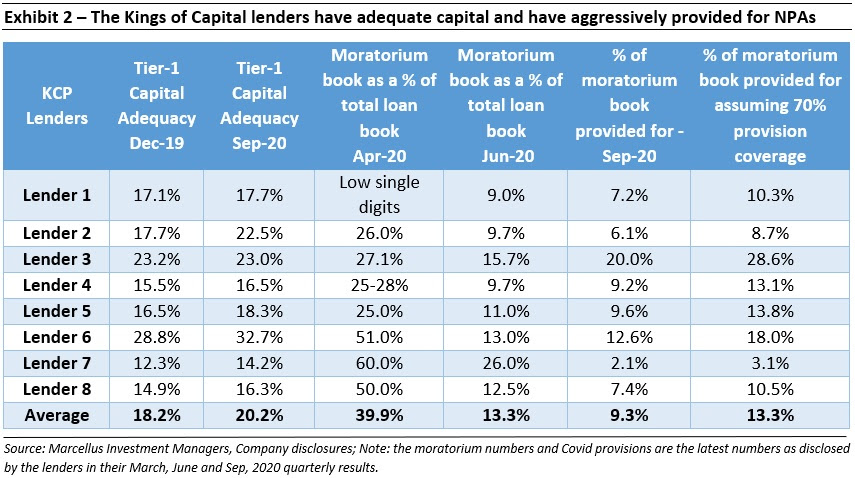

As per the illustration in the previous section, the P&L impact of the GNPA% number flows through only once NPAs are recognized. However, because no loan was required to be classified as overdue between March to August 2020, banks created provisions based on their internal estimates of loans which will be eventually classified as NPAs, their ability (in terms capital adequacy) and their willingness (in terms of taking the expenses upfront). However, lenders in the Kings of Capital portfolio (KCP) have not only estimated the amount of NPAs but have also aggressively provided for those NPAs as if there were no standstill asset classification, moratorium or Supreme Court judgement in place. For the reasons described below, this conservative stance on provisioning puts the KCP lenders in a very strong position as the Covid-19 crisis abates.

The Kings of Capital lenders are well placed to gain market share

-

Loan book under moratorium of KCP lenders was lower than that of the industry:

As per RBI’s July, 2020 Financial Stability Report, 50% of all loans across India’s lending sector were under moratorium as on 30th April, 2020. As illustrated in Exhibit 2 below, this number was ~40% on average for the KCP lenders which further reduced to ~13% in Jun, 2020. Therefore, to start off with the loan book under moratorium itself was lower by a fifth for the lenders in the KCP portfolio.

-

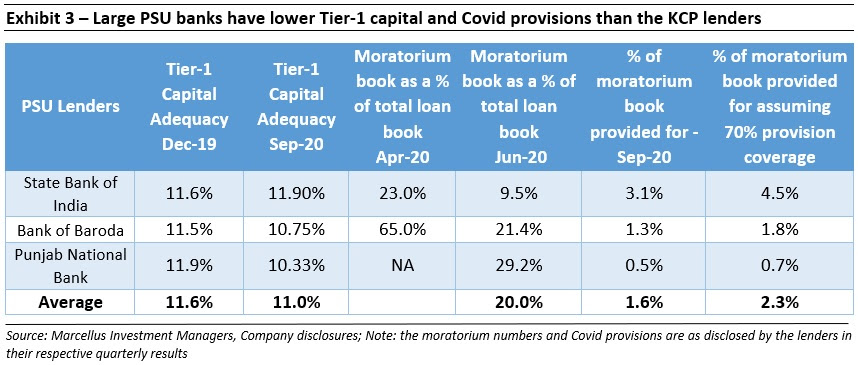

The Covid provisioning for KCP lenders is much higher than the industry:

As seen in Exhibits 2 and 3 below, on average the KCP lenders have on average already provided for 13.3% (assuming a 70% provision coverage ratio) of their loan book under moratorium while the three largest PSU lenders – which have a cumulative market share of 27% i.e. almost twice that of the eight KCP lenders – have on average provided for only 2.3% of their moratorium book. This translates into an average provision of 1.2% of the overall loan book for the KCP lenders and 0.2% of the overall loan book for the three PSU lenders.

Tier-1 Capital of KCP lenders has actually increased post Covid:

As illustrated in Exhibit 2 below, the Tier-1 Capital of the KCP lenders has actually increased by a couple of percentage points since Dec, 2019 despite agressively providing for NPAs in the past three quarters which demonstrates their strong and resilient operating profitability as well as the ability to raise equity even in the midst of a crisis.

Investment implications

As the Covid NPAs are made public over the next few months, we expect to see the following impact on the KCP lenders:

-

The profitability of KCP lenders will not reduce in proportion to the increase in the gross NPAs in the next few quarters:

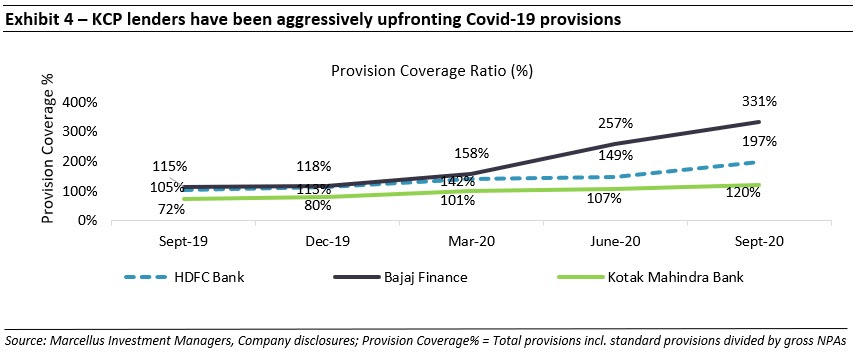

Because the KCP lenders have not waited for recognition of NPAs and have upfronted provisioning, a large part of the impact on the P&L has already been made public. As illustrated in Exhibit 4 below, the KCP lenders have continued to increase provisions as if the moratorium or the standstill asset classification benefit was not available. As a result, even though we will see the GNPA% numbers optically rise in the next few quarters, the profitability of the KCP lenders should not be impacted proportionately. |

|

|

-

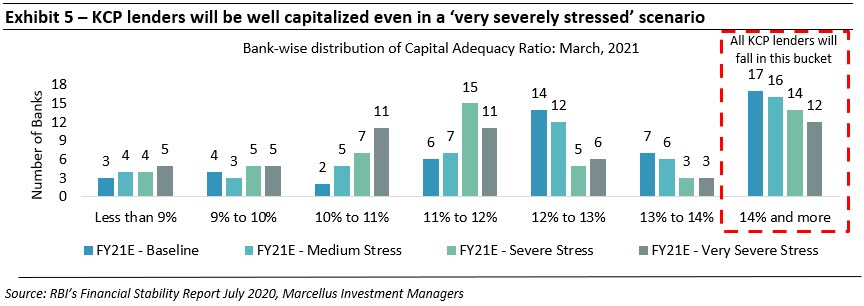

The KCP lenders are well capitalised to absorb any incremental stress that may emerge:

The KCP lenders are overcapitalised with an average Tier-1 ratio of ~20% which is actually higher than their pre-Covid Tier-1 capital, this is because of their strong operating profitability and ability to raise equity during Covid. As a result, the KCP lenders will be able to absorb any further stress that emerges in the lending ecosystem. For instance, the RBI in its July, 2020 financial stability report has defined a ‘very severely stressed scenario’ as one where the GNPAs of the Indian banking sector increase by 1.7x from 8.5% in Mar-20 to 14.7% in Mar-21. As illustrated in Exhibit 5 below, the RBI estimates that only about 20% of Indian commercial banks (12 of the 53 banks) will have a capital adequacy of more than 14% in such a severely stressed scenario. As per our estimates, all banks and NBFCs in the Kings of Capital portfolio will have a higher than 14% capital adequacy even in a severely stressed scenario. |