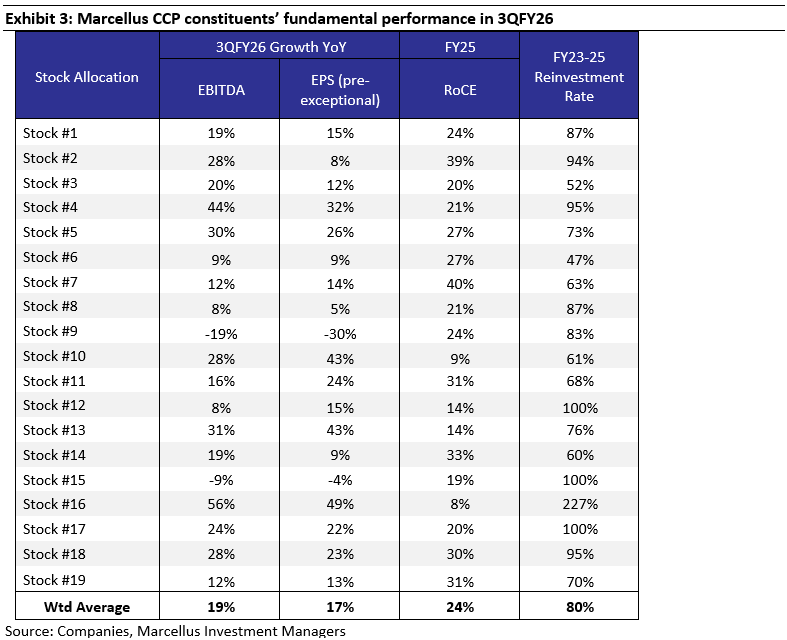

In an uncertain macroeconomic environment shaped by AI disruption and shifting global geopolitics, the Consistent Compounders Portfolio (CCP) strategy has evolved significantly. While maintaining a concentrated portfolio focused on good-quality businesses, we have diversified our top holdings across uncorrelated sectors such as healthcare, auto components, and export-led manufacturing. This deliberate shift away from our historical reliance on large-cap consumption, financials and IT services helps mitigate AI related risks to jobs and the domestic growth slowdown. Furthermore, allocations have been increased towards companies with higher expected growth, valuation re-rating potential and recent upgrades to consensus expectations. So far in Q1/Q2/Q3 FY26, the portfolio constituents delivered weighted average EPS growth of 10%/14%/17% YoY respectively.

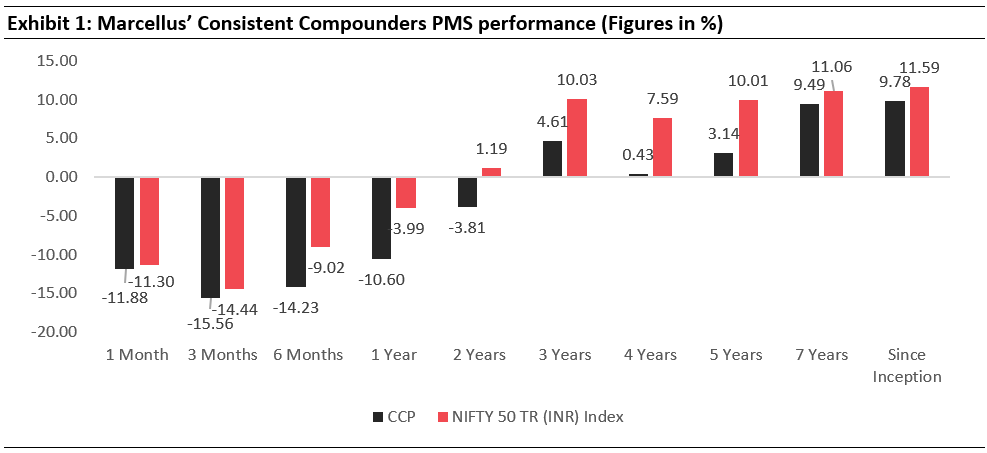

Source: Marcellus Investment Managers; Marcellus Performance Data shown is net of fixed fees and expenses charged till 31st March 2026 and is net of Performance fees charged for client accounts, whose account anniversary / performance calculation date falls upto the last date of this performance period; since inception & 3 years returns are annualized; other time period returns are absolute. For relative performance of particular Investment Approach to other Portfolio Managers within the selected strategy, please refer https://www.apmiindia.org/apmi/welcomeiaperformance.htm?action=PMSmenu, Under PMS Provider Name please select Marcellus Investment Managers Private Limited and select your Investment Approach Name for viewing the stated disclosure. The calculation or presentation of performance results in this publication has NOT been approved or reviewed by the SEC, SEBI or any other regulatory authority.

The external environment for Indian firms is increasingly uncertain due to the frequency of disruptions (e.g. AI’s impact on human labour and business models), geo-politics (global trade reset) and crisis events (wars, pandemics, etc). To mitigate the risks and benefit from the opportunities that such events present, Marcellus’ CCP portfolio construct has diversified across several dimensions over the last 3 years. The portfolio remains concentrated around certain themes, whilst being diversified across others. In this newsletter we articulate how we view the positioning of the CCP portfolio amidst the current uncertain external environment.

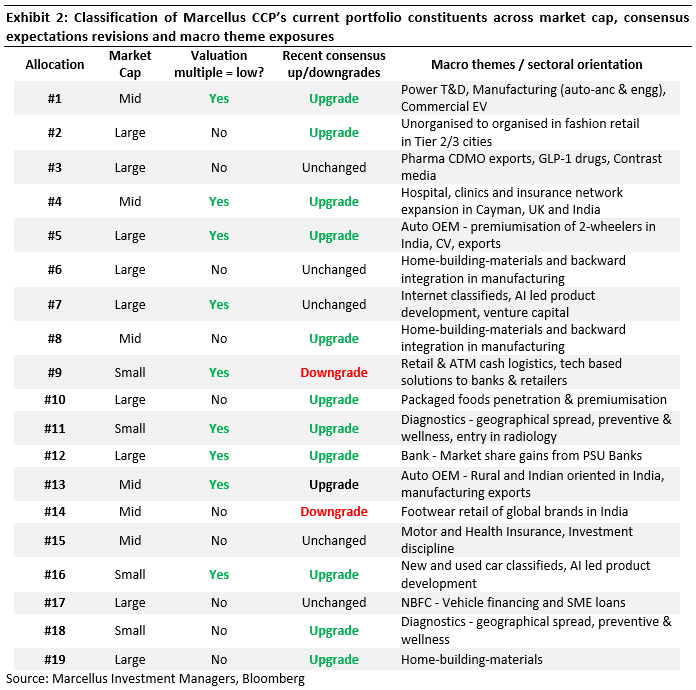

CCP remains a concentrated strategy with over 40% of the portfolio allocated to the top-5 positions. Total number of stocks currently in the portfolio is 19. Stock selection is still done basis the quality of the underlying businesses – good quality management teams running deeply moated businesses with strong cash generation and prudence in capital allocation decision making – thereby concentrating the portfolio towards ‘Quality’ as an investment style.

However, there is a significant change in the degree of diversification within the portfolio. For instance, as highlighted in the exhibit above, the sectoral orientation of the top-5 allocations in the portfolio is equally spread across non-correlated areas like power transmission & distribution, pharma exports in outsourced drug manufacturing & APIs, auto OEMs, auto ancillaries, healthcare and fast fashion retail.

Expected earnings growth over the next 3-5 years across all portfolio constituents is mid-teens or higher. In terms of forward valuation multiples, across more than half of the allocations, expected valuation changes are targeted to contribute positively towards portfolio performance.

Intended benefits / potential risks of CCP’s current portfolio construct

AI’s impact on Indian IT services: The Indian economy’s historical reliance on IT services exports is facing structural challenges due to a maturing global outsourcing market and the accelerating substitution of human labour by AI. Major IT companies are cutting thousands of jobs as artificial intelligence increasingly handles coding, quality assurance, and back-office operations. This disruption threatens the synchronized growth between IT job creation and urban middle-class consumption. However, this transition also creates a localized, structural opportunity for export-led manufacturing to emerge as India’s next growth engine.

Over the last two years, Marcellus’ CCP has completely exited from exposure to IT services (TCS and HCL Tech have historically been part of the portfolio). Although we have reduced portfolio exposure to urban-middle class consumption and increased exposure to export-led non-IT services businesses (17-20% weighted average exposure currently), the portfolio continues to have a reasonable exposure to domestic consumption as a theme, which is actively being reviewed as the external environment evolves.

AI’s impact on business models of internet companies: As evolution and adoption of artificial intelligence progresses, we expect operational or knowledge-based processes to get disrupted. This has significant implications for most businesses due to potential changes around how they operate and compete to add value to their customers. Investment decisions in CCP are intended to be based on three critical dimensions.

Firstly, will the value disruption of unit-economics of a business be more than offset by upside from scale expansion upside or vice a versa? Hence, will the winning business in the said industry have deeper or shallower moats post-AI?

Secondly, will the speed of disruption be rapid (1-2 years) or gradual (5years+)?

Thirdly, will the incumbent business (i.e. the company we are considering for investment) disrupt itself or will a new player disrupt the incumbent?

Quality and agility of the management team and its capital allocation decisions also plays a critical role in our assessment.

Over the last two months, as share prices of internet companies have corrected, we have added allocations to two internet businesses in CCP. In both the cases, we believe majority of the value addition to the customer (non-standard, high-ticket used car purchases, and softer aspects involved in recruitments with high volume of applicants) is built on trust and capabilities that are being enhanced through the ongoing proactive use of AI LLMs based radical changes made to their product offerings. The key-risk we run in our investment hypothesis is if LLMs themselves vertically integrate to offer such value-adds and hence if customers’ discovery, selection and transaction is entirely on the LLM platforms, instead of LLM based incumbent platforms.

Risks to growth in the Indian economy: India is witnessing a sharp deceleration in consumption growth, driven largely by a stagnation in white-collar job creation and a reduction in real wages over the past eight years. As the post-Covid “revenge spending” unwinds, net household financial savings have plummeted, approaching a 50-year low in FY24. Compounding this, average employee incomes in major companies have failed to keep pace with CPI inflation, eroding purchasing power. With consumption accounting for 60% of GDP, these factors present a sustained risk to overall corporate earnings growth. We intend to mitigate these risks in our portfolio through a combination of:

- Sectoral re-orientation: We are increasing our exposure to structurally growing sectors like healthcare (around 25% exposure currently) and relying on company-specific triggers such as aggressive market share capture and internal efficiency improvements.

- Skew towards Enterprising capital allocators: Our portfolio is increasingly skewed towards “enterprising compounders,” which now constitute over 70% of our allocation. Unlike traditional linear compounders, these companies aggressively reinvest 80%-100% of their cash flows not only to deepen core competitive advantages but to consistently incubate and scale new businesses beyond their core target markets. This dual-engine approach helps drive higher earnings growth rates, unlocks optionalities in new ventures, and ensures greater longevity of cash flow compounding. Historically, during a crisis (e.g. Covid, IL&FS crisis, demonetisation etc), such capital allocators in our portfolio have proactively ramped up capital expenditure, pursued strategic acquisitions, and made tactical working capital investments to secure cheap raw materials. Such execution during crisis allows these firms to mitigate near-term impacts while laying the foundation for accelerated market share gains and robust free cash flow compounding in subsequent years.

- Portfolio construction agility: Recognizing paradigm shifts in the economy, we have doubled the CCP coverage universe to enhance portfolio construction agility. This broadened scope is likely to enable us to identify evolving business models that have crossed the inflection point of attractive unit economics. Our position sizing remains aggressive yet disciplined, balancing our high conviction against consensus expectations aiming to trim optimism when valuations peak and increase positions when markets price in excessive pessimism. One of the outcomes of this agility has also been around a reduction in allocation of large cap stocks in CCP from 80%+ till three years ago to 51% currently (highlighted in exhibit 2 above).

Risk of lack of exposure to certain parts of the stock market: Marcellus’ CCP currently has significantly low exposure to sectors such as IT services and lenders vs benchmark indices. It also has zero exposure to sectors such as metals, oil and gas, PSU Banks etc. Hence, we run the risk of weak portfolio returns in the short run if the broader market’s performance is driven largely by sectors where we have chosen not to have much exposure (as was the case in FY26). Over the long run, we expect to mitigate this risk by delivering healthy absolute returns through the concentrated exposure to few good quality stocks / sectors. We also run the risk of de-rating in our portfolio if “Quality” as a style factor continues to be out of favour for the broader market. We expect to offset this risk through an increase in value orientation, targeting “growth surprise” compounders and hence, prioritizing companies showing capital allocation-based quality upgrades with non-core optionalities and accelerated growth potential.

Fundamentals of the portfolio remain strong: Earnings growth momentum has continued to be healthy in FY26 for the overall portfolio, both in absolute terms as well as relative to the broader market. Our portfolio companies have demonstrated a weighted average YoY EPS growth of 10%/14%/17% so far in Q1/Q2/Q3 FY26 respectively i.e. the first 3 quarters of FY26 (see table below). Current portfolio constituents delivered FY25 ROCE of 23% and a 3-year average reinvestment rate of 74%. These metrics are the building blocks of sustainable long-term compounding.

If you want to read our other published material, please visit https://marcellus.in/

The mentioned stocks form part of Marcellus portfolio thus Marcellus clients, Marcellus employees and their immediate relatives may have interest in. The described stocks are for illustration & education purpose only and not recommendatory.